I think investors reflexively look down on simple investing strategies and are drawn toward complex strategies. In this article, the writer compares 2 strategies 1. A simple SIP 2. Buying the dip (Anytime the market is not at a high). He further adds a condition in the test, that for buying the dip, the investor had advance knowledge of when the dip would occur.

Guess which strategy outperformed in the long run?

Also, adding this article which kind of speaks to the point. More information doesn’t lead to better investment decisions.

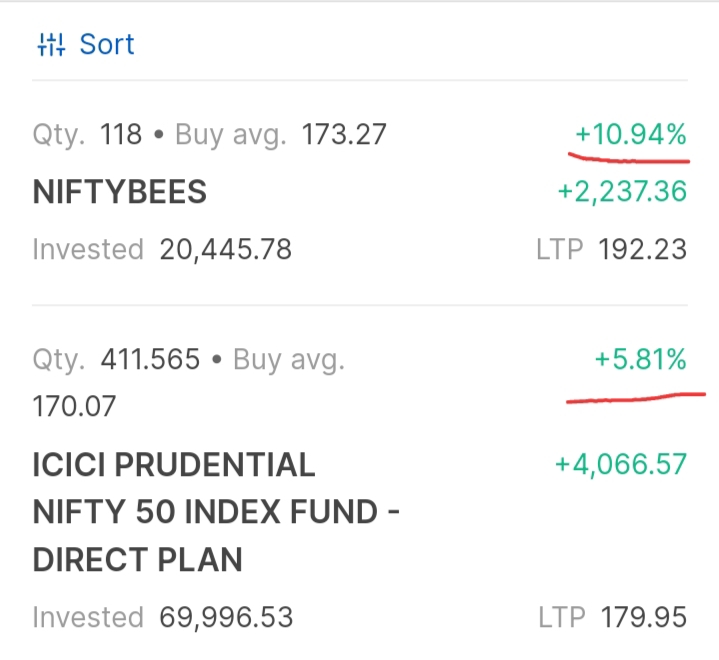

Typically, SIP doesn’t mean buying a set number of units.

Rather a set amount is invested periodically.

Thus, when the price of the asset is low,

one ends-up purchasing more of the asset with the same investment amount.

SIPs allow investors to save regularly with a smaller amount of money while benefiting from the long-term advantages of dollar-cost averaging (DCA).

Buying more units in dips involves timing the market (i.e. trying to correctly identify the “dips”).

What the first of the above articles highlights,

is that such attempts to time the market

have under-performed SIP/DCA over the long-term.

Just to add, Simple SIP is the best option to create long term wealth, probably once wealth is created, in order to prevent sequence of return risk , one should consider equally simple strategies like permanent portfolio or all weather folio.

In the sunset year, adopting the simplest strategy would give peace of mind. At old age we humans are gullible to sweet talking shrewd agents. They can easily play around fear/hype/greed. We need something simple to will help us to stick to the pan and not get hypnotised by fancy marketing.

When we are old, we need debt, a good, fat debt PF, not equity, unless we want to give something to our family at this age too, something like an index ETF or fund.