It can be said without a doubt that one of the key drivers of our economy’s growth in the last few years has been the emergence of the India stack.

Account Aggregator (AA) Framework has been the latest addition to the India Stack. The AA framework allows one to securely and digitally access and share information from one financial institution they have an account with to any other regulated financial institution in the AA network only with their explicit consent.

Sahamati, the collective of AA framework recently published a white paper on the Expected Evolution of Account Aggregator Ecosystem: 2023-27 and here are some of the key highlights:

First year - Overview

-

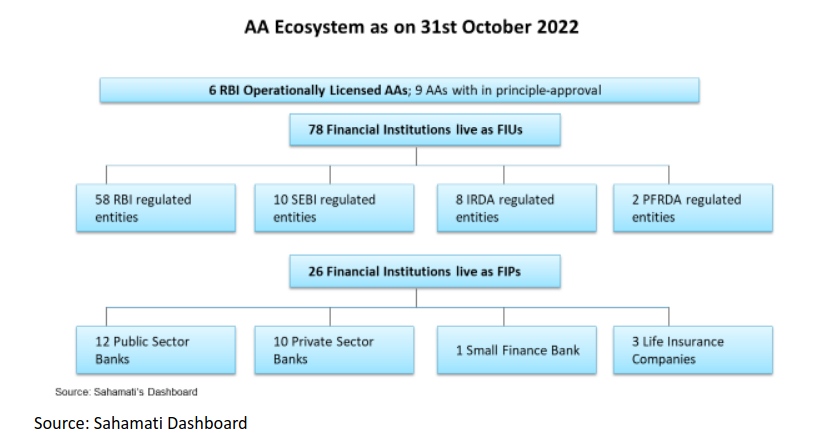

Since the AA ecosystem was officially launched in September 2021, 23 banks and 3 life insurance companies have gone live as financial services provider (FIPs), and 78 entities have gone live as financial services provider (FIUs), these are the entities regulated by one of the four Financial Service Regulators (FSRs) like RBI, SEBI, IRDAI, PFRDA.

-

More than 1.1 billion accounts in the form of singly held savings accounts and sole proprietorship current accounts have been enabled (available to be shared through AAs with customer consent). Further, there are 6 operational AAs and another 9 in-principle AAs waiting to get their operating license from RBI. As on October 31, 2022, more than 2.05 million customers have used AAs to give consent and successfully shared data from their existing FIP to potential FIU.

Existing participants

- Sept,2021 to Sept,2022 has been a defining period for the Ecosystem, with significant growth in the adoption and penetration of AAs. From March 2022-August 2022, all public sector banks joined the AA Ecosystem as a FIP increasing its coverage exponentially, followed by SEBI and PFRDA coming out with circulars, enabling for their respective entities to join the AA Ecosystem.

Expected evolution of the Ecosystem

-

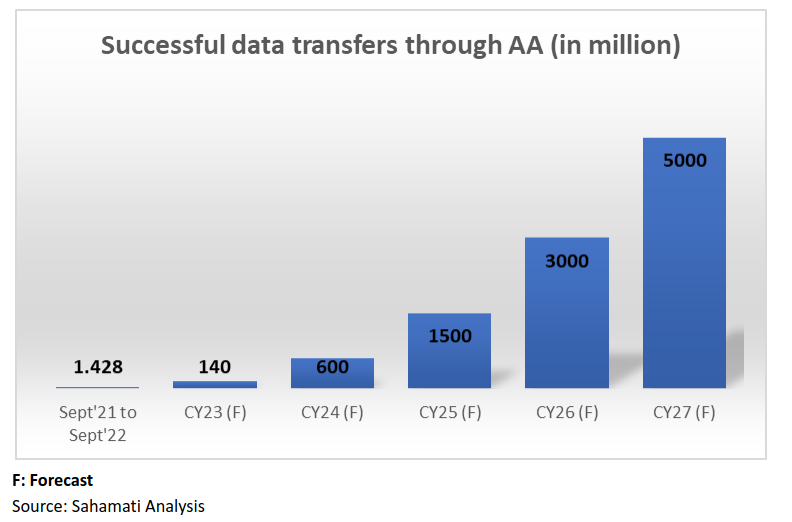

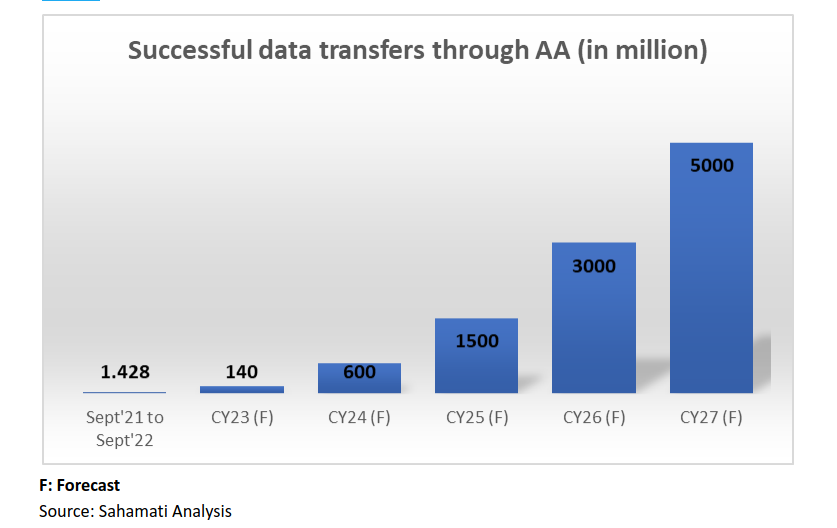

As per a market sizing exercise conducted by Sahamati based on an assessment of emerging use cases, the successful annual consents fulfilled, resulting in data transactions through AA, is expected to reach 1 billion by the year ending 2025 and 5 billion by the year ending 2027.

-

By the year 2027, retail lending is expected to constitute around 38% of the bank account statement shares on AAs, while share of MSME lending is expected to be at 10% of bank account statement shares.

-

How’s the performance so far?

-

The market size for Account Aggregator can be defined in terms of the number of consents successfully fulfilled, resulting in successful data transfers

-

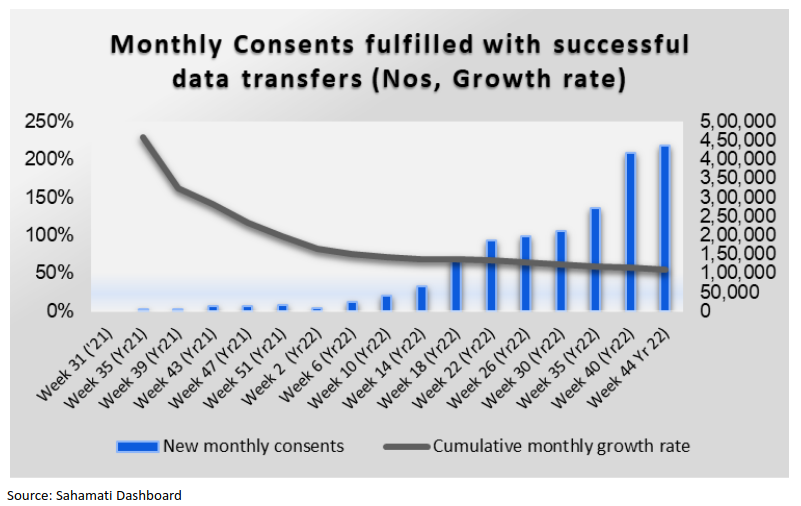

As of 31st Oct '22, more than 1.1 billion accounts in the form of singly held savings accounts and sole proprietorship current accounts have been enabled (available to be shared through AAs) on AA. Till October 2022, more than 2 million annual cumulative consents have been fulfilled successfully, resulting in data shares from FIPs to FIUs through Account Aggregators.

-

The usage penetration of AA is currently at just 0.2% ( at 2 million consents on a base of 1.1 billion enabled accounts).

-

The monthly growth rates have been stable at 50-60% over the past few months, thus showing sustained progress

Projected Data Transactions: 2023-2027

Existing and future use cases.

-

Securities market is expected to be the second biggest user of AA, primarily for the purpose of personal finance management, wealth management and demat account opening.

-

Insurance is expected to have a limited use case for bank statement shares through AAs. However, the usage of AA in the insurance sector is expected to improve significantly once existing insurance policies and IT returns data are made available through AA.

Here’s the list of some of the use cases of AA framework going forward.

| SNo: | Category | Sub-Category | Use Case |

|---|---|---|---|

| 1 | Lending | Retail / MSME | One-time bank statement pulls for underwriting and making a loan offer Recurring bank statement pulls for loan portfolio monitoring and building early warning signals |

| 2 | Securities | Personal Finance/ Wealth management / Income verfication for demat | Recurring bank statement pulls for a consolidated view of a citizen’s financial holdings and provide necessary services. |

| 3 | Insurance and Pension | Term Life & NPS | One-time bank statements pull for advising the customer on the right pension amount required for sufficient retirement planning and offer a policy with adequate sum assured and premium commensurate with the risk and income profile |

| 4 | Citizen | Income Tax Filing | Enabling tax computation and return filings for the citizen itself |

| 5 | Securities | Wealth Management | Enable financial advisory by pulling information from multiple accounts- deposits, Demat, mutual funds,insurance, credit cards, pension to provide a singleview of all assets of a citizen by consolidating balances and transactions held in disparate accounts |