Given FDs are now giving 7.5% for 1 year tenure, and short term/liquid debt funds are only trending at 4.5%-5%, is it better to invest in FDs for a fixed 1 year tenure?

Or will the liquid fund yields improve in the short time horizon?

You can invest in non-banking companies like Bajaj Finance. They give better interest rate than bank.

Small bank FD are giving 8% so can also go for it.

The overnight rate is close to 6%, so if you invest in liquid/ or money market funds, you should get a current yield of about 6.5% to 7% depending on the tenure.

I don’t think the yields will rise much from here because I think we are closer to the peak policy rate.

2 Likes

but my broader point is, why invest in debt funds at all when FDs are generating better returns (if tax is not considered) and why are Debt funds doing so badly now even in a rising interest rate scenario? Can understand about long term debt funds, but liquid funds should have seen a rise, right ?

Old bonds should mature which have lower interest rate, then new bonds with high coupon rate should be purchased, and this buying and selling is a continuous process, so slowly, the new bonds of high coupon rate, it will reflect in the returns.

There could be other economic reasons, good liquidity all over, so that bond issuers have other venues to raise capital. Banks are the biggest, so they have all kinds of clients, debt funds are limited in that sense.

The rates have risen since May. Before that, liquid funds were yielding around 4%.

The fastest transmission happens in the overnight funds. The liquid and money market funds roll over their existing papers on maturity, so there is a slight lag.

2 Likes

got it. So probably in a quarter, the rates should normalise. Thank you!

They already have normalized to a certain extent. The one-month return is about 0.55%. If you annualize that, it comes closer to 6.8%.

1 Like

Well most people do consider taxation aspect before taking investment calls ![]()

And for higher brackets, post tax liquid fund is still better than FD

Apart from taxation, lot of people invest in liquid funds so that they can pledge it and use the margin for trading.

Each one has a different need and invest accordingly.

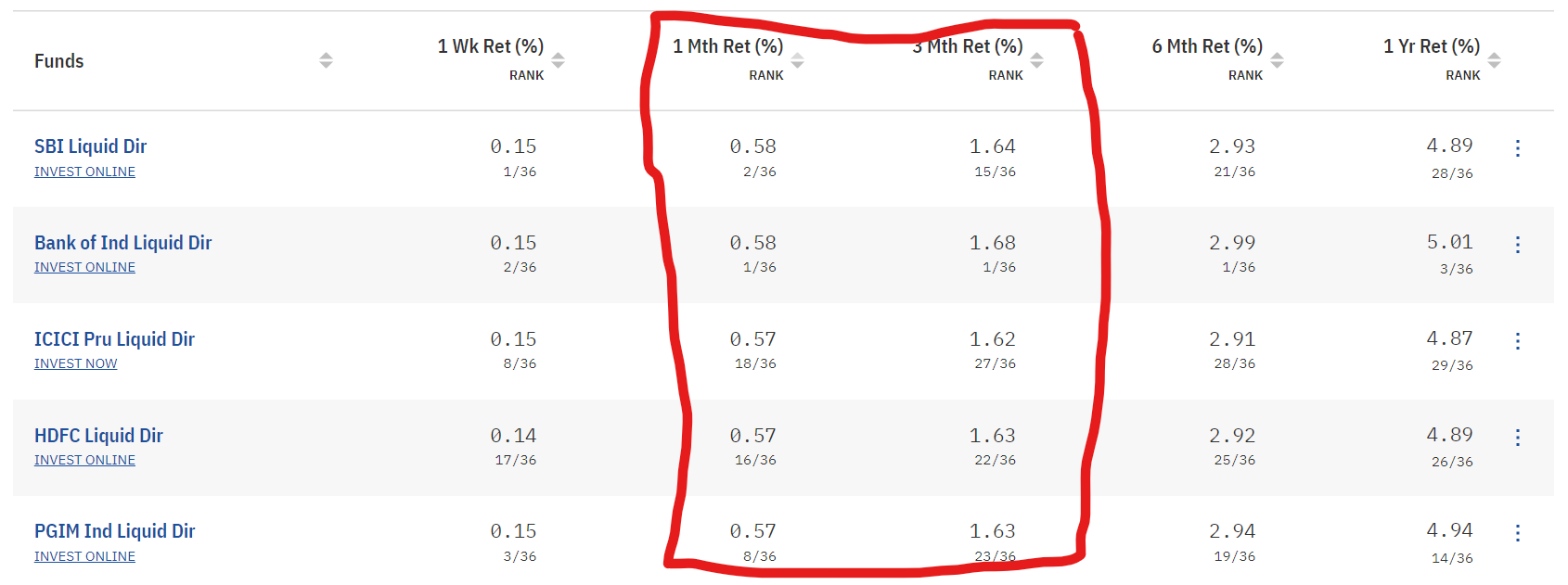

Seems like you are looking at last one year return of liquid fund and taking this call. Look at last 1month / 3 months and extrapolate that and you will see that liquid funds are doing much better than 4.5.

1 Like

yea agree Akash. I actually was looking at Low duration fund and a particular debt fund which was under performing it’s category. But agree, Liquid funds are doing well if you look at 1M returns.

1 Like

Thank you @Sreeraag_Gorty for bringing up this interesting topic. And thanks to @Akash_Shah and @Suyash.K and @GB26 for sharing the valuable inputs.

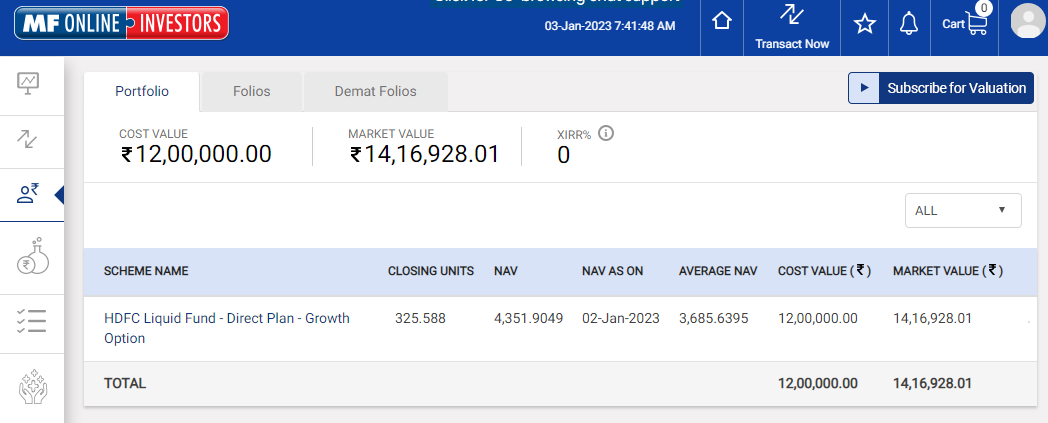

It might be true that the liquid funds are picking up recently. But I have stayed invested into the " HDFC Liquid Fund - Direct Plan - Growth" for more then 3 years and 8 months now, but still I have got lesser returns then what you have mentioned in your first post.

I invested 12,00,000 in April 2019 and its value has become Rs 14,16,928 as of today morning. I have attached the snapshot as well.

Because of this reason only, I am not that much interested in investing this other 1 crore amount that I have in the savings account, into the Liquid Fund as well and has been looking for alternative options which could give better returns then the Liquid Funds -

https://www.moneycontrol.com/mutual-funds/nav/hdfc-liquid-fund-direct-plan-growth/MHD1205

Thanks and regards

1 Like

The ascending order in which both returns and risk increases is overnight, liquid, money market, UST, short term etc.

So a few years ago, liquid funds did give around 6-7% I guess, but they are not supposed to give. They give more than a SB account, as they can invest in bonds of only 91 days. For more return we have to go for MM or UST, as the tenure of the bonds increase, the average maturity increases, so does the return, and so does the risk.

So in a sense, we don’t invest in liquid funds, we park our funds.

I have invested in liquid and MM funds.

2 Likes

Rates had fallen when Covid struck and were at low 4% for a good 2 years.

If liquid funds are yielding about 6.8% presently and rates don’t change, then that’s the approximate return you can expect in one year’s time.

Interest rates are dynamic and ideally, you’ll want to keep moving the maturities of your debt portfolio based on your call on interest rates. If you think that rates may be near its peak and would be lower in future, it’s better to invest in longer dated papers as compared to liquid funds.

1 Like

You didnt invest in liquid fund, you parked you fund?!

No I invested in liquid funds, because I was not particular about the return I will get from them, as I wanted it grow without any risk.

And if one wants to be absolute here, the best there is, is Quantum liquid fund which only invests in sovereign and PSU type papers, hence the lowest returns with the best safety.

For the more adventurous there are always credit risk funds, where a part of capital can go kaput, but there is a chance of getting more ![]()

Well XIRR works out to 4.5% so you have got precisely what was mentioned in first post ![]()

| 4/1/2019 | (1,200,000.00) |

|---|---|

| 1/2/2023 | 1,416,928.00 |

| XIRR | 4.52% |

1 Like