I have got 1 crore+ amount that is lying in my savings bank account, which is giving just 3.5 percent interest. I need to invest this amount into such instruments, which would give me the following benefits -

Safety of the principal amount that is invested.

Guaranteed minimum fixed returns on the investment.

Maximum % of this investment amount should be allowed to be PLEDGED as “CASH EQUIVALENT COLLATERAL” for getting the CASH COMPONENT of the overall Trading Margin, so that I can then use this margin for doing the investments as well as active intraday trading in the NSE Stocks, Futures and Options Segments. I do not trade into any other exchanges or instruments.

If any of you could please make some suggestions in this regard, that would be really helpful. Thank you so much for your time.

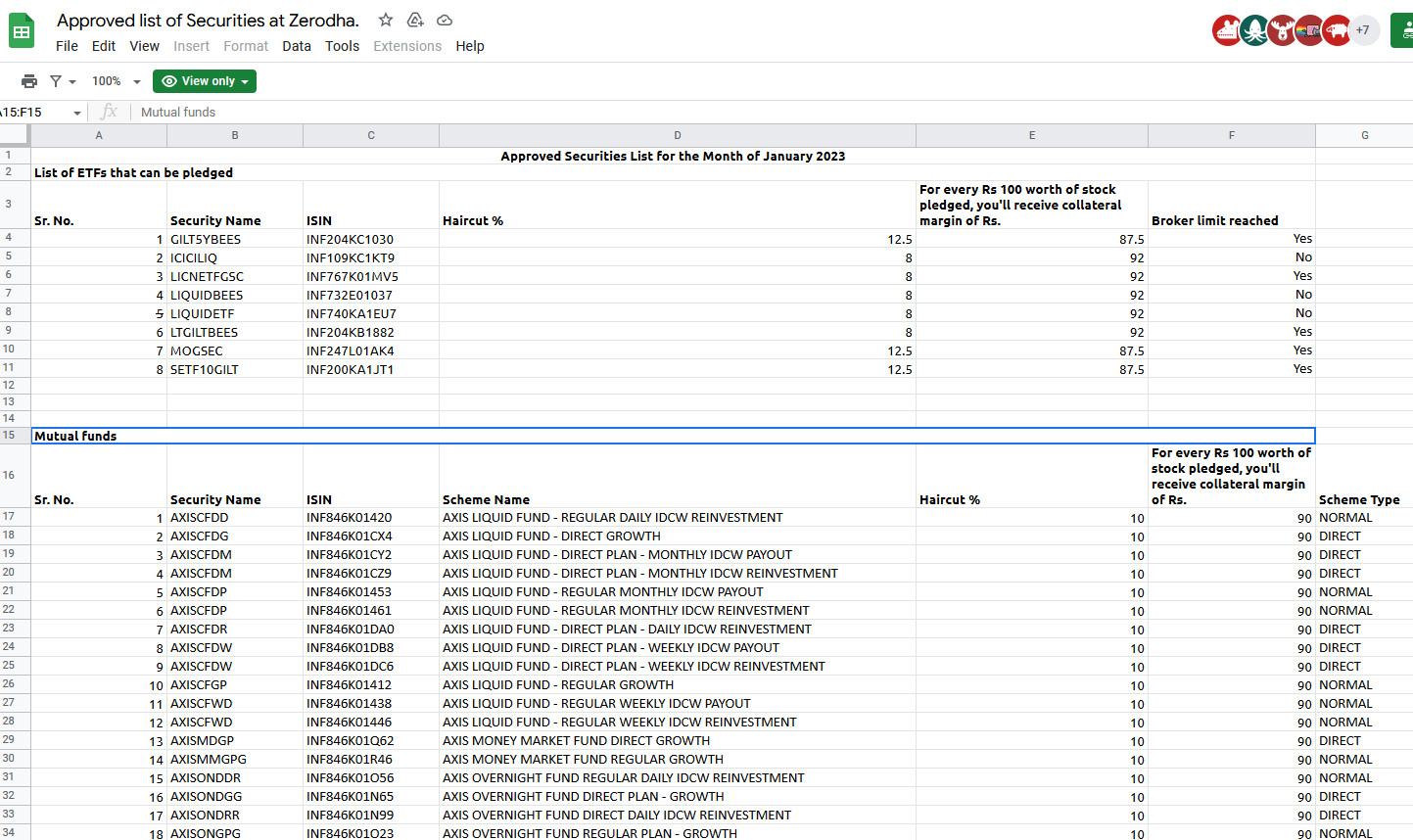

Please notice these notes given at the very bottom of the Excel sheet from the above link.

Notes

Haircut as applicable subject to a minimum of VaR+ELM+Adhoc

The clearing corporation has set a certain limit on the number of shares/units that can be pledged per security through a broker. If the broker limit is reached, you will not be able to further pledge such securities for margin.

For stocks pledged before 4pm, collateral margin will be available on T+1 day.

The collateral margin received by pledging cash component securities can be used fully towards any margin requirement for your open positions. You will not be required to maintain cash separately if the collateral from cash component securities covers the margin requirement.

The collateral margin received by pledging non-cash component securities can be used only up to 50% of the margin requirement for your open positions. The exchange stipulates for the remaining 50% margin to come in the form of cash or cash equivalent collateral. Any additional utilisation of the non-cash collateral, over and above 50% of the margin requirement will be liable to delayed payment charges.

Cost of pledge: Rs.30 + GST per scrip irrespective of quantity of stock pledged.

For all unpledge requests placed before 2 pm, stock will be available in demat account for trading on T+1 day.

You can pledge NIFTYBEES or BANKBEES and hedge it using monthly index options.

Whenever market go down your portfolio will be in loss and your hedge will give profit.

This technique is giving 4 to 5pct return on an average per month.

Please note that to hedge we are not using put buy or future sell but an inexpensive combination of monthly butterflies and put spread.

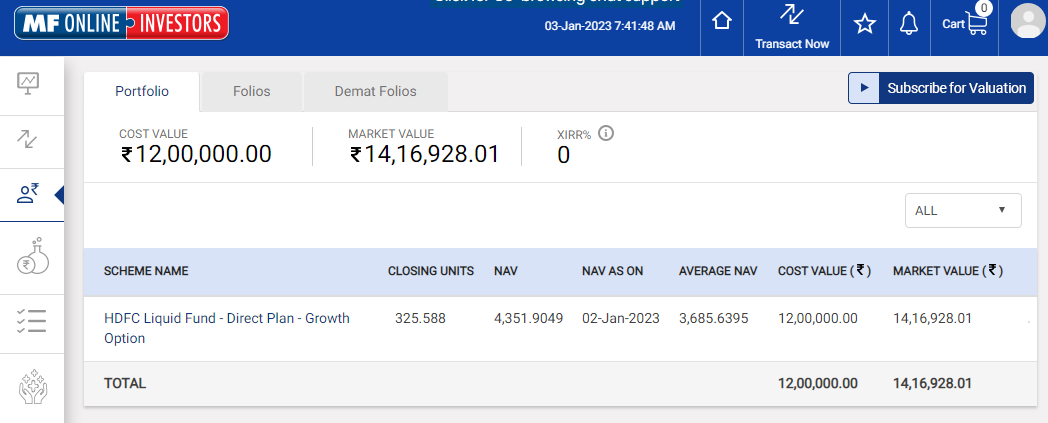

The Liquid Funds are safe overall, but they are no longer giving better returns, therefor I am not too eager to invest any more amount into them, other then the 12,00,000 investment that I made in them in April 2019 and which I am still holding, but getting very low return overall.

I am leaning towards buying some Mutual Funds for pledging, but these days there are so many different type of Mutual Funds available, that it could become very confusing overall. From the following link, should I simply look at the “Hybrid Funds and the Debt Funds only” if I want some safety of my principal amount ? Because in equity funds etc. there is a risk of loosing your investment as well. Kindly suggest.

And I am also getting this thought that maybe I should simply move this 1 crore to some Savings Bank Account which is giving good interest in the range of 6-7 % as HDFC Bank is giving me just 3.5% interest only. This step will give me some more time to do the proper research for finding out those Mutual Funds, which will suite my requirements.

Please look at the very bottom table from this link - Ujjivan Small Finance Bank in India | Build a better life which shows the Interest Rates for the - Savings Account of Ujjivan Small Finance Bank. I am thinking about moving my money to them today itself, and keep them there, till I reach a final decision.

Am I making some mistake in this and are there any better options to park the idle cash for a few days/weeks to get around 6 % interest? Please let me know.

I thought all debt funds give the returns that are comparable to the Bank FD etc. but many of these funds are giving much higher returns. What do you guys think?

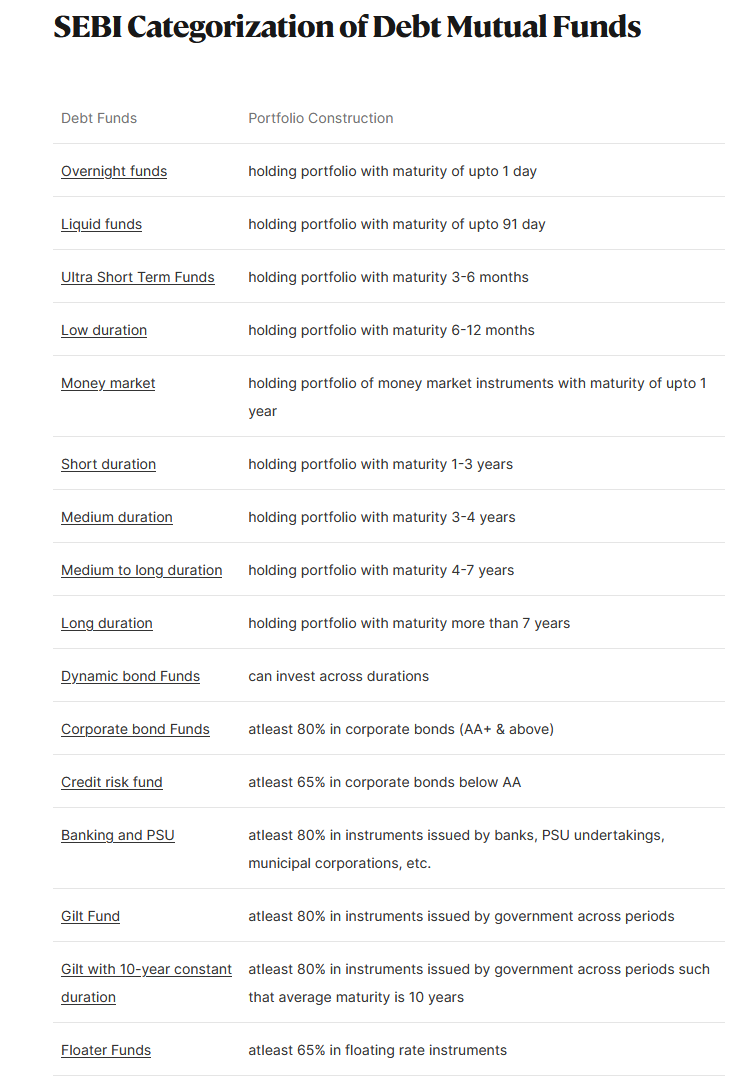

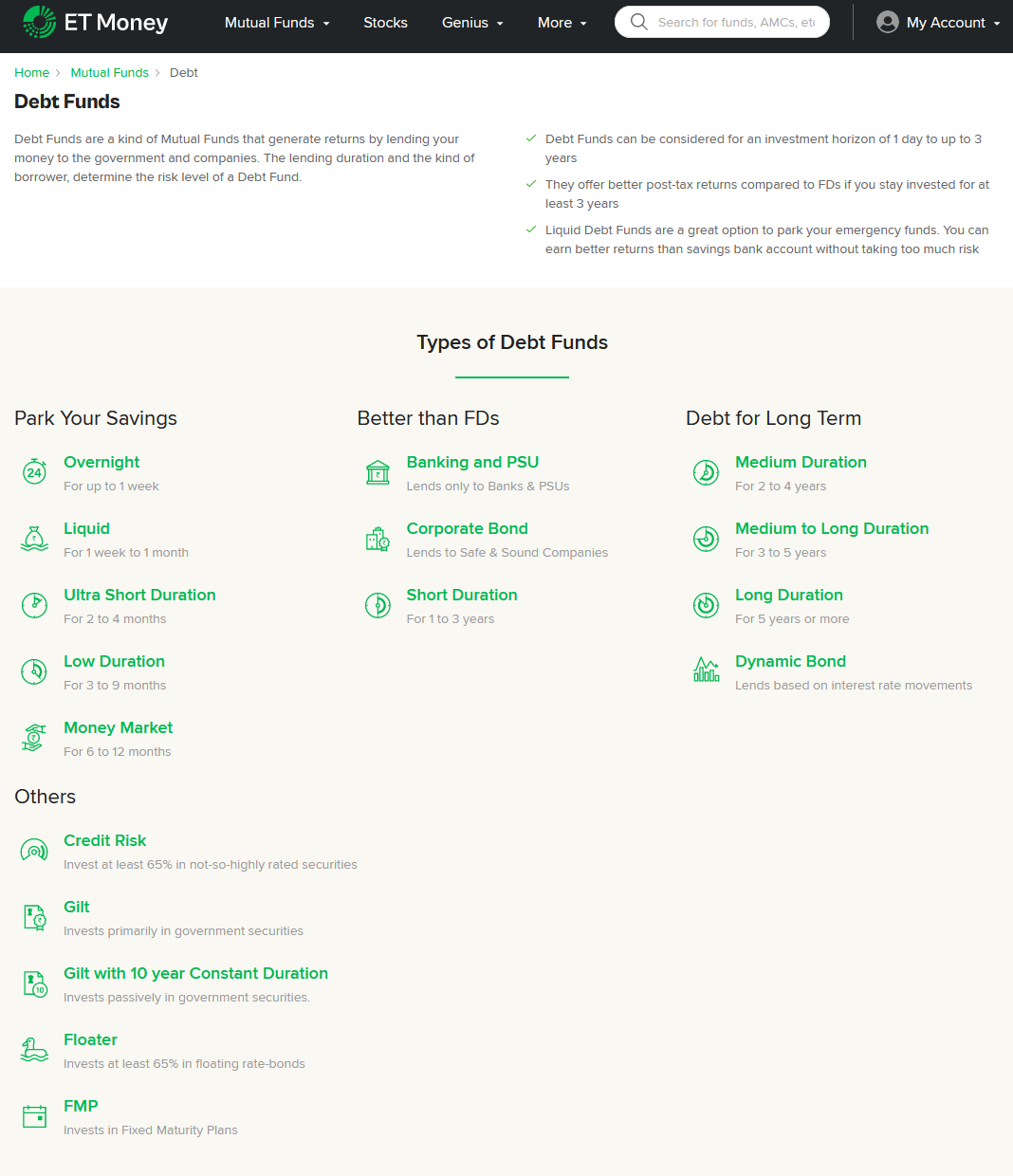

Actually I have got really confused by the presence of so many different categories in the Debt Mutual Funds, as you can see in the following snapshots -

Please look at the second tab of that excel sheet named “CASH COMPONENT” in which there are a total 342 Mutual Fund Schemes listed, which all have the haircut of just 10 % and therefor will give me maximum trading margin for my personal trading.

I have to select a few Debt Mutual Fund Schemes from this list of 342, which are overall safe and will give me the returns of around 6 % and then I just have to divide this 1 crore amount into these different schemes, so that I can then pledge them with the broker.

If someone could please guide me in this task, then I will be really grateful. Thank you so much.

My exact requirement is to select a few Debt Mutual Funds from that list of 342 Funds given in the Excel Sheet, which will give me safe returns of above 6 %.

Liquid, MM and UST should do the job, but it seems UST is not available, check. Liquid will not give 6, MM and UST can give. Almost all fund houses invest in the same kind of paper, Franklin Templeton was a little different, it gave more returns than other fund houses, but it lost too. So you can check the PF of the funds if you are investing more, and then see the tenure of the managers so as to get a sense of how long and how good they have been doing, and then buy whichever fund houses you are comfortable with.

This note is just to give you a perspective of current interest rate scenario with Banks in India so that in case you continue to keep your money in SB account there are other banks who are offering higher rates than 3 to 4%

You have Indus Ind Bank which is offering 6% on SB account and IDFC 6.25% (Tiered rates)

Small Finance Banks such as Equitas and Ujjivan offer tiered interest rate upto 7%.

AU small finance Bank is also offering 7% but over 25 lacks.

These three small finance banks are listed entities and you can see their performance and capital adequacy in any website I personally would rank the Banks in the following order

Au Small Finance

Equitas

Ujjivan Small Finance.

I read in your post that you were considering to move the entire amount to Ujjivan. If I were you, I would not do that as I would not park 1 cr in this bank. Not at all, even though the funds are in SB account and can be moved out fast but not this level of amount. (This is purely my perspective)

I am very comfortable with IDFC and Indus Ind bank and would rather park my money in their SB account which is offering 6.25 to 6% and not opt for small finance bank for the entire corpus.

The above is from the SB account perspective. I am aware you are looking to pledge and make use of the limit. This is not possible with Bank FD or SB account. The max you can get is an OD which will not meet your needs.

However, If you are not keen on pledging then HDFC is offering FD rates of 7% for 10 years.

Axix Bank is offering 7.10% for 13 months and 7.25% for 30months.

AU small finance is offering 7.75 for 45 months whilst Equitas 8% for 888 days.

If you have a senior citizen at home, then the rates will be 0.50 to 0.75% higher. Axix 8% for 30 months.

Sharing what I’m currently doing, along with the thought process. I think it’s pretty similar to what your goals are.

At least 50% of the capital has to go to instruments considered as cash equivalents. And rest basis potential returns and safety (liquidity is not a consideration since I’m looking to hold these for long term.

Cash equivalent holdings:

My portfolio consists of GSecs, SGBs & Liquid funds. However if I had to do it today, I think most of it would go to gsecs maturing in 10-15 yrs. Haircut across almost all cash equivalent instruments in 10% (barring a couple of liquid etfs I guess, where it’s 8), so not an important consideration here.

Also, with current gsec yields, I’ve a slight bias towards these instruments and currently about 60% of my margin’s coming from cash equivalents.

Non-cash equivalent holdings:

Here’s where one may face the problem of plenty. So the way I look at it is as my long term investments as well. So I hold niftybees, juniorbees & MOM100 in 3:1:1. That’s all, no other investment in this category for pledging.

P.S. I deploy the margins in rather conservative strategies. In case I was doing some aggressive trades, would have liked to keep 10-15% of my trading capital as cash in savings account/ liquidbees.

Thank you so much neha for sharing so much details about the rates of interest from different banks, very informative indeed.

As you already noted, since this SB money cannot be used for the purpose of earning extra income by using pledge method to get the trading margin, therefor I will not be keeping most of the amount into the SB accounts, going forward.

I have opened up an OD Account with the Bandhan Bank and it will be sufficient for my liquidity requirements. Rest all of the amount is to be invested into Various Funds from that excel sheet.

I appreciate your detailed reply. Thanks a lot.

PS: Are you not invested into any type of Mutual Funds etc. at all? What are your views on the Debt Funds, as they offer better returns then the Bank Accounts etc. and have got additional benefits as well.

Thank you so much @abcd5662 for sharing your practical insights in this regards. I am glad that we have some pretty common objectives, so your guidance will help me a lot.

You mentioned that you would prefer GSecs over Liquid Funds, could you please explain as to why would you prefer them?

What kind of returns are you getting in these GSecs that you are holding?

And since your holding period is of 10-15 years, but I am not comfortable in making a commitment of more then 2-3 years at the max, then what would be a better option for me in this regards, Gsecs or Debt Funds?

Can I easily sell the Gsecs whenever I want, just like I can do with the Debt Funds, or if I will have to hold these Gsecs till their maturity?

And in your Non Cash Holdings, you have kept almost all the amount in the ETF categories. Any special reason for this? Are you not interested/impressed by the returns of other type of Mutual Funds or what?

Regarding doing the trading in aggressive manner, yes I would also like to keep atleast 10 % of my trading capital in the form of cash, so as to easily meet any MTM requirements on a day to day basis.