First off, I want to say a massive thank you for the effort you guys put into The Daily Brief. The depth of research is fantastic and as a reader I genuinely love getting this information to help navigate the markets.

However I wanted to share a pain point from the perspective of a daily consumer and that is the articles are currently too long for a daily format and the repetitive text creates unnecessary friction.

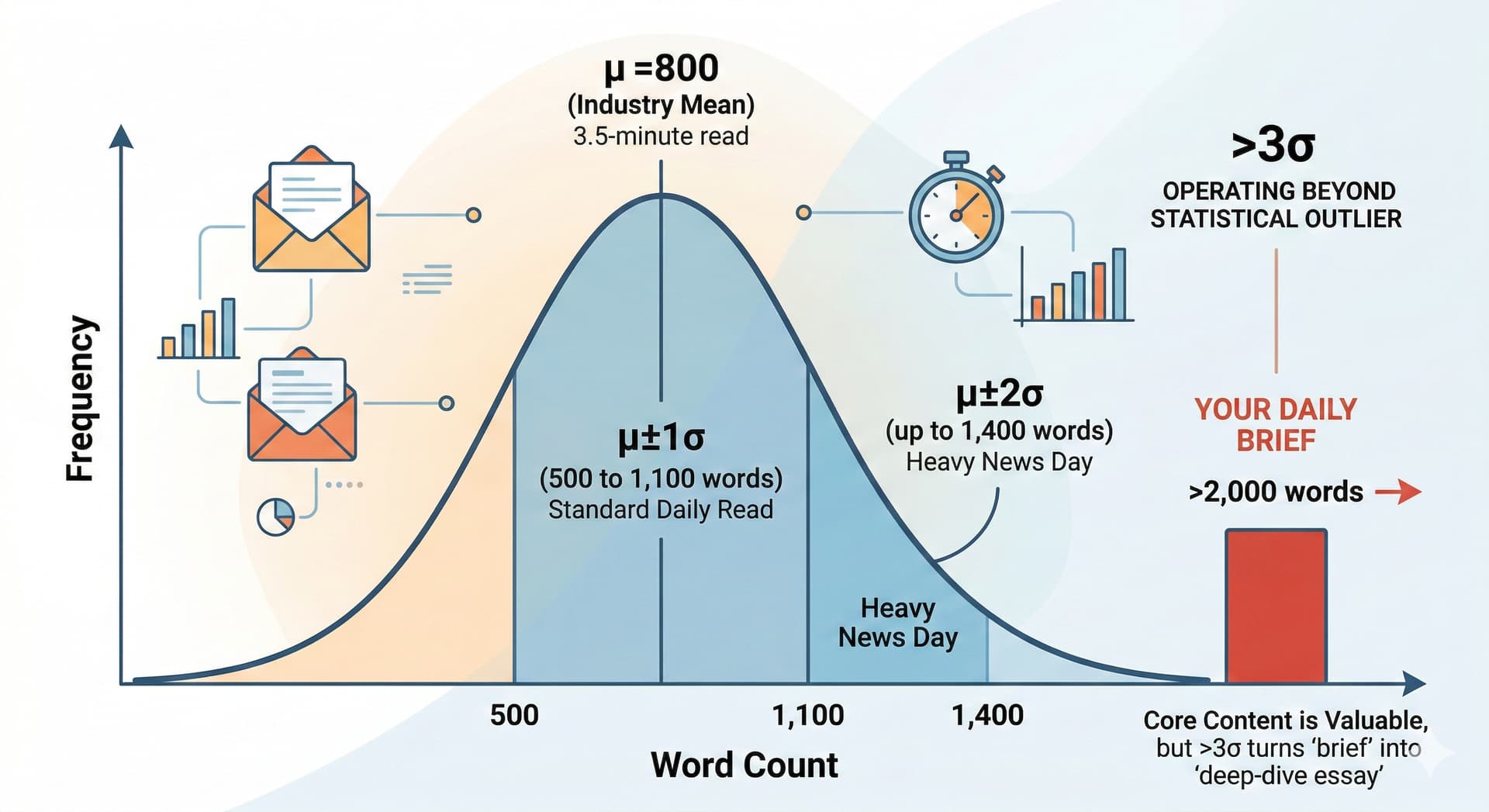

To put the length into statistical terms,

If we look at the normal distribution of an optimal daily newsletter’s word count, say x be the number of words. The comfortable industry mean (μ) is usually around 800 words (i.e. about a 3.5-minute read), with a standard deviation (σ) of about 300 words.

So a standard daily read falls within one standard deviation of the mean μ±1σ (500 to 1,100 words). A heavy news day might push to μ±2σ (up to 1,400 words). Right now, your Daily Brief is consistently operating beyond 3σ (often 2,000+ words). It is a statistical outlier. While the core content is highly valuable, a >3σ word count turns a “brief” into a deep-dive essay, making it difficult to commit to reading every single morning.

Secondly, the static intro and outro boilerplate on every post is quite annoying. Every day readers have to scroll past the same text explaining the goal of the brief and the reminders about the podcast, youtube, and Hindi formats. Then at the very end there is another repetitive block of text pitching the whatsapp channel.

When you open the article daily, filtering through the exact same intro and outro to find the actual signal is frustrating. If readers value the content (like I do), they will naturally seek out your other platforms. A simple sign-off like “Written by X and Y” at the bottom is honestly all you need.

Sooo… trimming the word count and removing the daily boilerplate would itself make this the perfect daily read. Below I also suggest a few more actionable ideas:

-

Trim the article to a target of 800 words (max 800 + 300 words). Don’t believe me, believe stats.

-

Remove all static intro and outro boilerplate, sharing prompts, and socials. Just use one line at the end: By XYZ, Zerodha. Subscribe: link. Thats it.

-

Ask AI to give you a “financial newspaper opinion article headline (Mint / FT style, 10–15 words, aligned with the article type) and a subtitle (12–20 words, sharp and consistent with the stance). Something like that.”

-

Include 2 to 3 AI images in between the article sections to break up the text.

Your email delivery should look like this: In our inbox, we should see just the ‘Title’ in the subject line (no “The Daily Brief” or dates) - trust me traders/investors will definitely click it early morning if it is something related to the market. Inside the email start with a title/subtitle or TL;DR if you want to, then the article and at the end just the one line sign off and subscribe link.

Implement this and you will see your readership grow more than ever. Most importantly your readers will enjoy it more.

data scientist,

yours,

livepositionaltrader