Hi all,

I’m to understand why Financing Profit/Margin is negative for a lot of banks.

Here is the example of Kotak Mahindra Bank. Why is the Other Income value so high as well?

Thanks!

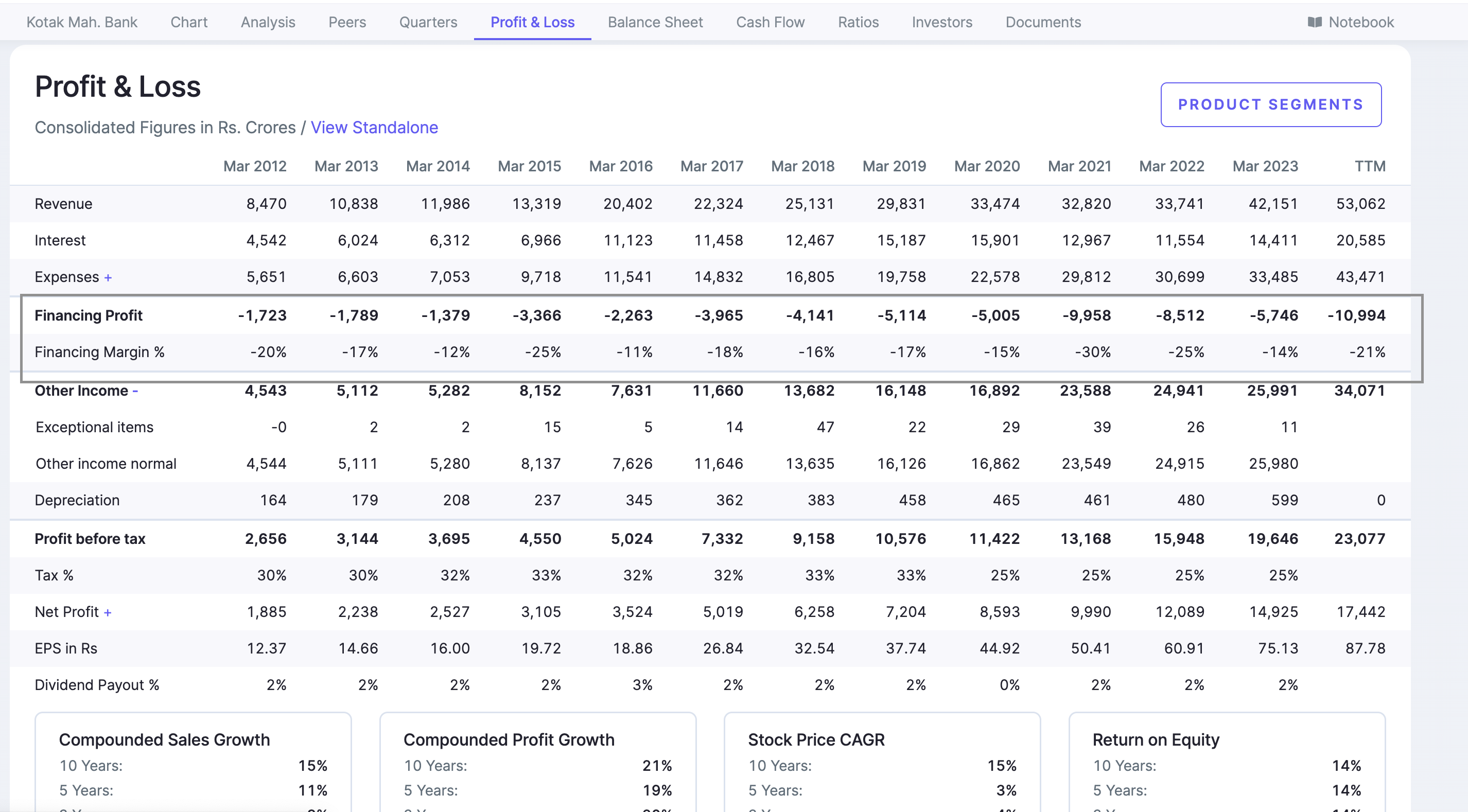

Hi all,

I’m to understand why Financing Profit/Margin is negative for a lot of banks.

Here is the example of Kotak Mahindra Bank. Why is the Other Income value so high as well?

Thanks!

Hi @tarun2

I’m sharing my colleague @Vineet_Rajani’s thoughts on this topic

Negative finance profit is basically finance cost. It’s the interest paid on borrowings. You will see that interest income is positive. The real metric you should be looking at is Net Interest Margin (NIM), that is Interest Expense minus finance cost. NIM is positive here as well.

Just looking at one year’s financing margin may not be helpful. But if you look at historical data like the screenshot in this post, a reducing margin would suggest perhaps the bank is enjoying a lower cost of borrowing. A comparison with other banks could be helpful too.

PS: Financing profit is not a term that anyone else apart from Screener is using.

As per my knowledge, This includes fees, commissions, profits on sale of investments, profit or loss on account of revaluation of investments, recovery in write-off loans, and dividends received from bank subsidiaries or other associates and this generally is a substantial part of banks income not only in the present but also was the case in the past.

This was in 2021