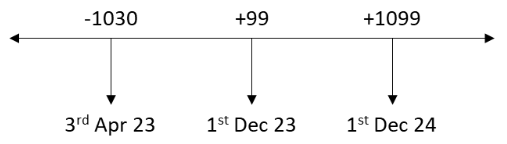

The IFCI-NH NCD has a yield of 9.90% and a face value of Rs. 1000. The date of maturity of the NCD is 1st December, 2024 and the payable interest is annually. This essentially means that the holder of the NCD will receive an interest of Rs. 99 on every NCD held every year until maturity. The cash flow of the NCD appears as below

The XIRR of the cash flow is 10.04%.

The NCDs are rated as “AA-/Stable” by Brickwork & “A/Stable” by ICRA. It is important to note that IFCI is a Government of India undertaking and the state holds around 66% share in IFCI.

This is not investment advice, just information. Do your research well before investing.

IFCI Ltd. appears to be an NBFC.

Though one that is a PSU as well.

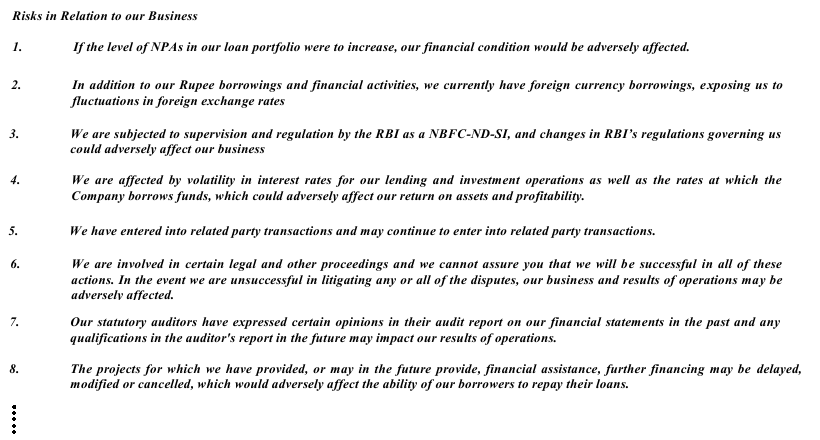

Reviewing the prospectus of the bond [1][2],

it mentions all the typical risk factors that a NBFC faces. (Refer to Section II Risk Factors of the shelf prospectus [2] that lists about 60 of them)

This is a listed entity. The promoter is Government of India - 66.4%. Hence by default it will be considered sovereign. The bond was originally issued in 2014 and maturing in 2024

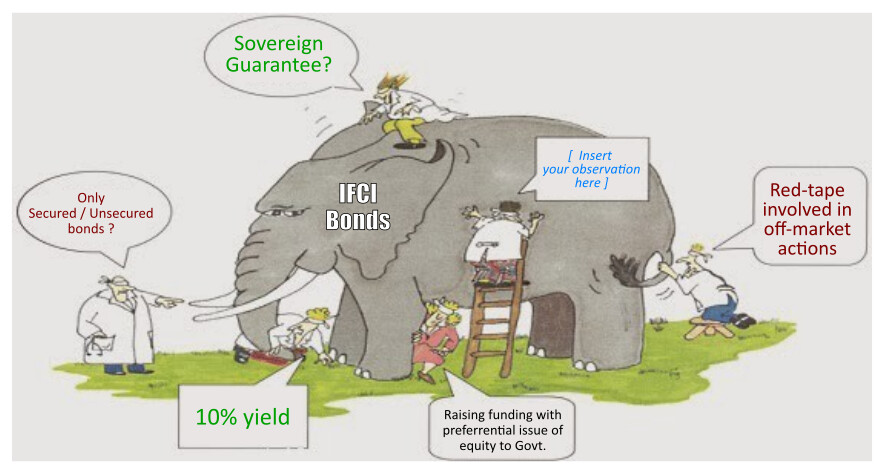

Are there any new NCD being issued afresh. Being a NBFC, they need to roll over the existing ones. Went through their website and could not find any new issues. Are you aware of any new issues

Did some more digging online.

the only mention of any “Sovereign guarantee” associated with these IFCI bonds i could find is…

The different guarantees given by the Union Government are as follows:

Guarantees given to RBIs, other banks and Financial Institutions (like IFCI, LIC, UTI etc) for repayment of principal and payment of interest, cash credit facility, financing seasonal agricultural operations, and for providing working capital in respect of companies, corporations, cooperative societies and cooperative banks

…

What this means is they have additional set of regulations to comply with.

Presumably this ensures better governance/regulation and implies lesser risks compared to typical NBFCs.

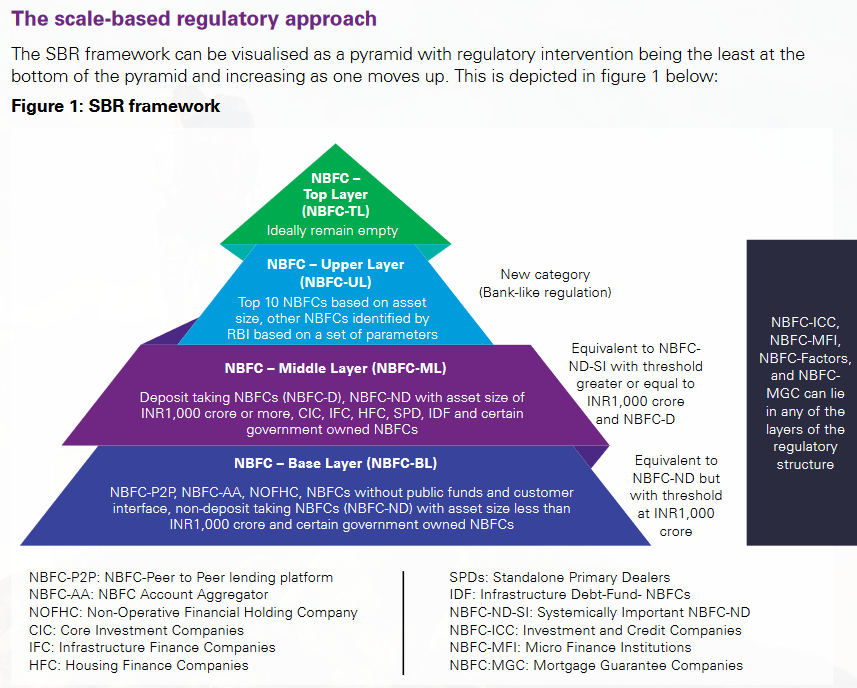

A somewhat recent development that may prove to be a twist in the tale

is RBI’s introduction of Scale-Based Regulatory approach (SBR)

which minimizes additional regulation on NBFCs with lesser net asset value. (IIUC, IFCI appears to fall under NBFC-BL / NBFC-ML with minimal regulations)

More than 18 months left for the current tranche of bonds to mature (DEC 2024).

Not sure if there will be another IFCI bond IPO in the near future 2023/24.

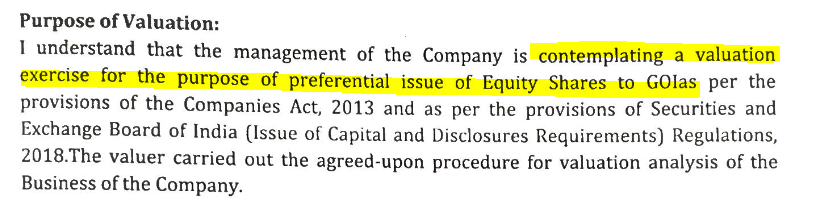

Currently, IFCI appears to be planning to raise money by a preferential issue without involving the public.

Guys, the bond is been downgraded to B+ rating because of its poor financial health. Thats the reason it is trading at 10% else no PSU bond is traded at such high yields.

Sovereign bond means RBI is issuing the bonds and Rbi is responsible for its payment.

Ifci bonds are secured , they are not sovreign

Sharing here my miserable experience with IFCI bonds -

I had invested in infra bonds offered by IFCI in 2010 or so… (remember that extra 20k tax deduction option for long term infra bonds under Sec 80CCF during Chidambaram’s tenure? it was discontinued from FY12-13. I invested in 2 FYs back then - one of them was IFCI.) Was a nightmare getting back my own money. I opted for annual interest (rates weren’t bad), and yearly interest was credited to my bank account on time.

In Oct 2018, I opted for their buyback option (no online option for buyback form submission, compulsorily send it only & only by speed post to RTA address)… followed up on phone call to check if they have recd my form. Guess what? the call centre guys at Karvy (RTA) denied receiving my form… I mailed the speed post recpt + scanned copy of the filled in signed form. They insisted i re-send. I re-sent. Again not recd by them. But imagine my horror when the bonds were debited from my demat towards extinguishment in Jan 2019 (meaning they exercised the buyback option in Dec 2018) & there was still no sign of the money. I have all ping pong trailmails over 6 months. IFCI also refused to help. In fact so badly run (classic babudom redtape) that they wouldn’t respond for months to my mails & nobody picks calls… & of course Karvy as RTA is no better. Eventually I lodged a complaint with SEBI SCORES after which i got the NEFT credit but without penal interest for not crediting on time.

Moral of the story: Keep a close eye on bond extinguishment debits from demat ac & cross-check if your bank ac has been credited for the same. It was a small amount I know but nevertheless hard earned money.

Agreed. When I said sovereign I meant that since it is owned by Government of India, there is a implicit understanding that Government will not default on its bond payment and will honor it. Yes they could let a company go down the drain, but then, Govt will lose it credibility especially when it comes to payment of bond holders.

I saw on their website two of their series IV bonds having coupon rate of 10.70%

To the best of my knowledge this company is similar to ONGC or other PSU where the company is managed and majority owned by Govt.

After reading @sufimonks real time experience, I will let it pass.

Thanks for the insight guys, really helps to understand the NCD in detail. What I understand is that the NCD is 100% secured with asset and Govt. of India Backing.

Reupping what I wrote about the recent amendment in taxation for interest income on listed NCDs this Budget. Beginning 1st April 2023, there is TDS on interest income (>5k pa) on all NCDs including those held in demat form. Earlier there was no TDS if NCDs were held in demat & it would not show up anywhere… It was up to ppl to disclose honestly while filing tax returns…

Of course he did, the classic blind men and the elephant story, where no one knows about the whole elephant but only knows what they touch, which in a sense is true too.