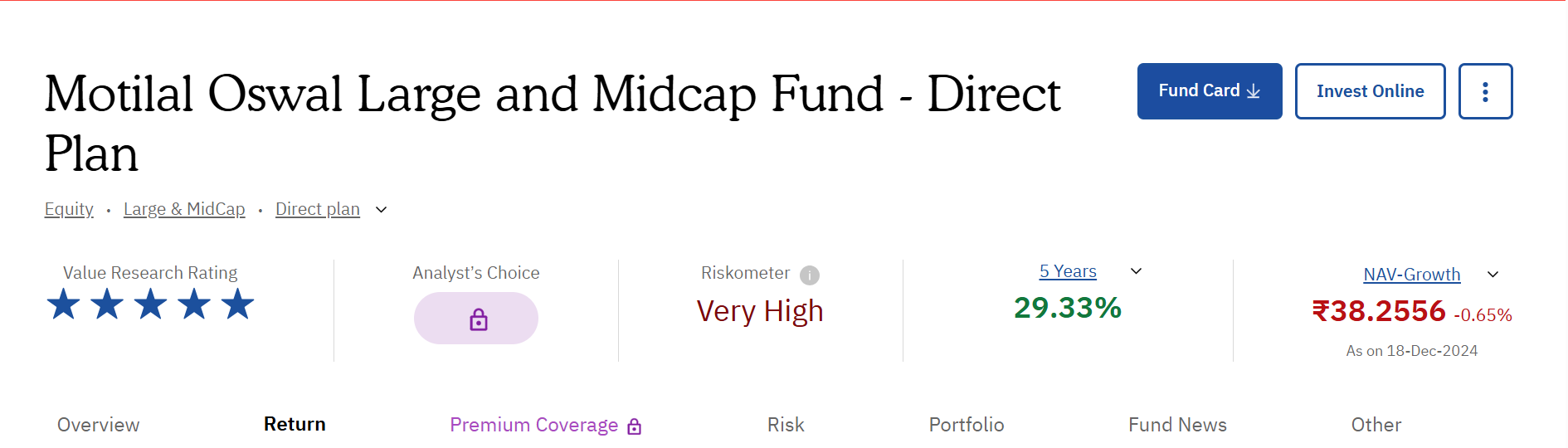

Motilal large and midcap fund

this fund is superior returns and super downward protection

i invested this - i will take for long term to next generation

any review

your review

The fund manager played very well in ups and down

Motilal large and midcap fund

this fund is superior returns and super downward protection

i invested this - i will take for long term to next generation

any review

your review

The fund manager played very well in ups and down

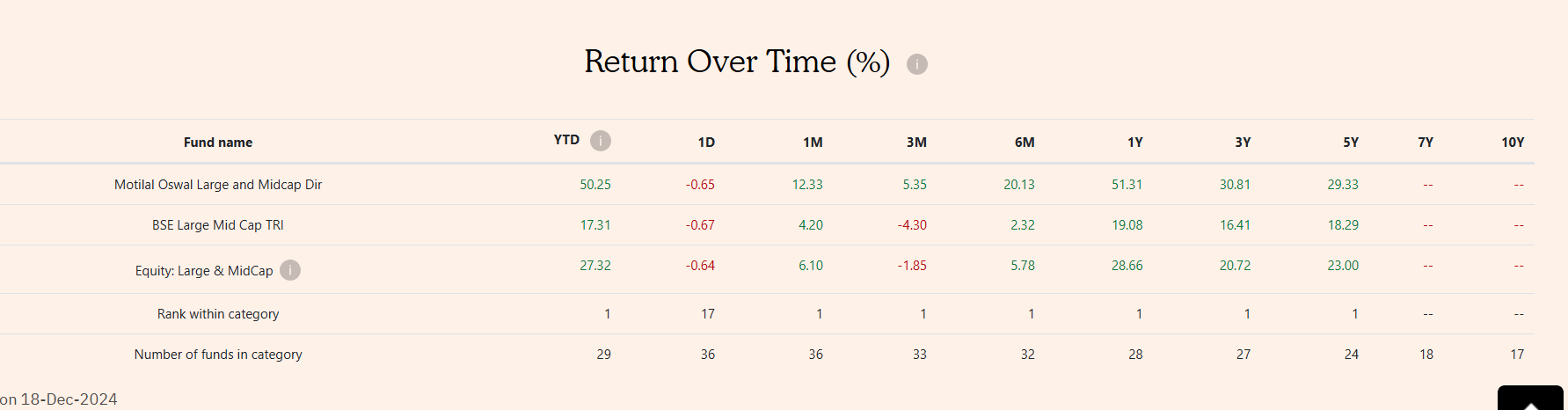

Can you elaborate specifically what suggests this about the fund ?

i still do not get how we go from any of these statistics to “super downward protection”.

For example,

if there was a chart comparing over the same time period

that might have been a justification for this claim of “downward protection”.

I don’t see that above or in the source page.

What else is involved in this “downward protection” ?

How to arrive at that conclusion from these stats? ![]()