I have recently joined Zerodha to give it a try.

First thing I noticed is the adding fund is not seamless like my HDFC Securities Demat & Trading account where the bank account is directly linked. Allow me to explain how adding funds to your Zerodha trading account incurrs loss to you in the long run.

Case 1:

Instant Transfer.

You want to transfer say 10,000 to your account, the instant transfer option costs you Rs 9+GST per transaction. Regardless of whether you add Rs 100 or Rs 1 Lakh, you will have to pay this extra cost.

You may counter my case by saying that why add money in small amounts, instead add a big chunk at a time and then this Rs 9+GST is affordable. But the point is in HDFC bank account your money is also earning interest @3.5% until it is invested. Whereas if you keep money in the Zerodha trading account, you don’t get any interest. So adding in bulk does not make sense.

If you add in small chunks as you need, you lose amount per transaction and TIME to execute that as well.

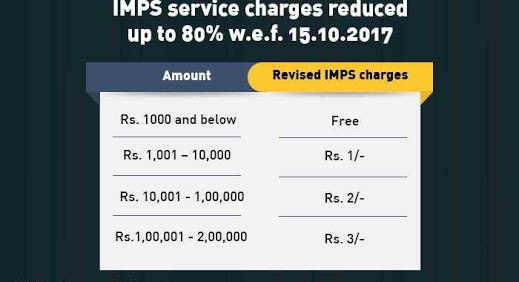

Case 2:

You choose to pay via NEFT or IMPS.

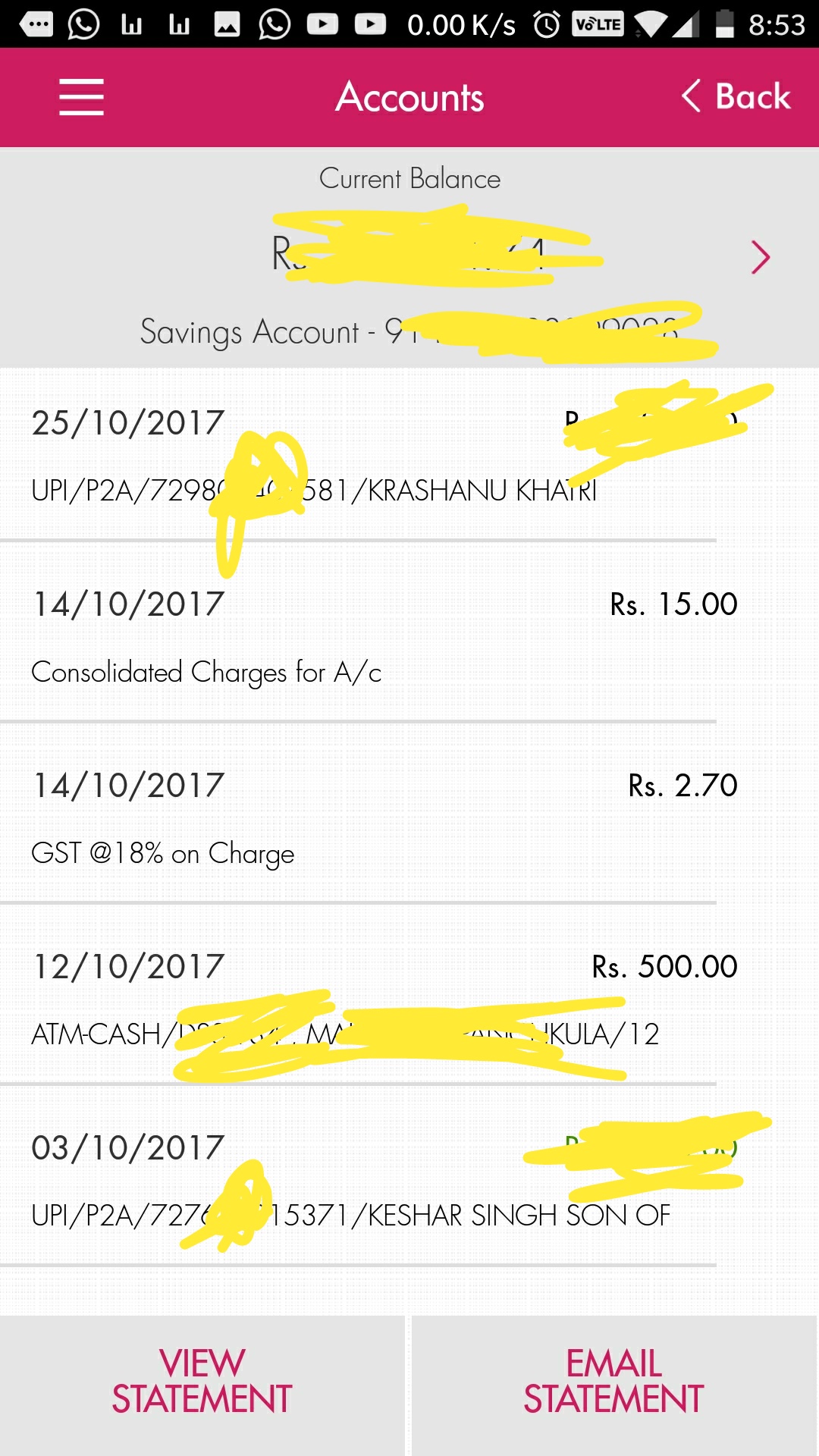

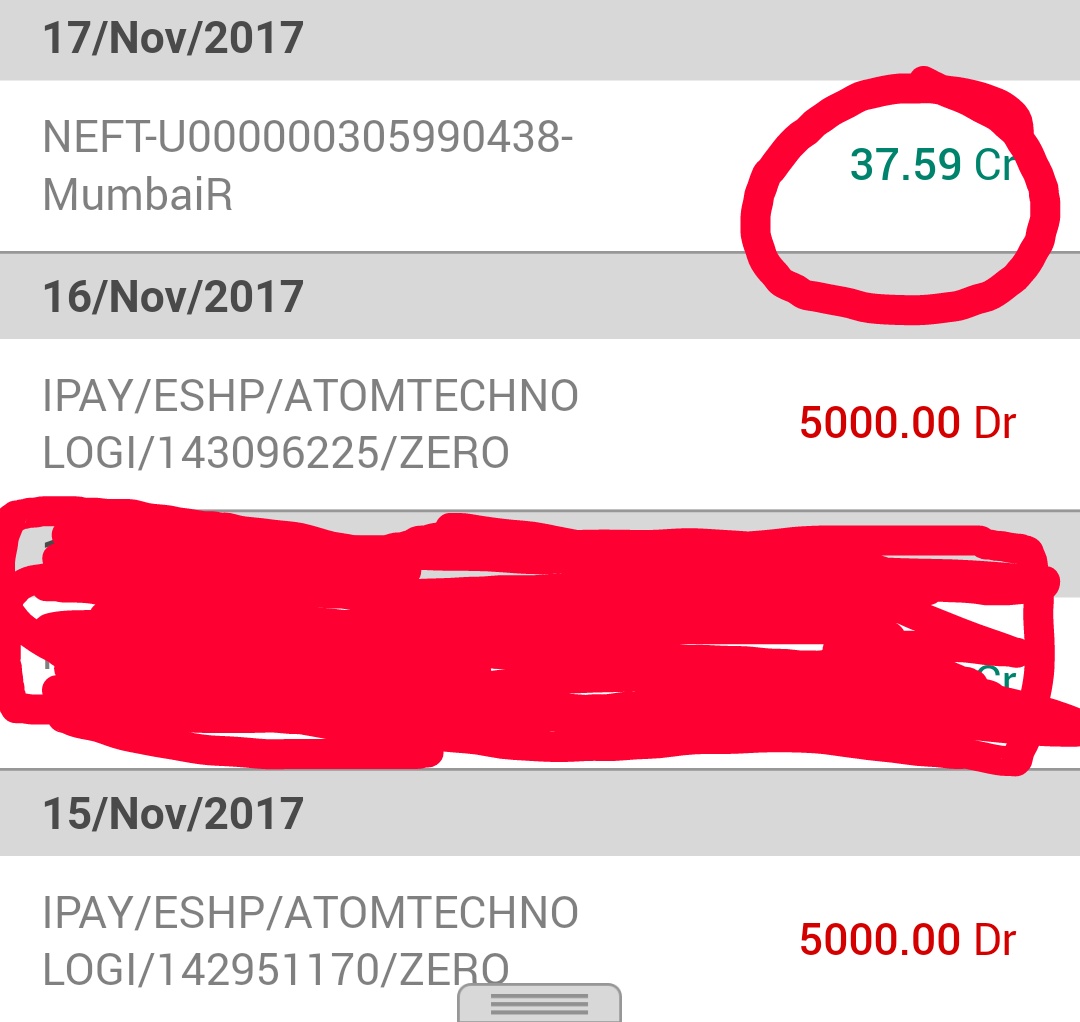

Same logic. If you transfer in bulk, you don’t lose on the interest until the fund is invested. And in you transfer on-demand or in small chunks, you pay extra for each transaction (to the bank as NEFT/ IMPS charges) and also lose time as NEFT/ IMPS transfer takes time. I had to send email to Zerodha with screenshot of the transaction details to get it credited in my trading amount.

Case 3:

You choose to do SIP in mutual funds through Zerodha Coin. Let say you have 5 mutual funds SIP of Rs 2000 each i.e. SIP of total 10,000 per month but at different dates. Say they are 2nd, 5th, 8th, 16th and 25th date of the month.

If you choose to transfer 10,000 to Zerodha trading account at one time in the beginning of the month, you lose on interest.

If you choose to manually transfer you lose money on each trasaction by paying additional transaction charges for each time. Also, you lose time to execute each transaction manually.

If you choose to do a bank standing instruction to Zerodha account 2 days before the said dates of SIP (to be on safer side), you lose bank interest for those 2 days for the said amount. Whereas if you have a trading account with your bank, then the amount earns you interest until invested as well as it is automatically deducted on the said day without fail and without any extra transaction charges.

You may contradict my arguement by stating that this much is “chalta hai” and i am over thinking. But I just gave you an example of Rs 10000 investment in a month. What if someone has a bigger portfolio and one who has multiple SIPs, going on. And consider these small small transaction charges, and the loss of bank interest and loss of time for executing mannual transactions for 15 odd years of investment period. It would definitely amount to a significant figure.

All in all, Loss of time and money in all the above cases. And Time is Money when it comes to Investment.

Hope Zerodha understands this and takes appropriate action.