Of late, we are already seeing side effects of the rampant growth in speculation with many options becoming 10-50x within minutes and we are getting to see lot of freak trades with options spiking a lot without any major move in the indices. One can only imagine what will happen once markets become volatile and the speculation remains intact.

Axis mutual fund shared these interesting charts :-

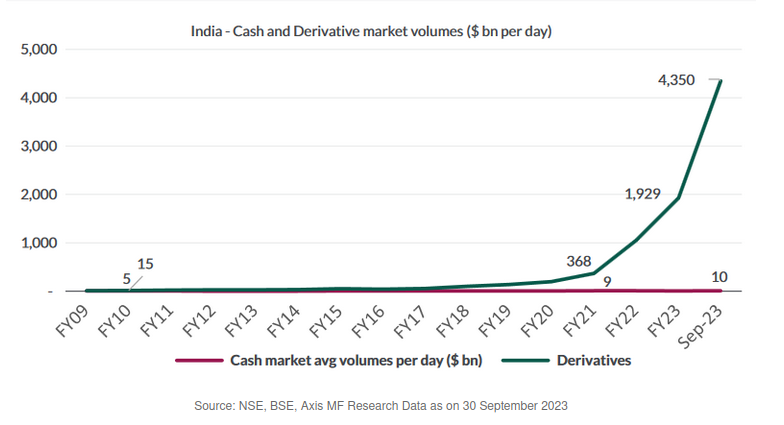

Derivative volumes

-

Total derivatives volumes have risen to over US$4.3tn per day roughly translating to 125% of the underlying companies’ market capitalization or over 200% of its free float being traded every day.

-

In the US, derivatives account for 70% of traded volumes, compared to 99.6% currently for the Indian markets.

- Of the over 5,000 companies listed in India, derivatives contracts are available for 193 stocks and indices. For these, there are ~46,000 individual contracts available at any point spanning products (futures, options), tenor and strike prices. Index options reign supreme accounting for 98% of total derivative volumes.

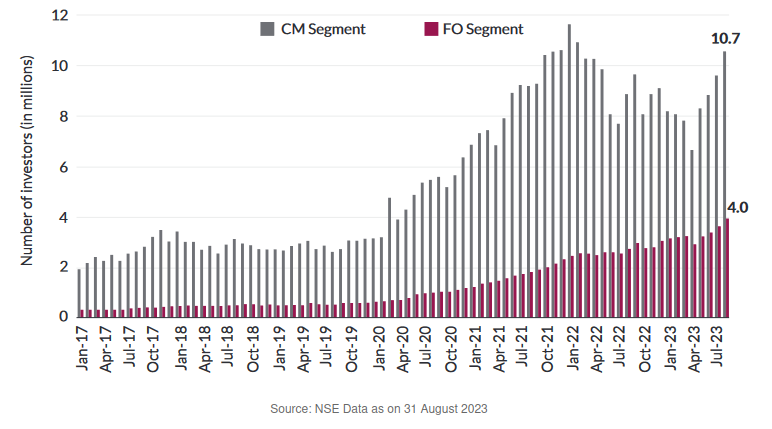

Number of derivative traders is up by 8x, while cash market traders is up by 3x

- Number of active derivatives traders jumping 8 times to 4 mn from less than 0.5m in 2019. In comparison, in the cash market, the number has grown 3 times - from ~3mn in 2019 to 11 mn.

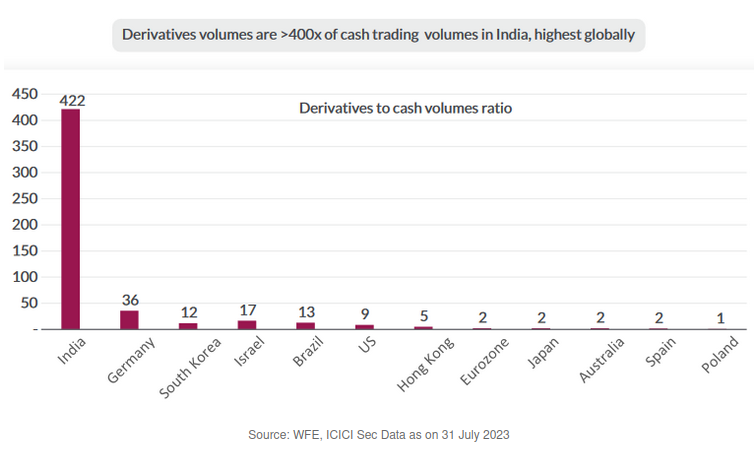

- In most markets, derivatives volumes now account for 5-15x their cash market volumes. In India today however, derivative volumes are more than 400x higher than that of underlying cash market today, having grown from 3x in 2010.

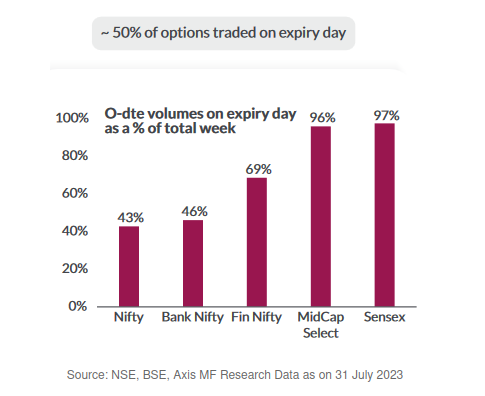

Expiry day (Odte options) volumes

-

Introduction of weekly expires on every day of the week has enable zero day to expiry volumes to spike up like how it is in US markets. In the US, zero day to expiry options now constitutes 55% of S&P 500 volumes.

-

Open interest at the end of the day is only 1% of the daily traded volumes, i.e. only 1 out of 100 contracts are carried forward to the next day. Retailer’s option trading is also largely speculative given the average holding period of less than 30 mins. This indicates how speculation is surging at an exponential rate.

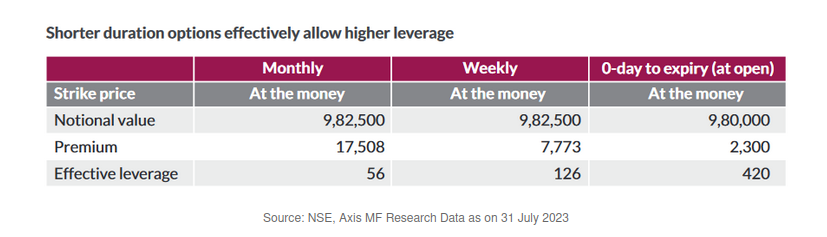

Shorter duration options enable higher leverage !!

- Nifty’s ATM weekly contract is available at 40% of the cost of a monthly contract while offering the same notional value. This effectively increases leverage to 126x, from the 56x leverage offered by monthly contracts. In the case of zero-day-to-expiry options, leverage increases further to an astonishing 420x.