Hi

Glit mutual funds are safe like buying Indian government GSEC bonds directly ?

Please guide @VishalJain

Hi

Glit mutual funds are safe like buying Indian government GSEC bonds directly ?

Please guide @VishalJain

it would be great if can buy gilt funds and other funds directly from zerodha ledger balance. its too much hassle to withdraw to bank account, buy via coin, get credit in 1-2 days then pledge it again. money tied up 4-5 days like this

Yes, safer in terms of limited credit risk as underlying is sovereign. However, price risk is there depends on the underlying duration the portfolio.

On a credit risk perspective absolutely safe. Better than bank fd as it is issued by central govt

Can u please explain. What is coin… is it crypto currency?

With added risks associated with an intermediary “middle-man”.

Since, technically one doesn’t hold the Govt. securities,

but a 3rd-party “middle-man’s” scrip that is supposed to be (and almost always is) backed by govt securities.

If using Zerodha,

https://coin.zerodha.com/ is the app/site/portal

to invest in few other instruments apart from stocks.

Did not understand. Irrespective of the intermediaries, govt is obliged to settle on due date

I understand the experience in this case. But as per SEBI regulations, mutual fund purchases have to be made directly from your bank account, not from the funds in trading account.

…obliged to settle with the “middle-man” Gilt fund that had invested in the GSECs,

not with the individual who wanted exposure to GSECs via the Gilt fund.

The individual holding the units of a Gilt fund,

a. is trusting the guarantee of the sovereign that the Gilt fund invests in.

b. is also trusting the intermediary that has issued these units of Gilt fund.

IMHO, in a relatively well-regulated market, the above (b) is a minimal amount of additional risk. But, the risk is non-zero, however minuscule it might be.

With how easy it has been to directly invest in GSECs/SDLs/T-Bills in recent times,

IMHO there is very little reason# to invest in Gilt funds to get exposure to GSECs,

instead of investing in GSECs directly.

gsecs i think give regular interest and will expire. So more regular taxes on slab.

With MF i can keep holding and let it compound. Real rates are anyway very low, taxes will probably make them negative.

I also see people complaining around gsec pledging, only applies to traders.

Not sure about gsec liquidity for retail.

In return we do have MF expenses, but taxes will more than nullify that i think. I try to use low expense options wherever possible. Don’t remember about gsec ones. I havent invested in them, but we have gsec fixed maturity index funds with least expenses from what i remember ( But they expire ).

For me, i don’t see any reason to invest directly.

But probably ok if income is below tax limit, maybe one can avoid expenses that way.

Great point about the flexibility GILT funds offer to the individual

on when exactly one wishes to book income/profit, ![]()

(compared to GSECs requiring planning while investing in them, and accepting periodic income)

Yes, in one line, that’s it.

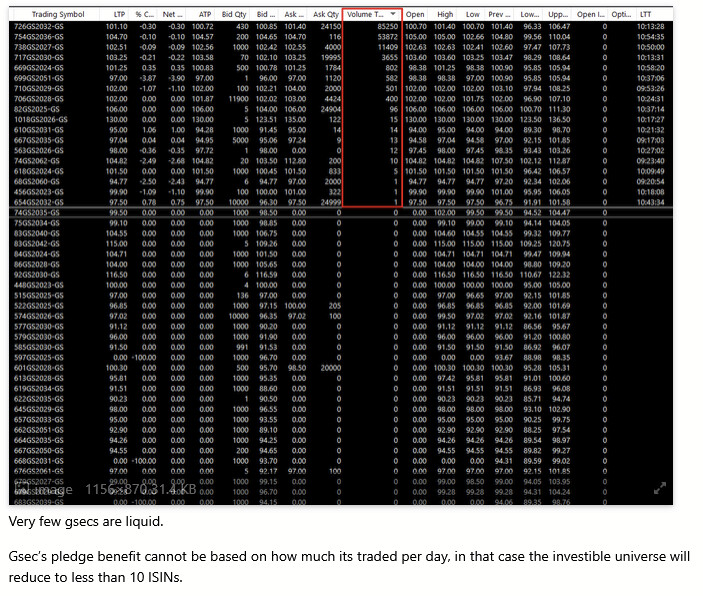

For the past 5 years, it has been several crores of INR available on BSE/NSE on a daily basis.

However, at any exact moment on any given day,

which of the numerous GSECs is going to be liquid is anyone’s guess.

Here’s a snapshot at one specific instant of time (presumably in SEP 2023).

At any given point of time,

there are ~100 outstanding GSECs with varying maturity, yield, and liquidity. ![]()

Add SDLs, T-Bills, and STRIPS into the mix (investments with extremely similar counterparty-risk),

and the number of scrips to monitor explodes to ~1500.

With slightly different attributes/properties between each of these classes.

IMHO, a key challenge is the lack of an intuitive user-interface around such sovereign bonds.

Some brokers provide better user interface to manage this complexity, others don’t.

Here are a few examples of what is possible, but missing -

a. Quickly filtering and listing all GSECs, sorted by yield based on current ASK-price in NSE/BSE is supported by some brokers. giving the user the ability to pick a GSEC suited to their needs (returns, maturity, liquidity).

b. Being able to place a limit-order that is active for a month, along the lines of -

“Purchase upto INR 1Lac of any GSEC, SDL that offers an effective yield >9%, maturing between 3 and 10 years”

Am not aware of any broker that is focusing on providing an intuitive terminal for all of this.

However, with real-time market data API access, and a little bit of imagination/coding,

one can easily create custom terminals for this purpose for ourself.

(How do i know? I have built a couple such terminals for “personal use”.)

Hi can you explain me some of my query’s about Gsec , i am literally don’t know much about Gsec , i would like to buy some gsec having shorter tenure for the purpose of pledging for Trading margin as well as for some returns. Thing is that to know the Interest payment date is very difficult , if i buy Gsec on kite , is it feasible ? if yes at what price one should buy , for example 738GS2027 is trading at 104.50

Can refer to the steps described in 2 posts in this previous topic-thread here and here.

Asking around before getting involved in some scheme that one doesn’t fully understand.

Good timing! ![]()

![]()

You can start by reading about Bond Yield

and then this chapter on how one can calculate the yield of a GSEC bond,

and how interest payments are received from a GSEC.

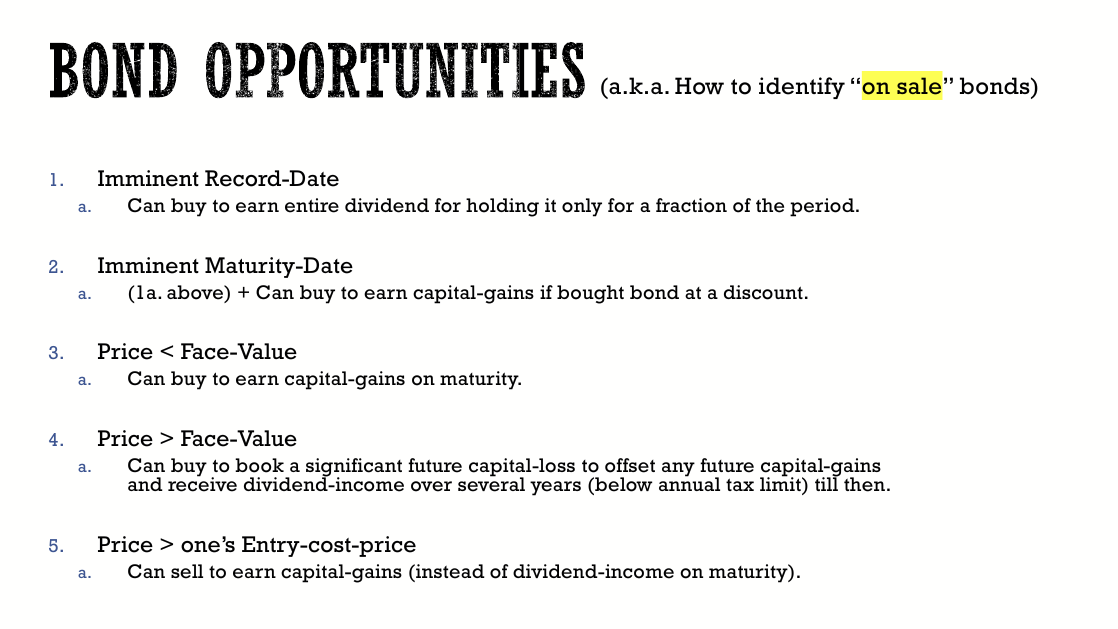

Apart from this,

just FYI here’s a quick summary of a few scenarios

to extract additional returns from investing in bonds through the secondary markets like NSE/BSE.

(in addition to receiving periodic interest on them)

( Not that you should explore them right away,

since you wish to invest in GSECs mainly for the “purpose of pledging for Trading margin”.

But, thought of sharing here, these few other possibilities surrounding GSECs (and bonds in general), since we are on the topic.)

9% is pretty high vs current 10y yield which is around 6.5% as per tradingview ( And falling fast ! ).

33% tax on this gives you 6% post tax, which is decent enough as gilt funds will give pre tax of around 6-6.5% depending on expense. And CG whenever we decide to book ( i don’t book at all for now and only book latest investment when needed )

Too much hassle for me for now, esp with uncertainty around pledging.

But nice to see this, you basically give liquidity to other people in illiquid market.

How much volume can you push ? This is esp good for people below tax limit. 9% long term tax free, will be good for retired folks definitely.

Thank You , I appreciate your patience & sincere effort to write here & explain , I think its really difficult to go through so many things , well definitely i will try , l think you are very well versed with Bonds& GSEc , Let me come to you regarding Gsec’s , if i have any doubt , The only thing stooping me to buy gsec not only for pleading but also as an Investment is , Interest payment date , i need to explore more on it.

Jump started to get some practical experience , bought just 100units of 738GS2027 GS ,

Between 2020-2025,

here’s the typical# experience based on asks/bids (in addition to trades)

of GSECs, T-Bills, and SDLs on NSE and BSE.

# - Sustained, extremely volatile market periods supported significantly higher volumes.

| Yield-range | The associated Liquidity, Volume, … |

|---|---|

| 6-8% | Several Crores of INR within seconds, 9 out of 10 days in the market. |

| 8-9% | Tens of Lacs of INR within an hour, most days in a week. |

| 9-10% | Lacs of INR within a day, on few days in a month. |

| 10-20% | Lacs of INR, for a few minutes each time, random times each month. |

The astute-minded individual will note that

even though there are instances of double-digit returns even in sovereign bonds,

to successfully act in such scenarios,

one needs to hold the capital without deploying it for quite some time,

i.e. wait for several days at a time without earning anything on the capital.

So,

while a ~0.5% actual return on a T-Bill in a week

(buy it at 99.50 INR, matures at 100 INR in a week)

yields us ~25% annualized rate of return,

while waiting for such an opportunity to arise,

having to hold the capital in one’s trading account a month without deploying it,

makes it effectively earn a “0.5% return in a month” i.e. a ~6% annualized return.

Markets vary over time, and success requires planning and patience in this market as well.

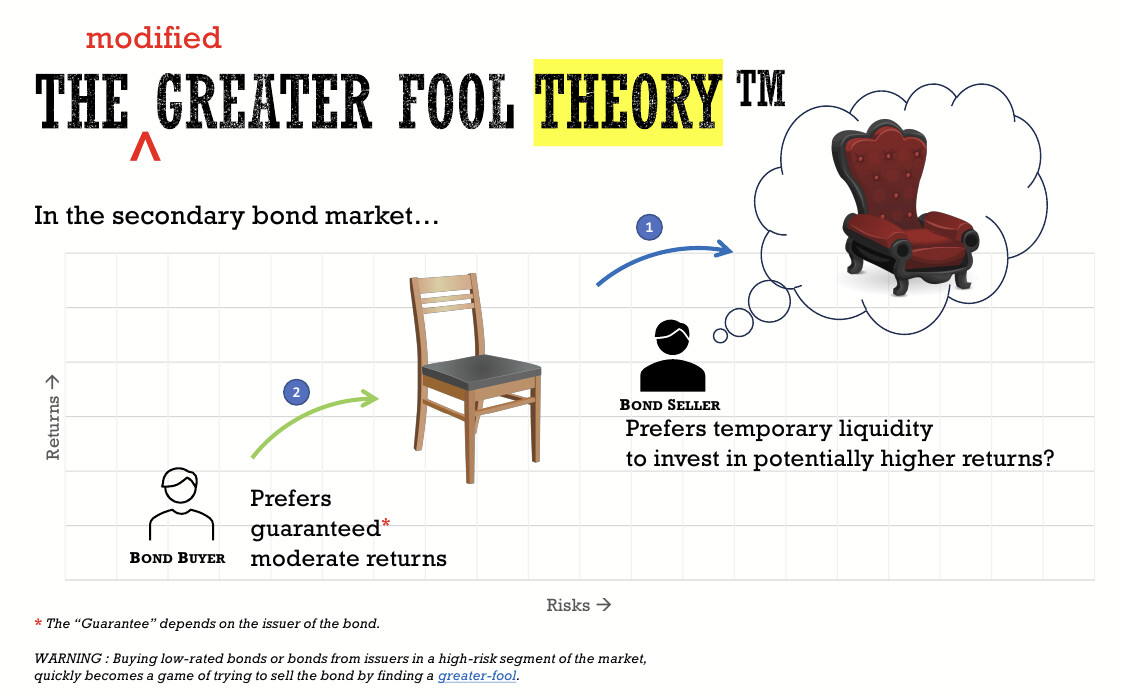

From memory, i can recall a 96% yield on a sovereign bond, ![]()

(purchased a T-bill at 95INR which matured at 100INR in 20days)

during a period of extreme volatility in the stock market,

when sovereign bonds were also trading at deep discounts on their face-value.

Here’s how a game of “musical chairs” played out in the bond market…

During the volatile period,

presumably, several individuals/institutions that held GSECs/SDLs/T-Bills

were liquidating them on NSE/BSE,

to immediately re-invest the proceeds into some “solid stock”

that had dropped to an all time low in the turbulent market.

As a bond buyer in such market scenarios,

one is “selling liquidity” at a premium

and can charge handsomely for it. ![]()

(all with near-zero credit-risk if buying sovereign bonds)

Determining whether it is ethical behavior to

support/enable such “greater fools” to take risks in a volatile market,

is left as an exercise for the reader ![]()

OK. Welcome to the bond club. ![]()

Now tell us…

Based on the price that you purchased it at,

Q1. Upon maturity of the bond,

a. How much capital-loss will be incurred, and in which financial year?

b. Will it be STCL or LTCL?

Q2. Describe the income-stream associated with this asset.

a. Periodically, how much interest will be credited

to the bank-account linked to the demat account holding this GSEC?

b. How many such instances over the next 2-3 years?

c. and exactly when all? (dates)

Q3. What is the effective yield % ?

(Note: All information necessary to calculate the answers to these Qs,

is available in the links discussed above in this topic thread)

I initiated this topic in the sense of capital safety.

Buy Glit fund is safe as buying GSEC ?

Investors please share your experience.