Hello and welcome to Beyond the Charts! A newsletter where we dive into fascinating charts from the world of finance and the economy, breaking down what’s happening in a way that’s easy to understand.

If you prefer watching video over reading, you can watch the episode here:

Global economy

In the last edition, we looked at a bunch of high-frequency indicators to get a sense of how the Indian economy is doing. The short version? The Indian economy seems to be losing a bit of steam lately. If you missed it, you can read it here.

This time, we’re shifting gears to focus on the global economy, starting with the United States. After all, it’s the world’s largest economy, and when the US sneezes, the rest of the world catches a cold. In the next few editions, we’ll also dive into Europe, China, and other major economies.

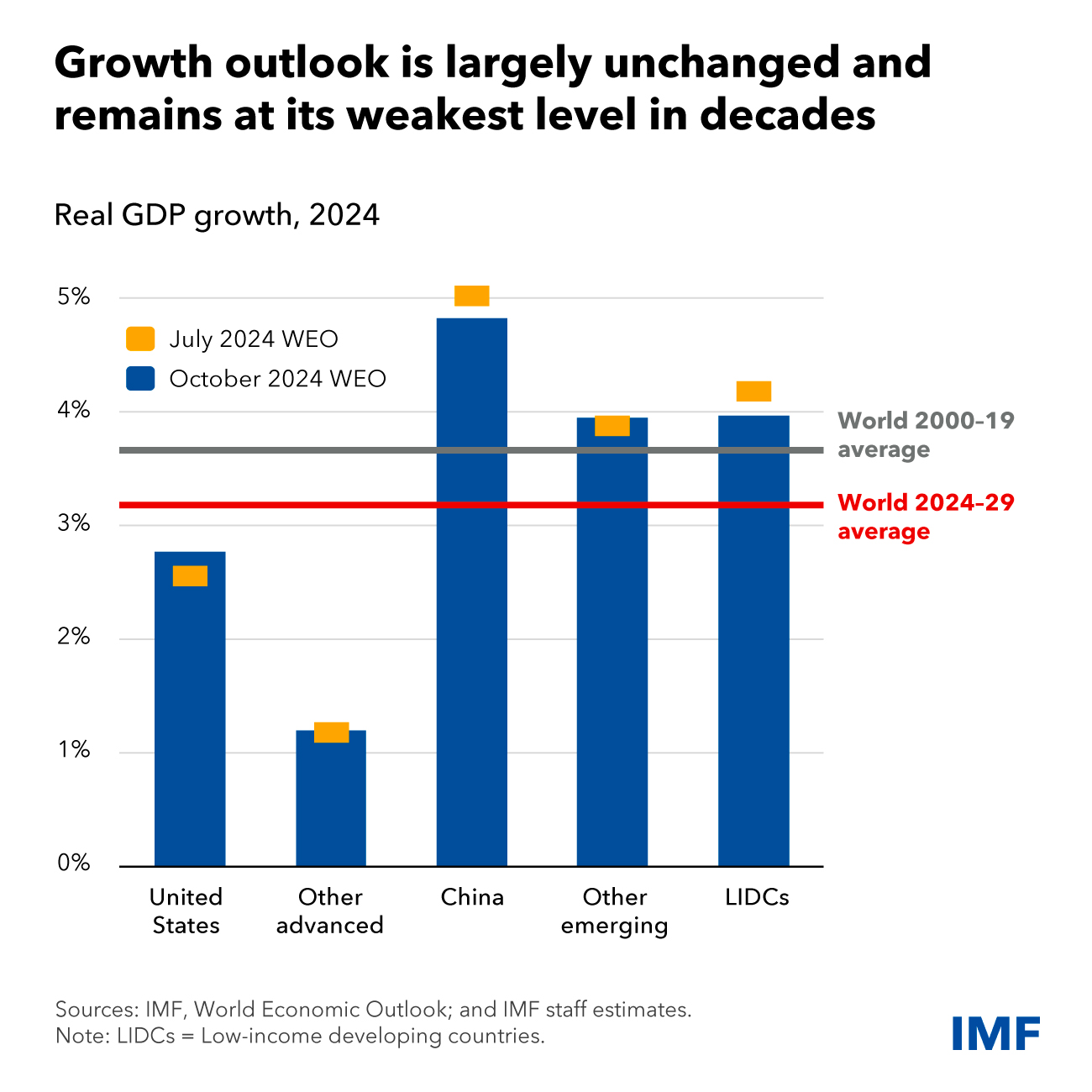

But for now, let’s start with the global picture before zooming in on the US. In October, the International Monetary Fund (IMF) shared its latest world economic outlook. According to the report, the global economy is settling into a phase of steady but not-so-impressive growth.

The IMF expects global GDP to grow by 3.2% in 2024. That number hasn’t really changed much from its earlier updates in April 2024 or October 2023. And looking ahead to 2029, the IMF predicts growth will stick to this same 3% range.

Source: IMF

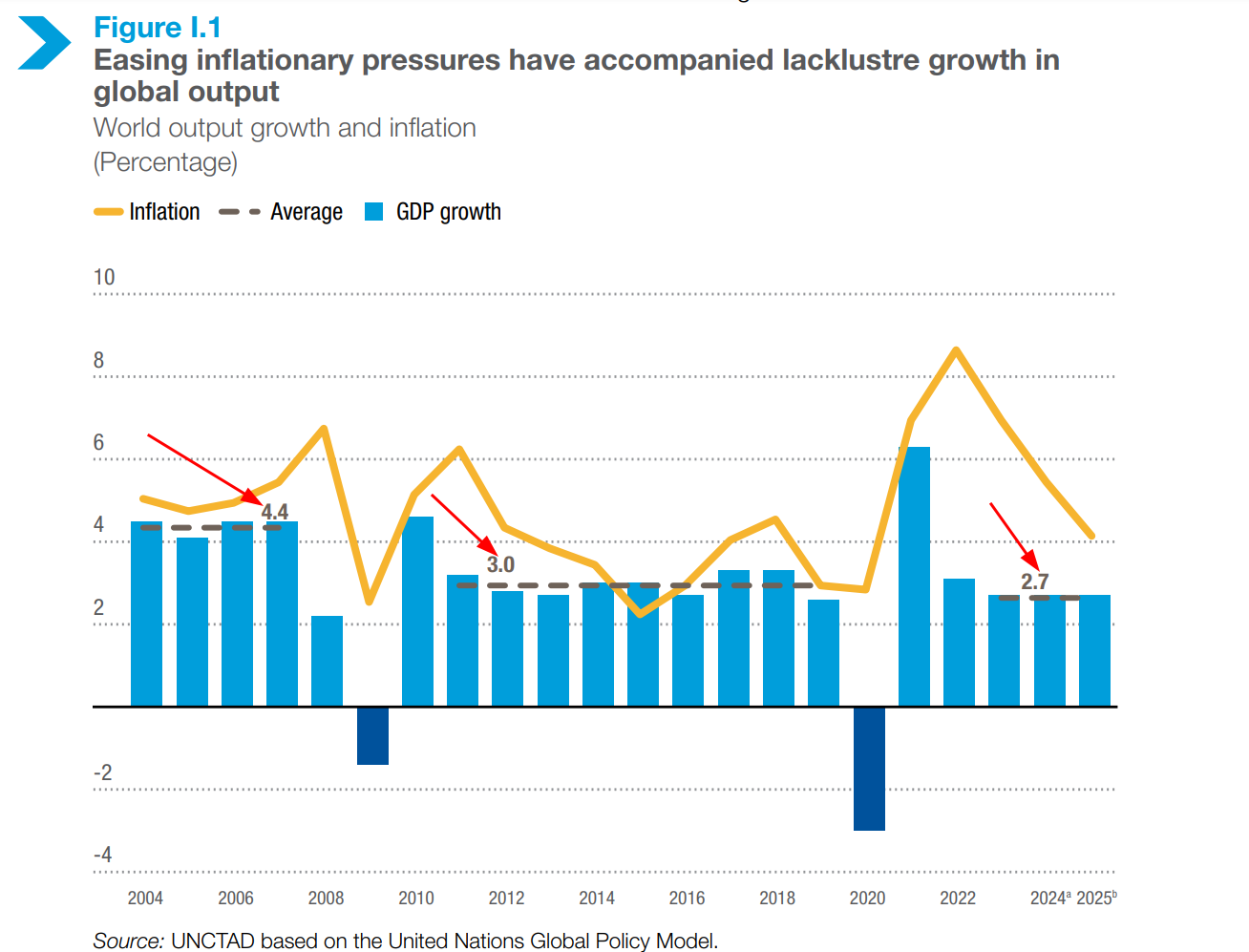

What’s really interesting is how the global economy’s growth rate has been trending over the years. Before the 2008 global financial crisis, the world was growing at an average rate of 4.4%. Then, between 2011 and 2019, it slowed down to 3%. And now? It’s dipped even further to an average of 2.7%.

Source: UNCATD

So, why is the global economy slowing down? It mostly comes down to three key reasons:

First, businesses aren’t running as efficiently as they could. The right talent and resources aren’t always reaching the companies that need them the most.

Second, many countries are dealing with aging populations, which means fewer people of working age. By 2030, the growth in the global workforce is expected to be just a third of what it was a decade ago.

Third, ever since the 2008 financial crisis, businesses have been hesitant to spend on growth. They’re unsure about the future and often face challenges in getting the funding they need.

Unless we see major changes in government policies or breakthroughs in technology—like AI—the global economy might struggle to grow beyond 3% by 2030. That’s a noticeable drop from the 3.8% growth we saw before COVID.

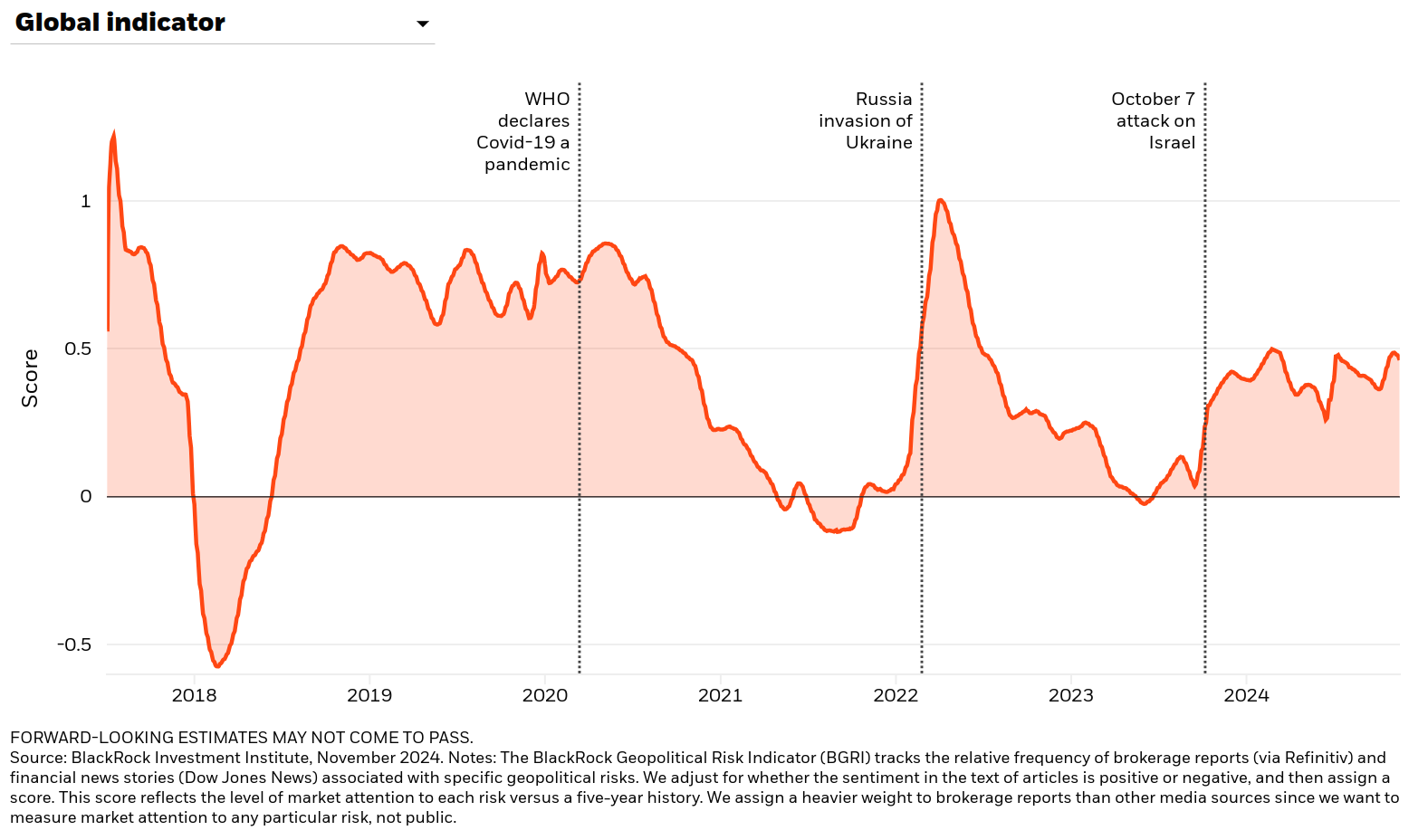

On top of this, just recently, India’s central bank pointed out that global growth has taken another hit, thanks to rising tensions between countries.

Source: Blackrock

On the bright side, the IMF points out that the strong push toward lowering inflation—known as disinflation—has started to ease. While inflation in goods has either stabilized or started coming down, inflation in services is still running high, mainly because wages continue to grow steadily.

Source: IMF

Source: RBI

With inflationary pressures varying across the globe, countries are taking different approaches to monetary policy. Most developed nations, except Japan, have started cutting their interest rates. But for growing economies like India and others, the situation is more complicated. Some of these countries have room to lower rates, but others can’t afford to, as inflation remains stubbornly high.

Take India, for example—it hasn’t cut its rates at all.

In simple terms, wealthier nations can relax their monetary policies as prices stabilize. Meanwhile, many emerging economies still need to stick with strict measures to keep rising prices under control.

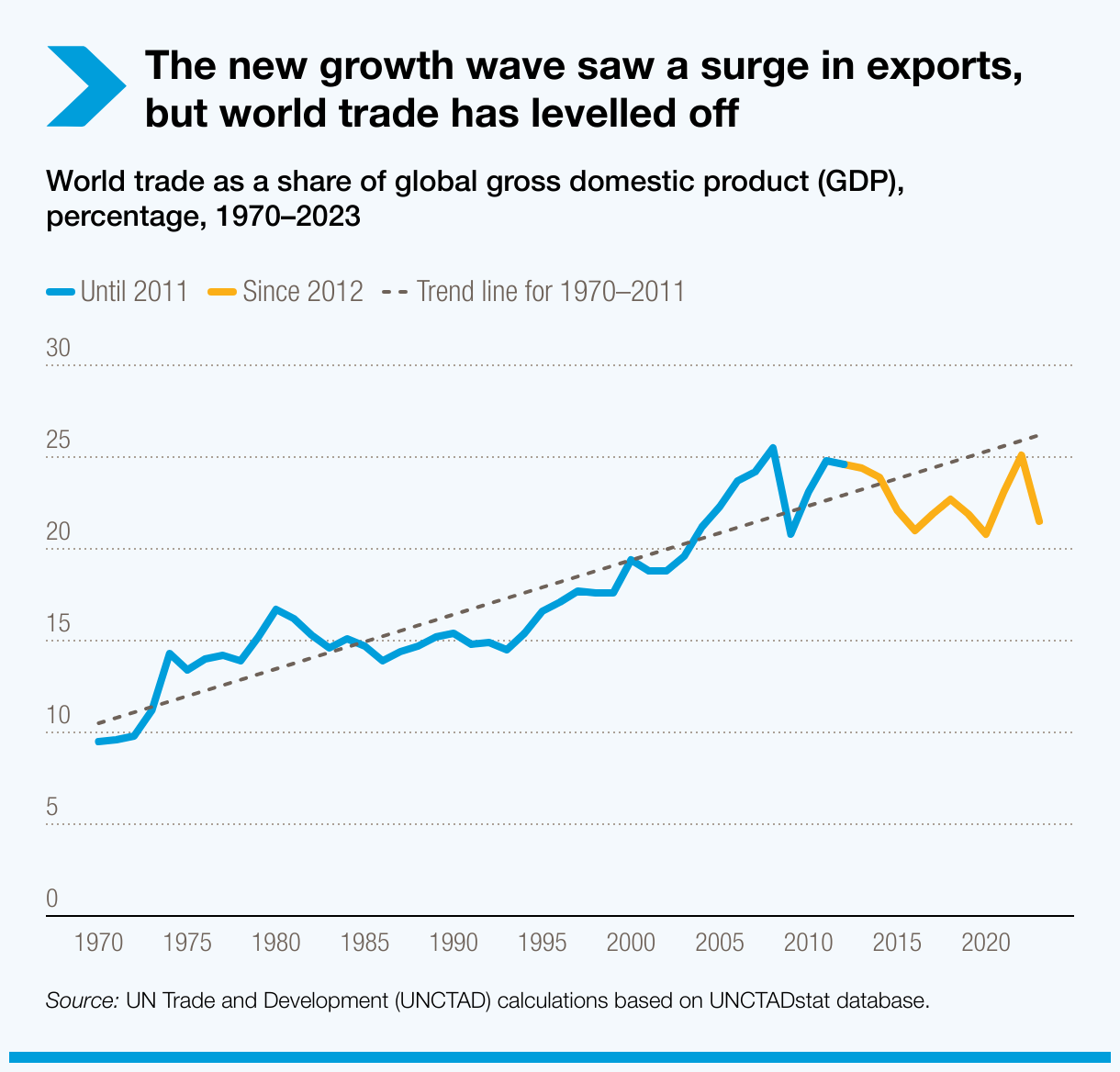

Another way to understand the state of the global economy is by looking at merchandise trade volumes—that’s the total amount of goods being traded across the world. According to the UN’s latest report, global trade is slowing down, with countries trading fewer goods than before.

A big reason for this drop is the struggles faced by European economies, especially Germany, Italy, and the UK. In fact, Europe as a whole is having a tough time economically, which is dragging down global trade.

Source: UNCATD

On the other hand, services trade between countries is also slowing down.

Source: UNCATD

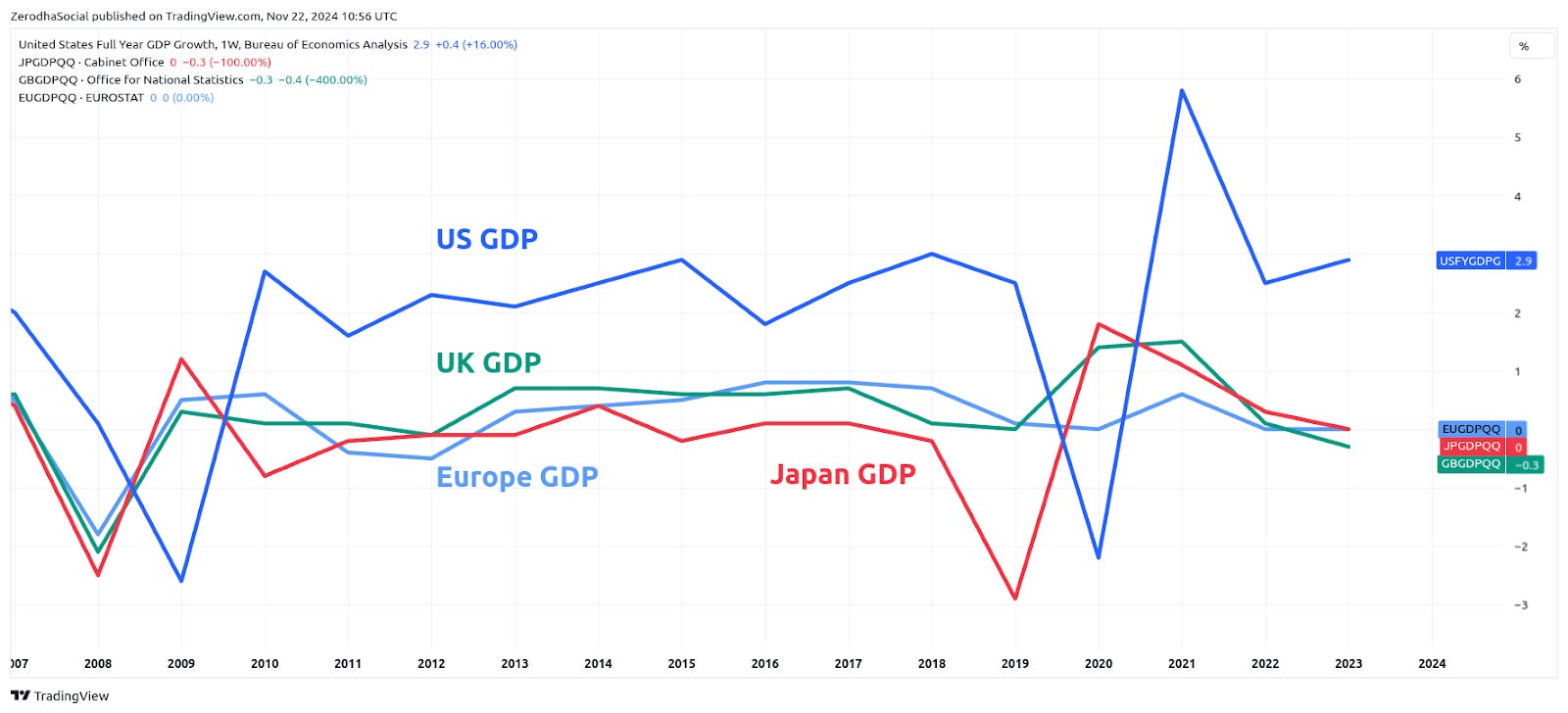

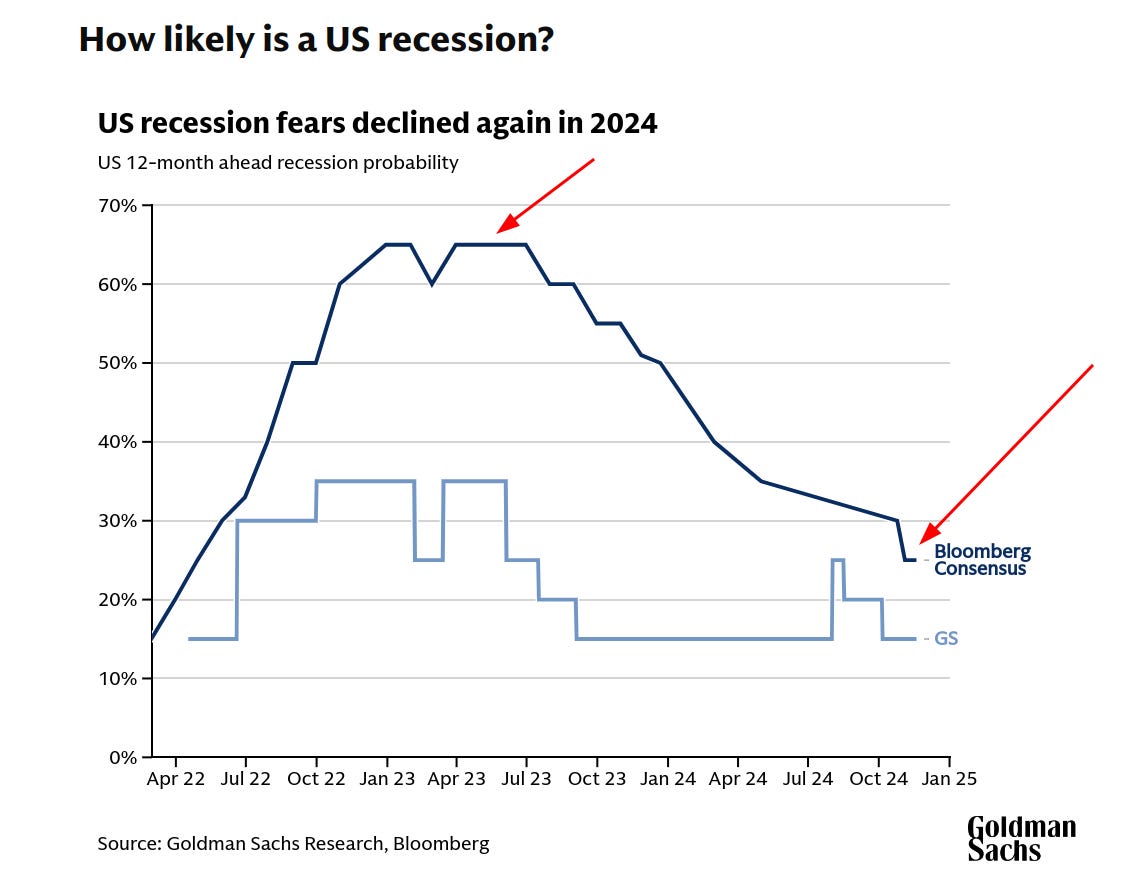

Now, let’s talk about the world’s biggest economies. The U.S. continues to lead the pack, and for the third year in a row, it’s growing faster than other developed countries. According to the IMF, the American economy is expected to grow by 2.8% this year and 2.2% in 2025.

This is pretty remarkable, especially when you think about how, back in mid-2023, most experts were sure the U.S. was on the brink of a recession. Turns out, they couldn’t have been more wrong. The economy showed a level of resilience that surprised everyone.

Source: Goldman Sachs

The U.S. economy is performing exceptionally well. According to the latest growth estimates from the Atlanta Fed—one of the twelve regional Federal Reserve banks—the economy is still going strong and charging ahead.

Source: Atlanta Fed

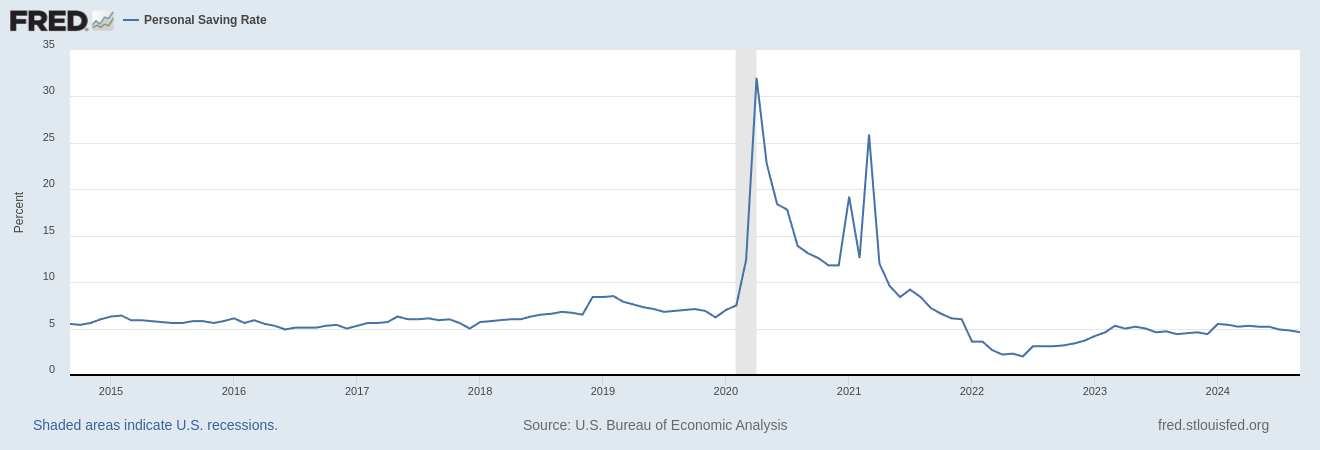

Consumption makes up about 70% of the U.S. GDP, and the U.S. is the largest consumer in the world, driving demand for many economies. Countries like Mexico, China, Canada, and others are closely tied to how the U.S. economy performs. So, if U.S. consumers start to struggle, it’s bad news for the rest of the world.

But right now, U.S. consumers are doing incredibly well. Personal savings have come down from the COVID-era highs but are holding steady. That means consumers aren’t feeling overly stretched just yet.

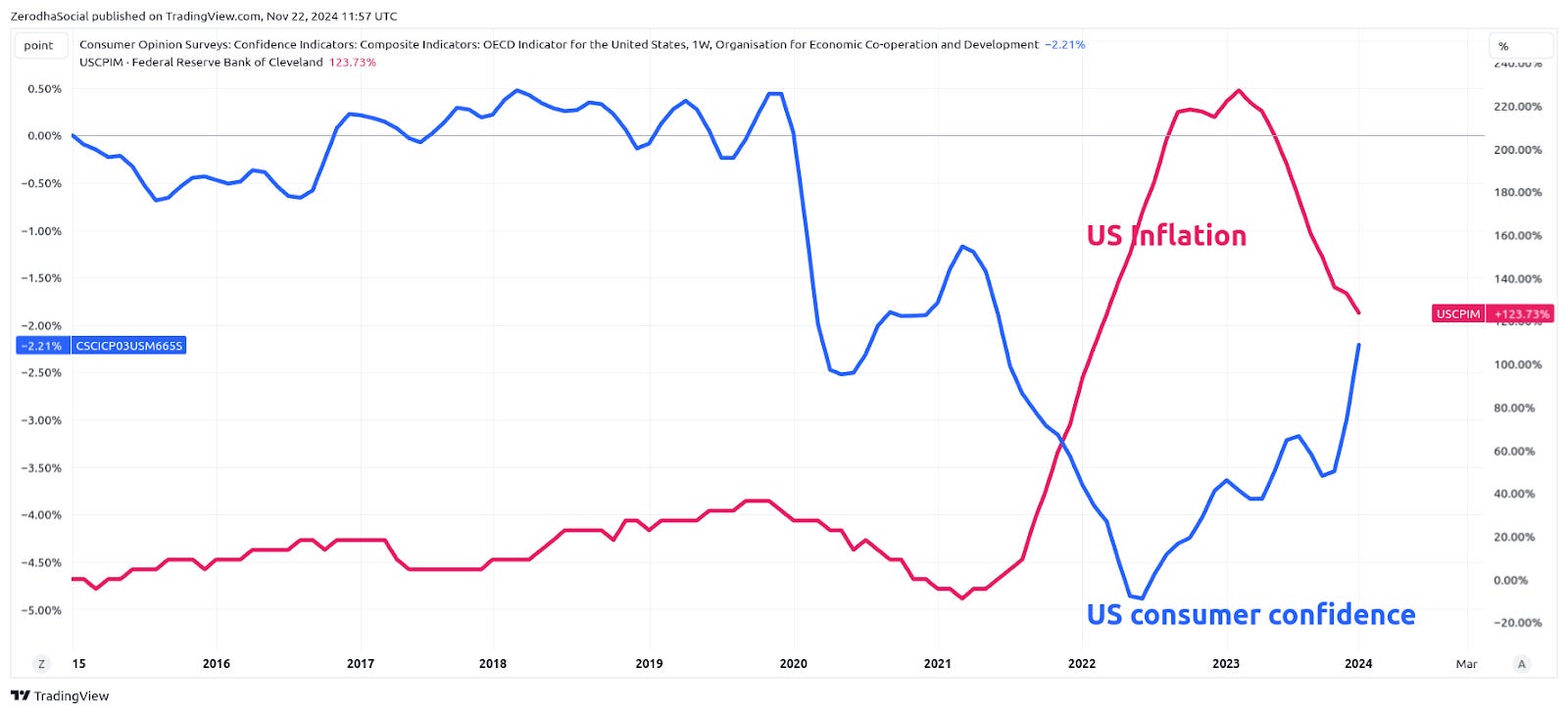

You can see this reflected in consumer confidence surveys too. Confidence hit rock bottom when U.S. inflation peaked in mid-2022. But as inflation has eased since then, consumer confidence has steadily bounced back.

Source: St. Louis Fed

Personal spending has also stayed strong, even in the face of high inflation and rising borrowing costs.

Source: St. Louis Fed

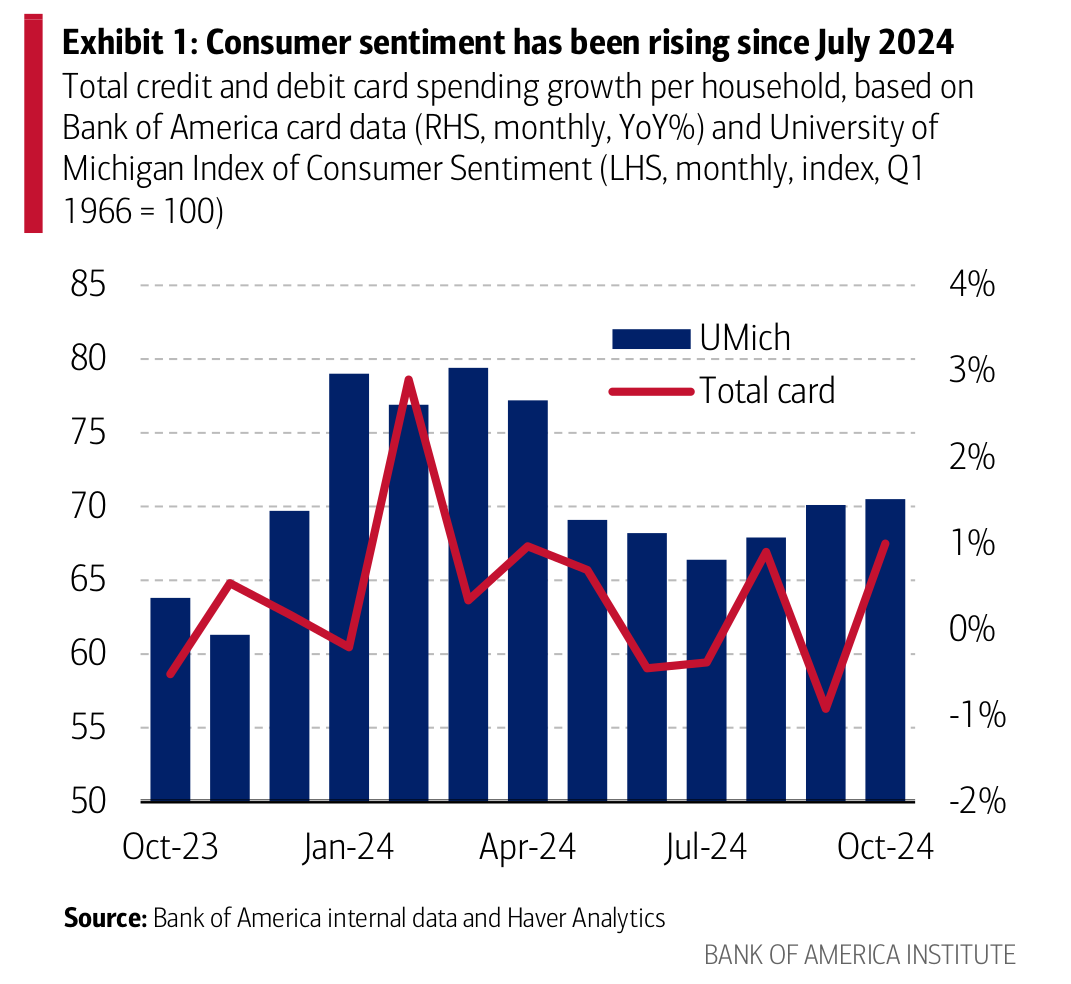

Here’s another data point from the Bank of America that measures credit card and debit card spending growth among its customers. It’s been remarkably strong.

The labor market is holding up remarkably well, despite all the noise in the headlines. When more people are working and finding jobs, it’s a clear sign of a healthy economy—and that’s exactly what’s happening right now. The strength of the job market shows that the U.S. economy is performing better than many had predicted.

The US is doing well on the inflation front as well. This has prompted the US Federal Reserve to cut interest rates from 5.5% to 5%. While inflation is still running a bit above the Fed’s ideal target of 2%, it’s dropped enough that they’re comfortable lowering interest rates. They basically think keeping rates high at this point would do more harm than good.

But Fed Chairman Jerome Powell is playing it safe. He recently said:

“The economy is not sending any signals that we need to be in a hurry to lower rates. The strength we are currently seeing in the economy gives us the ability to approach our decisions carefully.”

You might wonder why the Fed is cutting rates when inflation is still above their target. The answer is pretty straightforward: they’re planning ahead. Changes in interest rates don’t affect the economy overnight. Think of it like steering a large ship—you have to turn the wheel well before you want to change direction.

When the Fed changes rates, there’s a delay before we feel the effects. Banks need time to adjust their own rates for loans and savings accounts, and it takes even longer for these changes to ripple through to businesses and consumers. So the Fed has to think several moves ahead, rather than just reacting to today’s conditions.

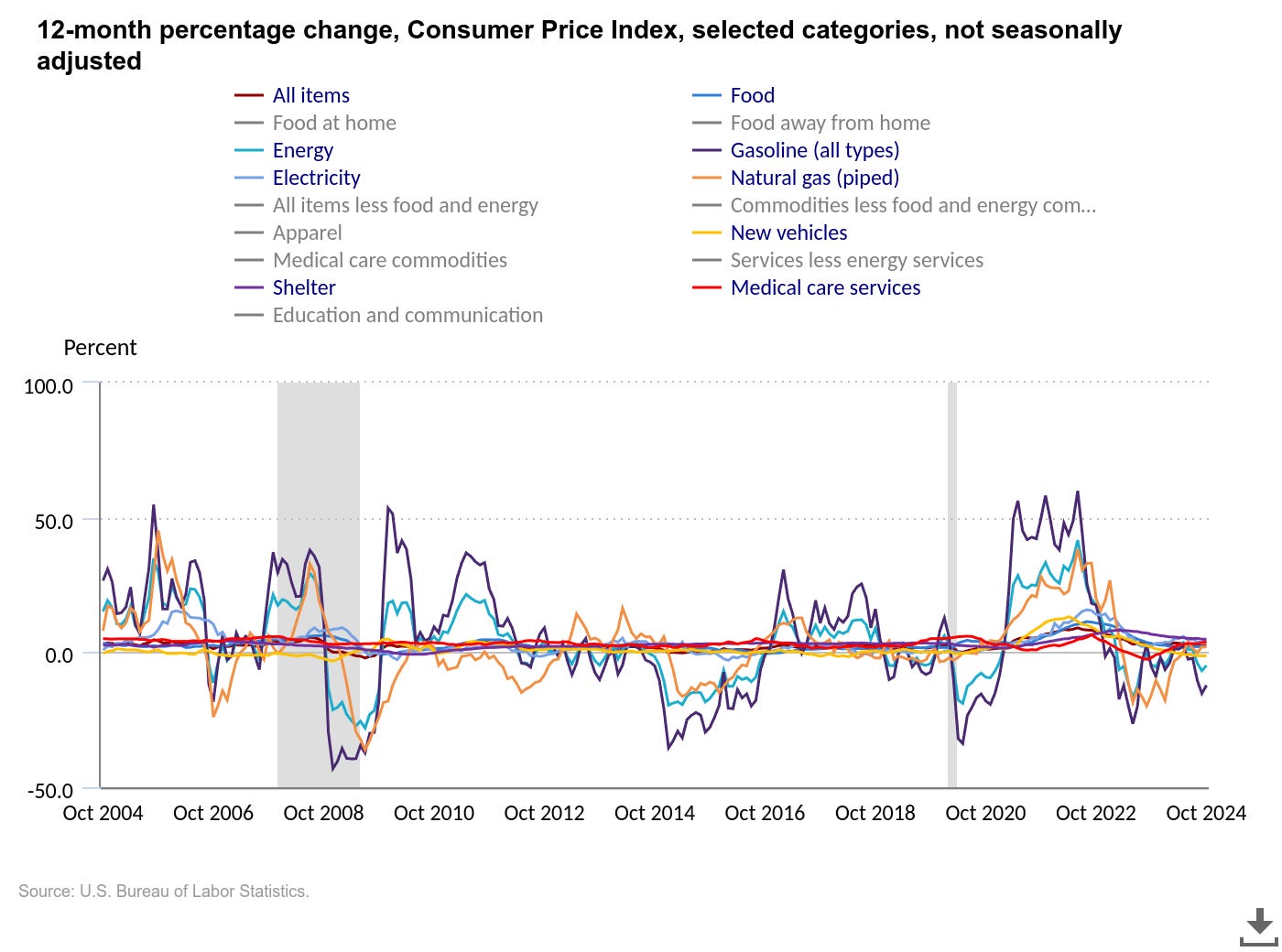

Source: BLS

In the U.S., inflation in areas like gasoline, car prices (both new and used), and food has slowed down significantly. But not everything is easing up. Some everyday expenses are still putting pressure on Americans’ wallets. Transportation costs remain high, housing prices keep climbing, and electricity bills are rising faster than anyone would like.

So, while the overall inflation situation has improved from its peak, it’s still a mixed bag when you dig a little deeper.

Source: Charlie Bilello

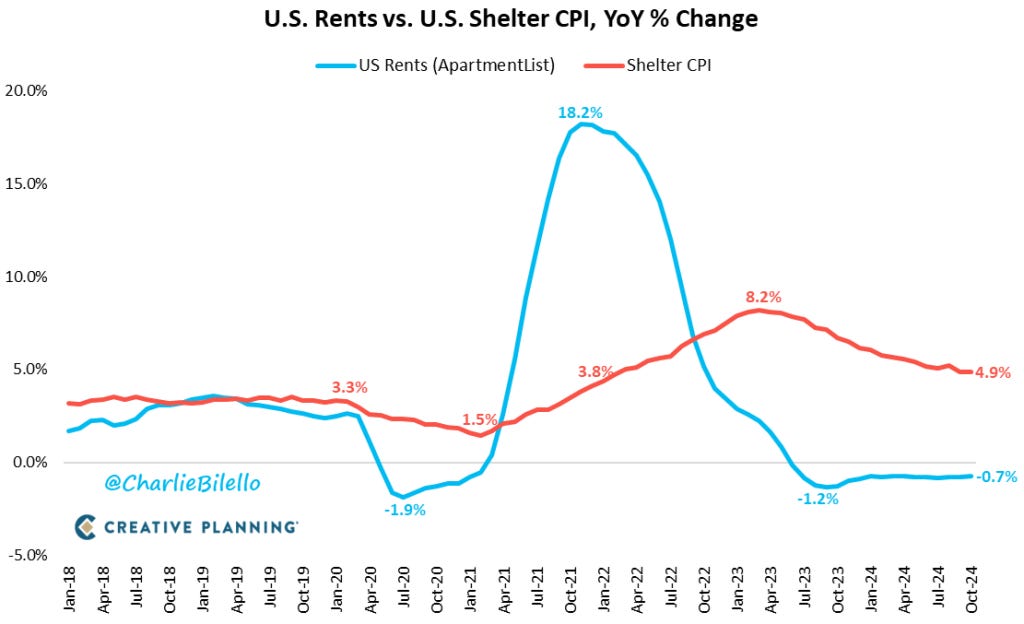

Shelter inflation is a key part of the U.S. Consumer Price Index, covering things like rent payments, hotel stays, and other housing-related costs.

Right now, inflation in this sector is still running high at 4.9%. That’s significant because housing tends to be the biggest expense in most people’s monthly budgets. When rents rise faster than wages, it leaves less room for other essentials. So, even if prices for things like gas or groceries are leveling off, high housing costs can still make it feel like your paycheck isn’t stretching as far as it used to.

Source: Charlie Bilello

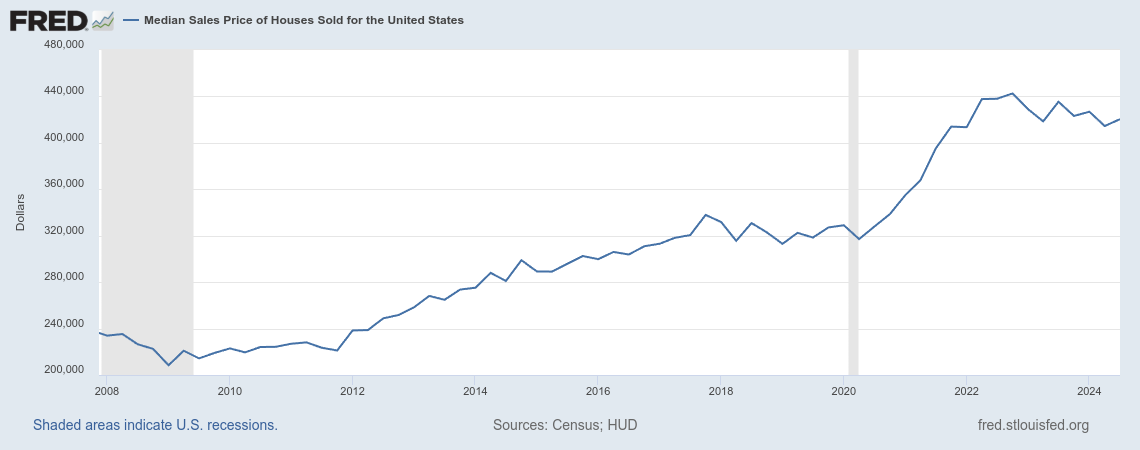

To put things in perspective, the U.S. housing market has gone through some major changes since 2020. When COVID hit, the Federal Reserve slashed interest rates to near zero, making mortgages much cheaper. At the same time, the rise of remote work drove up demand for homes.

On the other hand, housing supply was tight. Construction slowed during the pandemic, building materials became more expensive, and investors were snapping up properties. These factors combined to drive housing prices sharply higher.

While prices aren’t climbing as quickly now, they’re still much higher than pre-pandemic levels. This has created a serious affordability issue, leaving many Americans struggling to buy homes.

Source: St. Louis Fed

Overall the US economy is doing quite well and as long as the US economy does well, the global economy will continue to be steady.

Trump’s tariffs

In the post-COVID world, geopolitics has taken center stage as the biggest risk to financial markets. From the Russia-Ukraine war to conflicts in the Middle East and rising tensions between China and the U.S., it’s been a turbulent time. And alongside these events, buzzwords like de-globalization, de-dollarization, slowbalization, and fragmentation have been making the rounds.

These issues are becoming even more critical as Donald Trump prepares to take office as the president of the United States. The big question on everyone’s mind is whether he’ll impose tariffs—not just on Chinese imports, but potentially on goods from the rest of the world too.

With that in mind, let’s explore how global trade has evolved over the years and what impact such tariffs could have on the global economy.

Since 2012, global trade as a percentage of GDP hasn’t really declined—it’s more or less plateaued.

Source: UNCATD

Source: IMF

Both the IMF and the World Trade Organization have noted signs of fragmentation in global trade. One key trend is that countries are increasingly trading with nations they consider friendly, rather than with others they might have less favorable relations with.

Source: WTO

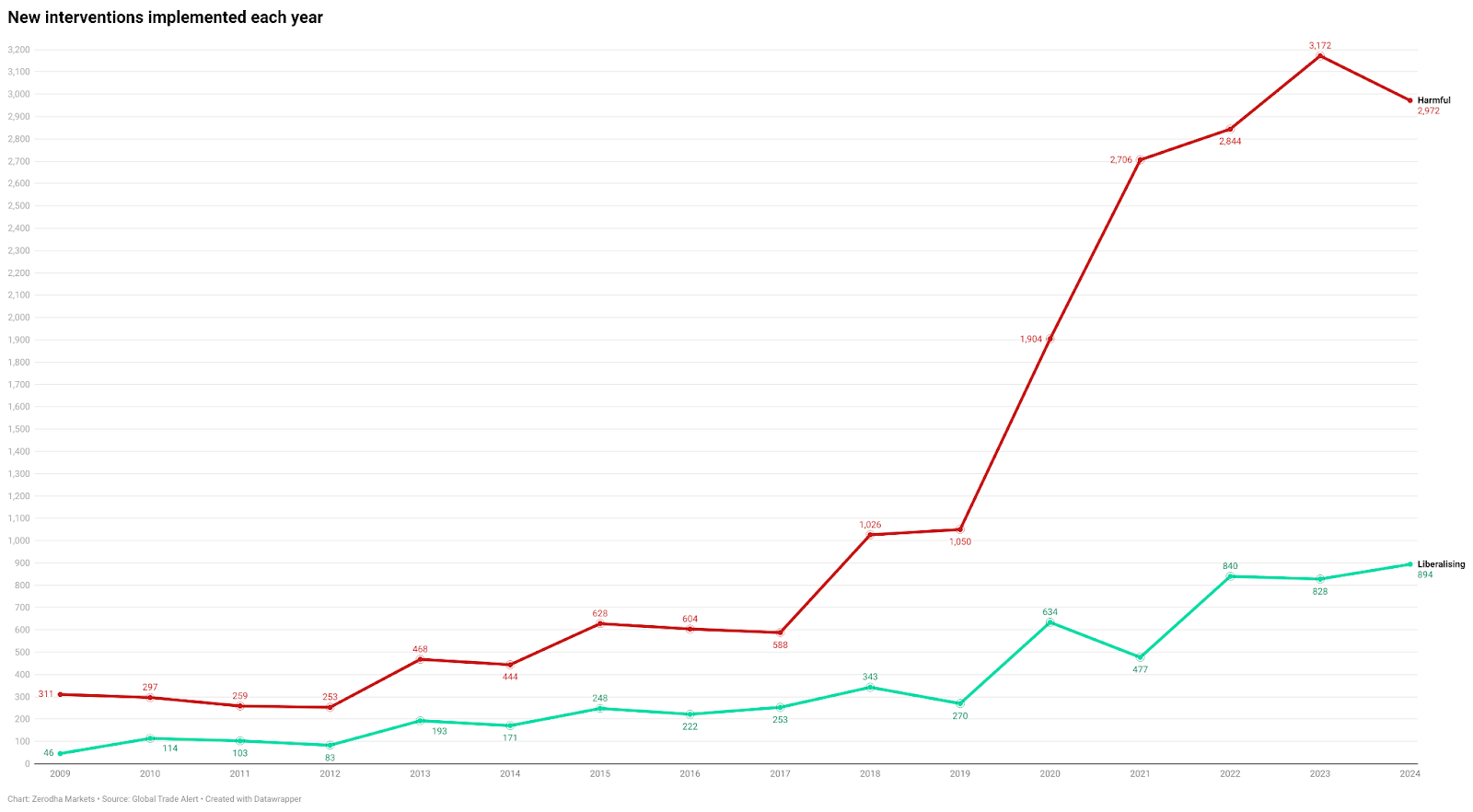

Another sign that things are heading in the wrong direction is the growing number of trade restrictions imposed by countries. Since Russia’s invasion of Ukraine, there’s been a noticeable spike in these restrictions. Nations are increasingly putting up barriers to control what goods can cross their borders.

It is in this context that Trump will take office as the president of the United States. So what will be the impact of Trump tariffs on the world? Who will be the winners and losers?

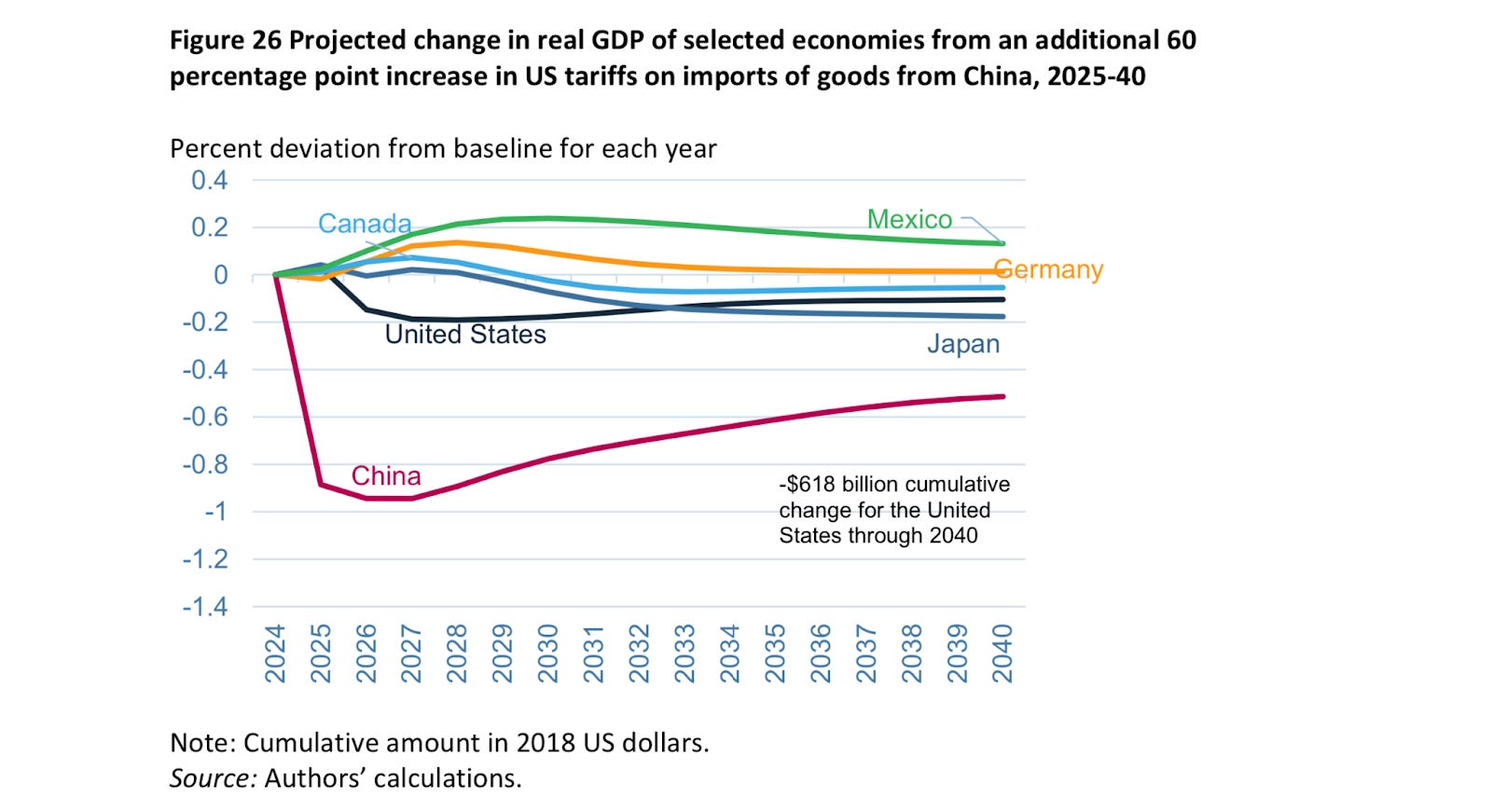

The Trump administration is talking about increasing tariffs on Chinese imports—potentially up to 60% on some goods—and may also add a blanket 10% tariff on everything imported from other countries. These measures aim to pressure foreign suppliers but may not significantly destabilize the U.S. economy due to prior adjustments in trade patterns.

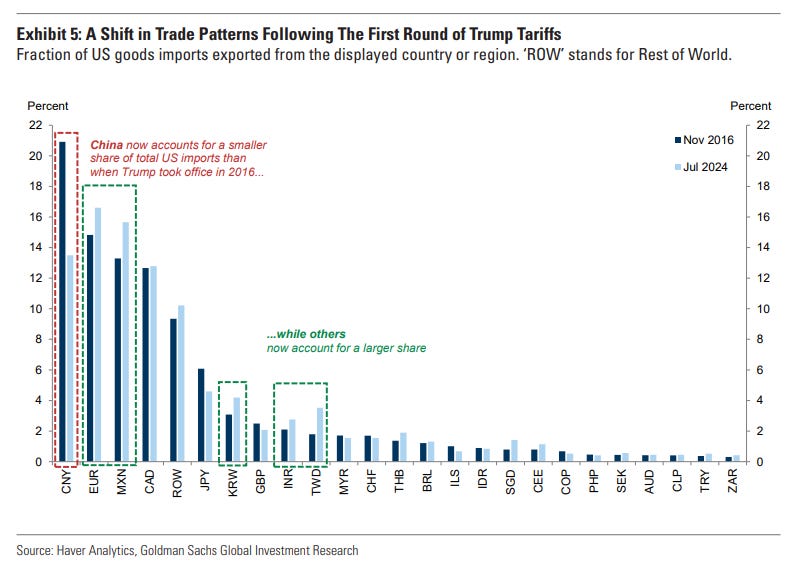

Since the first round of tariffs back in 2018-2019, the U.S. has learned to rely less on China. Many businesses have started buying from other countries, like Mexico and Canada, instead of China. In fact, China’s share of U.S. imports dropped from 21% in 2016 to less than 15% in 2024.

Source: Goldman Sachs

This reduction has helped businesses diversify their supply chains and spread risks, but it doesn’t entirely eliminate dependence on China for key sectors like electronics and pharmaceuticals.

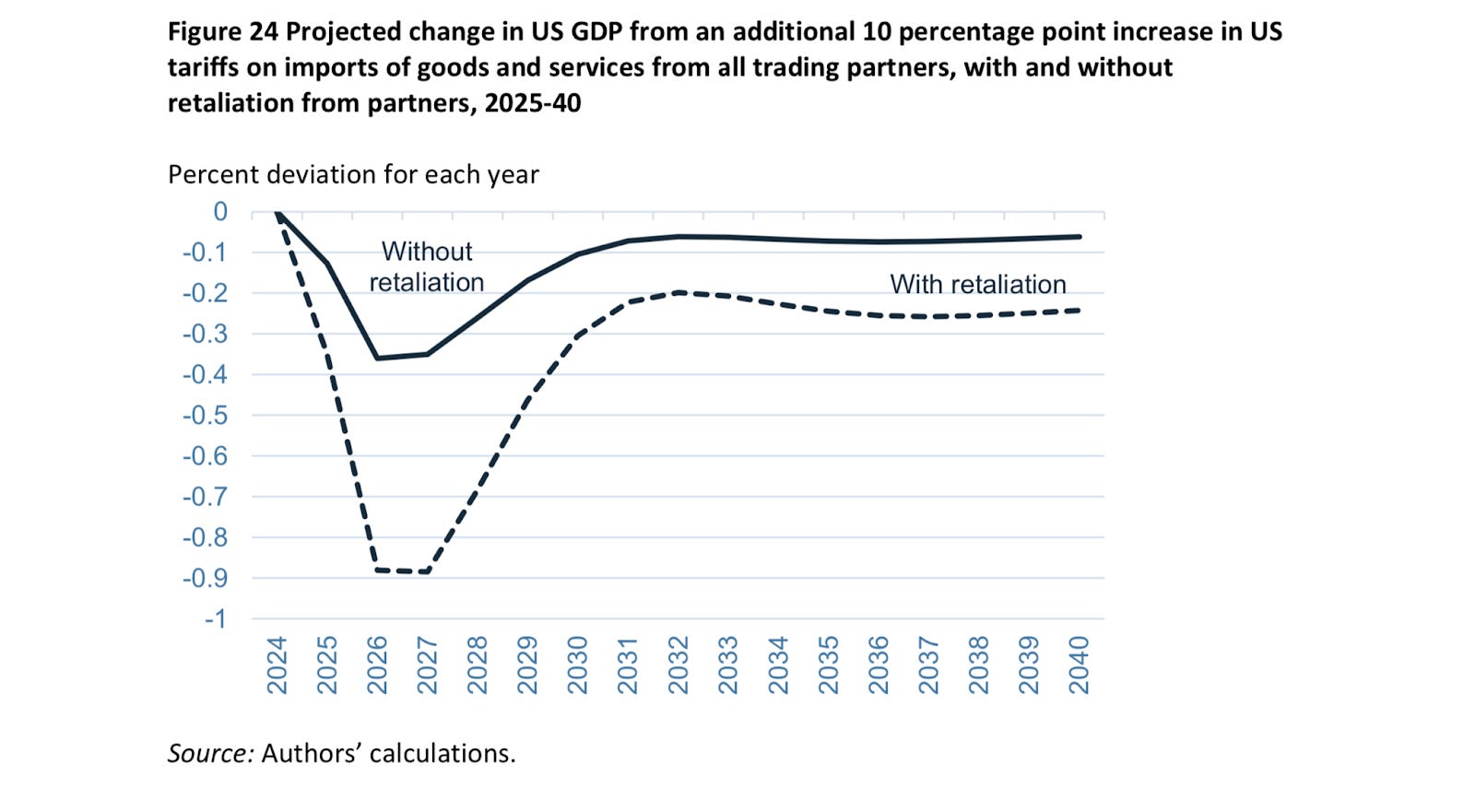

However, if tariffs are applied to all imported goods, regardless of where they come from, the economic impacts will be much broader. A 10% across-the-board tariff would weigh heavily on U.S. GDP, leading to a 0.36% decline by 2026 as per the PIIE working paper.

Source: PIIE

Other economies, such as Canada and especially Mexico, would face even greater challenges. Mexico, in particular, is highly reliant on trade with the U.S., with exports accounting for a significant portion of its GDP.

Source: PIIE

A 10% tariff is projected to have significant economic consequences. For Mexico, it could result in a $28 billion GDP decline in a non-retaliation scenario and as much as $53 billion if retaliatory tariffs are introduced.

While Canada would also feel the impact, it would be less severe compared to Mexico. This is because Canada’s economy is slightly more diversified and less dependent on U.S. exports in tariff-affected industries like manufacturing. That said, sectors such as automotive and agriculture would still experience disruptions.

The European Union would face moderate effects, with countries like Germany being hit the hardest. Germany, which relies heavily on exporting machinery and vehicles—much of it to the U.S.—would see reduced demand as a 10% tariff makes its products more expensive, potentially slowing growth.

China, despite being less reliant on U.S. trade, would still face substantial challenges. Key export industries like electronics and machinery would take the brunt of the impact. A slowdown in Chinese exports would ripple through global supply chains, affecting countries that rely on Chinese intermediate goods.

Source: PIIE

As tariffs increase, businesses across sectors would face higher input costs, while consumers might pay more for everyday items like electronics, groceries, and clothing.

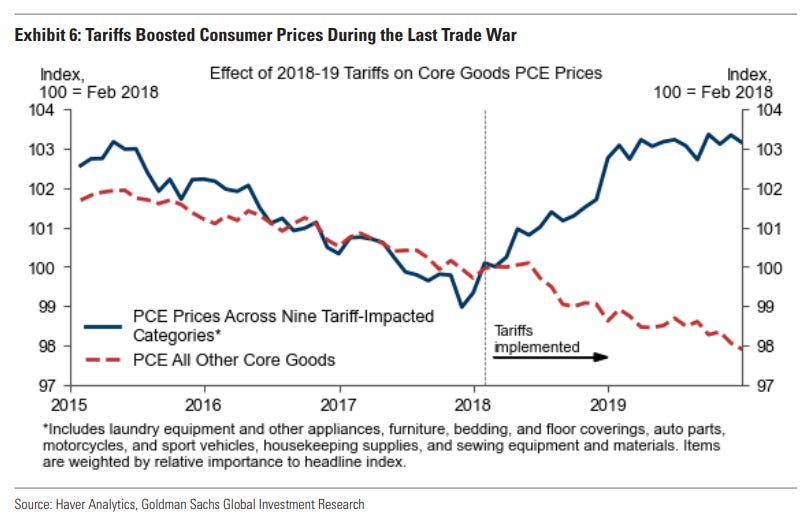

Tariff-driven price hikes were evident during the 2018-19 trade war when prices of core goods in tariff-affected categories rose sharply.

Source: Goldman Sachs

A similar inflationary pressure could resurface, Higher tariffs are expected to raise U.S. core inflation by 1.2% under a 10% universal tariff, according to Peterson Institute data. This would strain household budgets and undo recent progress on inflation control.

Source: PIIE

There’s another concern—other countries might retaliate with their own tariffs, creating a domino effect on the global economy.

Retaliatory tariffs from trading partners could amplify the economic damage. Sectors like agriculture, durable manufacturing, and mining—industries that rely heavily on exports—would bear the brunt of these actions, even though they’re often the ones tariffs aim to protect.

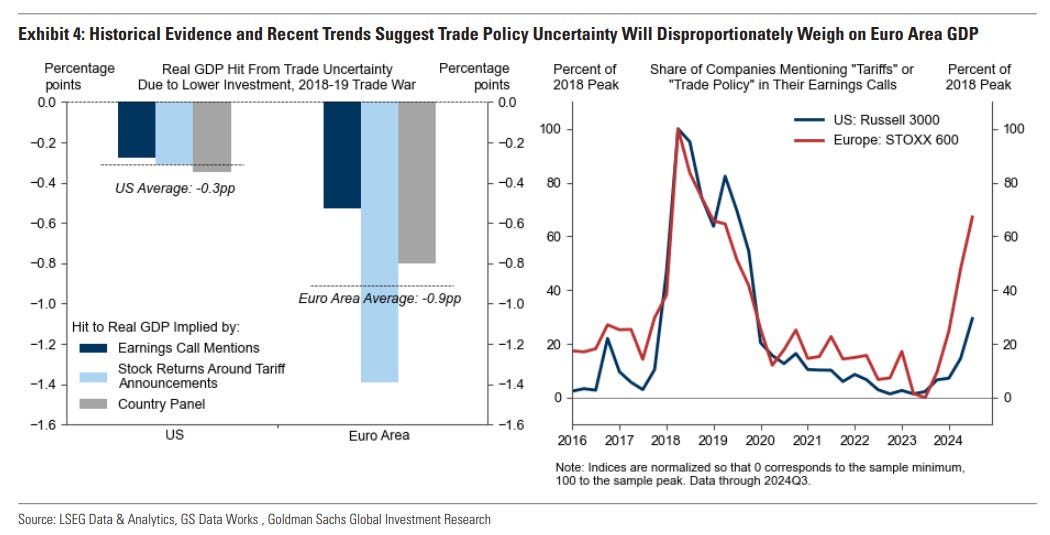

The fallout would also extend to regions like Europe, which are deeply dependent on trade. According to a Goldman Sachs report, the eurozone could face a GDP contraction of nearly 0.9%, compared to a smaller 0.3% hit for the U.S.

Source: Goldman Sachs

Even with reduced trade ties, the U.S. is still one of China’s largest customers. New tariffs could significantly impact Chinese industries, particularly electronics, machinery, and textiles. According to the PIIE report, a 60% tariff on Chinese imports could reduce China’s GDP by 0.9% by 2026.

While Beijing might roll out stimulus measures to offset the slowdown, the ripple effects on global supply chains could take years to fully stabilize.

Source: PIIE

While targeted tariffs on Chinese goods have had a smaller economic impact, broad-based tariffs could have far-reaching consequences. They could drive up inflation, trigger retaliatory measures, and create global ripple effects, making the next round of tariffs more harmful than earlier ones.

Although the U.S. economy has adapted to reduced Chinese imports, a universal tariff policy could undo some of that progress, leading to higher costs for businesses and households alike.

Rise of thematic

Now let’s take a look at the rise of sectoral and thematic funds in India.

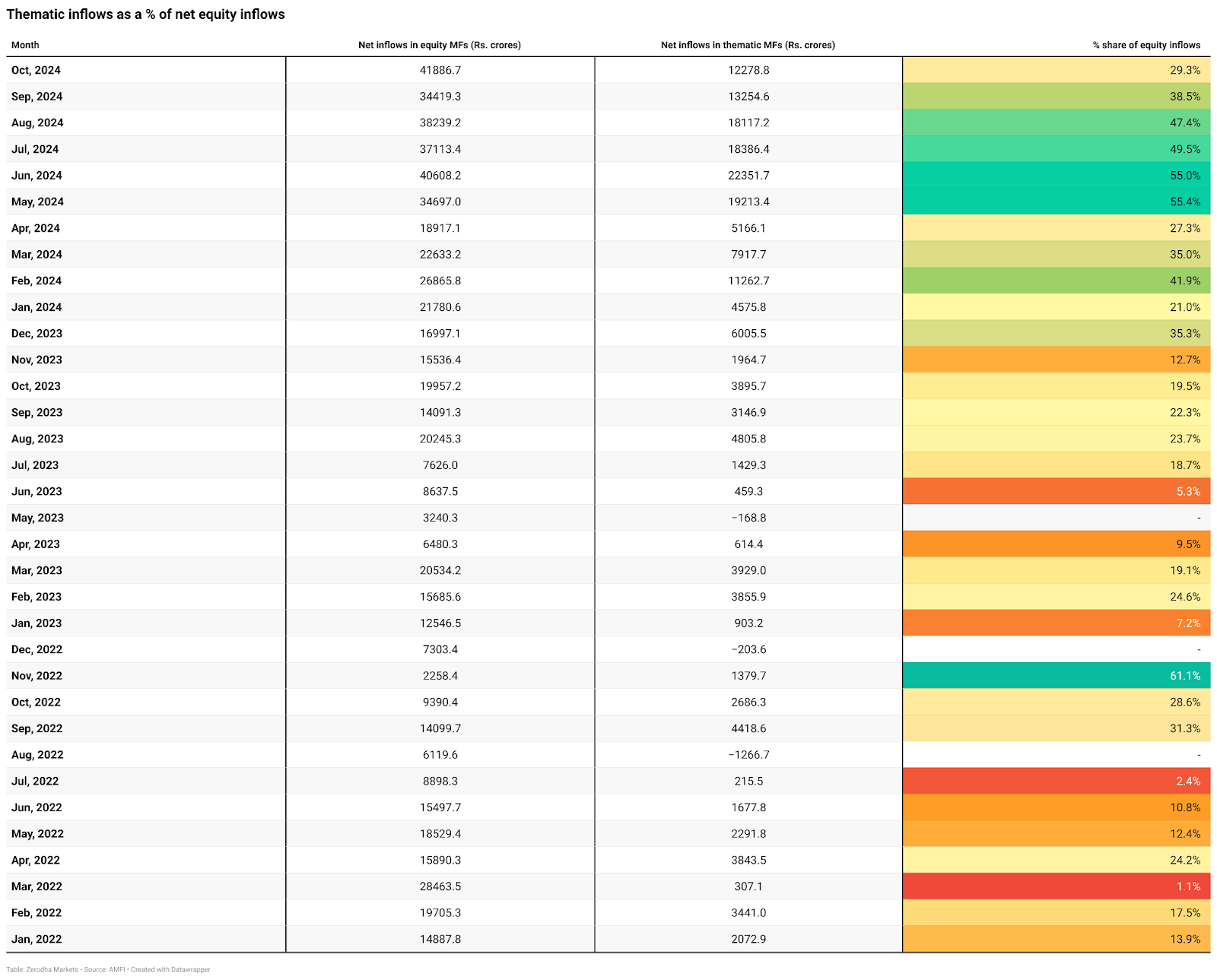

Whenever something starts doing well, everyone wants a piece of the action. Nobody wants to miss out trend that is making money. And this is what we are seeing with sectoral and thematic funds this year.

These funds, which focus on specific sectors or themes, have attracted 42% of all money flowing into equity mutual funds—amounting to ₹1.32 lakh crores by October. To put that in perspective, this is more than the total inflows we saw during both 2022 and 2023 combined.

If you’re not familiar with how sectoral or thematic funds work, think of them as a basket of stocks tied to a single idea. Unlike regular mutual funds that spread your money across various sectors, these funds zero in on a particular sector or a theme like electric vehicles.

Sectoral funds focus on a single industry, like banking or pharma. While thematic funds invest across sectors but are unified by a central trend, such as EV funds investing in automotive, battery manufacturers, and related industries.

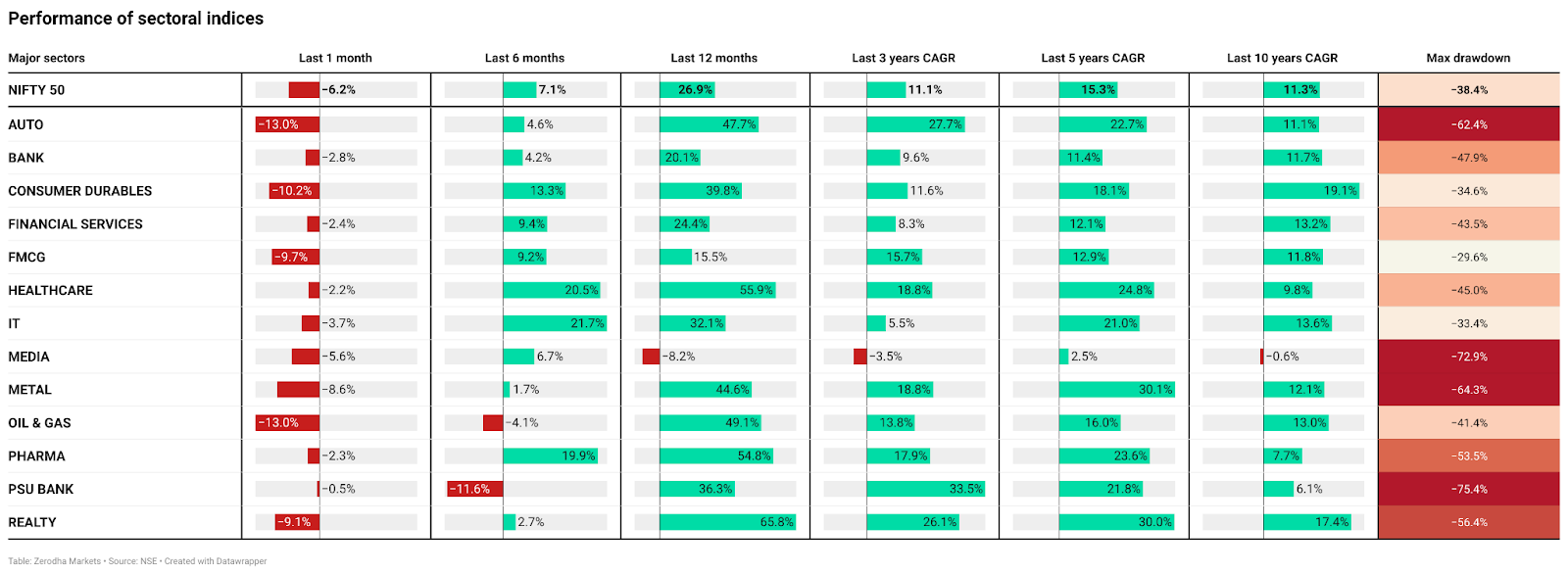

Given how popular these funds have become, we decided to look and see how different sectors have actually performed over time. Let’s start with the major sector indices.

If we go by the data up to the end of October 2024, most major sector indices have had a fantastic year, with 8 out of 13 doing better than the Nifty 50 index in the past 12 months. But here’s the thing: when you look at the long-term performance—say over five or ten years—most sectors end up giving returns that are pretty similar to the Nifty.

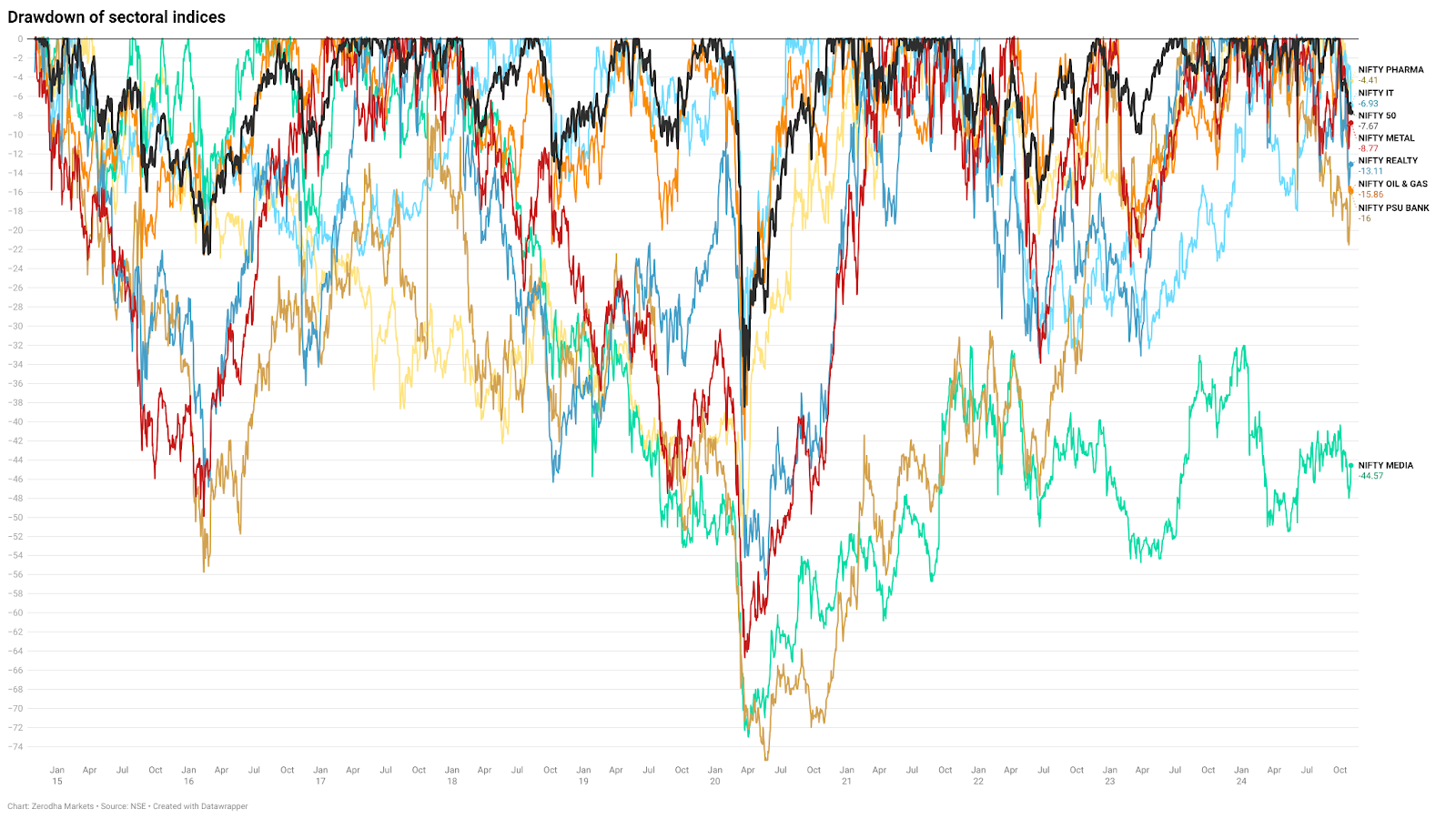

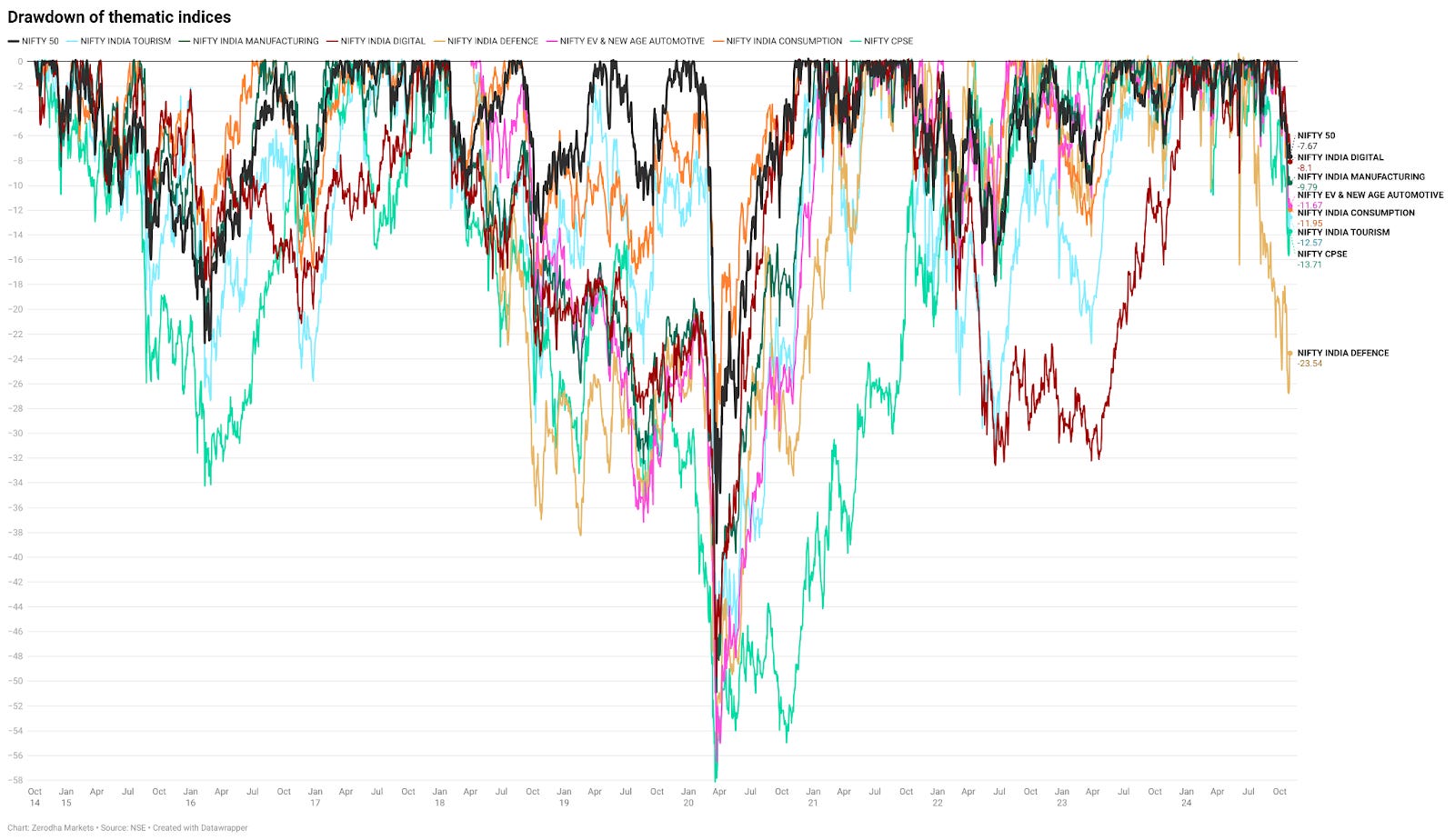

Coming to thematic indices, which have become quite popular this year. And you can see from the charts why that is the case. Over the last 6 and 12-month period, most if not all these themes have given spectacular returns. However, as you extend your time horizon, the returns aren’t all that impressive and are just keeping pace with the broader market.

Why does this happen? It’s because sectors and themes tend to perform in cycles. They’ll have their moment where they outshine everything else, but once that cycle ends, they usually go through long stretches of underperformance. And these downturns can be brutal.

Some sectors and themes have seen their value drop by over 75% during bad phases. Timing the market to ride these cycles perfectly is almost impossible. Most of us aren’t going to buy at the bottom and sell at the peak—we’re just not wired that way. More often than not, people end up buying high when the hype is strong and selling low when things start to turn.

Part of why people are attracted to these funds is psychology. When something is doing well, it’s hard not to feel like you’re missing out. This “fear of missing out,” or FOMO, makes us chase trends without thinking about the risks.

There’s also something called recency bias, where we assume that just because a fund has been doing well recently, it’s going to keep performing the same way. But if you dig into the history, you’ll see that’s rarely the case.

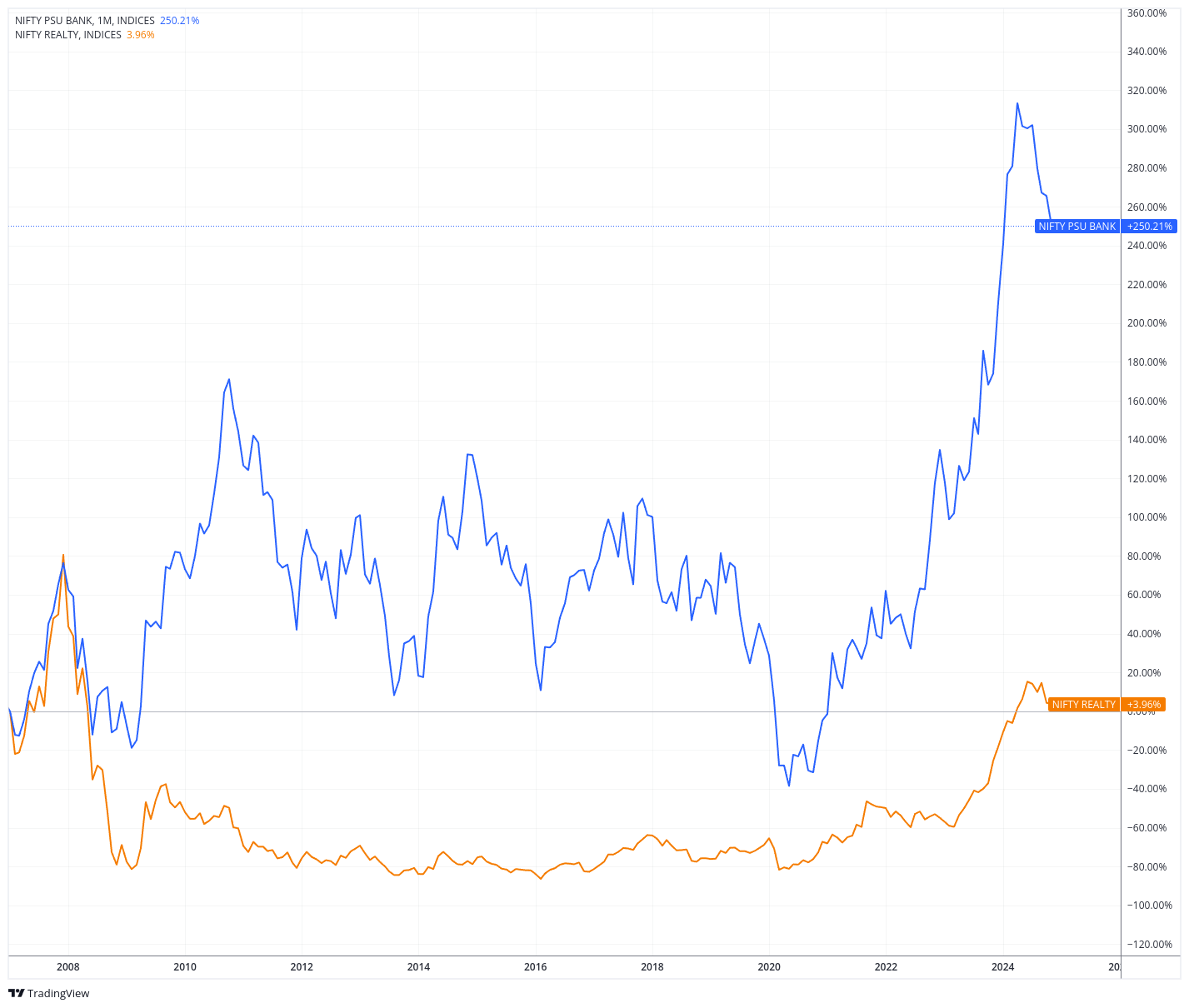

Let’s take real-life examples. Back in 2007, the realty sector was on fire. Everyone wanted in, and then the global financial crisis hit. Realty stocks crashed, losing 90% of their value from their peak. Even now, 17 years later, the sector hasn’t recovered to those levels.

The PSU bank sector is another one—it has performed very well in the last 3-4 years, but historically the performance has always been highly cyclical, with sharp declines during tough economic times.

The reason for this cyclicality is how closely these funds are tied to larger economic and policy trends. For example, government programs like “Make in India” or the push for electric vehicles have driven interest in manufacturing and EV themes.

These ideas are exciting, but they’re also dependent on factors like government subsidies, infrastructure, and global demand. If those things slow down, so do the returns.

Does this mean you should avoid these funds altogether? Not necessarily. If you truly believe in a theme and have the patience to ride out the ups and downs, they can be a good addition to your portfolio. But they shouldn’t be the sole focus of your investments. And you also need to be ready for some serious volatility. If you’re someone who gets nervous when the market drops, these funds might not be for you.

Trends come and go, and while it’s tempting to jump on a bandwagon, long-term investing is a marathon, not a sprint.

That’s it from us today. Do share this with your friends to spread the word.