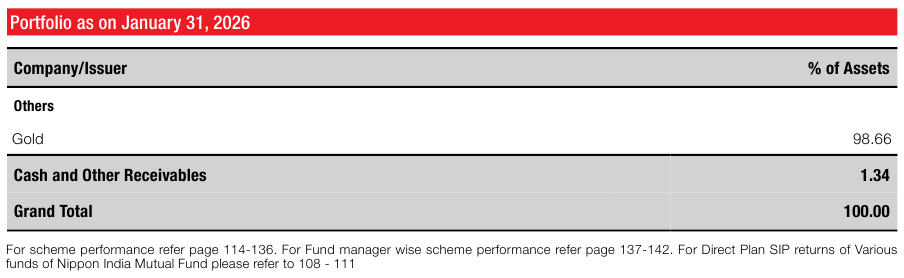

Earlier, Gold ETFs were almost entirely backed by physical gold. Now, SEBI allows fund managers to invest a portion of the portfolio in gold derivatives such as futures, while still maintaining at least 95% exposure to gold and gold-related instruments. It is evolving into a hybrid instrument .

refer : https://www.business-standard.com/finance/personal-finance/are-gold-etfs-moving-away-from-physical-gold-what-investors-should-know-126040600163_1.html

This means Gold ETFs are no longer strictly holding only physical gold. A small portion of the exposure can now come from financial contracts that track gold prices rather than actual gold stored in vaults.

Another important change is in valuation. Previously, Gold ETFs were largely benchmarked to international gold prices with adjustments. Now, valuation is more aligned with domestic spot prices in India, which improves price accuracy for local investors.

Because of these changes, Gold ETFs are moving from being a pure physical gold proxy to a slightly more flexible structure. This introduces some new elements such as derivative exposure, which can involve roll-over costs and minor tracking differences. However, the overall gold exposure requirement ensures that the fundamental nature of the ETF remains intact.

From an investor perspective, this does not significantly change the role of Gold ETFs as a tool for price exposure to gold. They still remain suitable for liquidity, allocation, and portfolio diversification.

However, investors who specifically want pure physical gold exposure should be aware that ETFs may no longer fully serve that purpose in the strictest sense.

When huge investment happens in gold etf , physical gold may get more demand so waiting for physical gold may lead to tracking error . This time the future will be helpful to invest money rather than waiting for the physical gold .

The key takeaway is that Gold ETFs remain a price-tracking instrument for gold, but they are no longer a perfect representation of holding physical gold. Investors should start paying attention not just to returns, but also to how individual funds are managing their gold exposure.

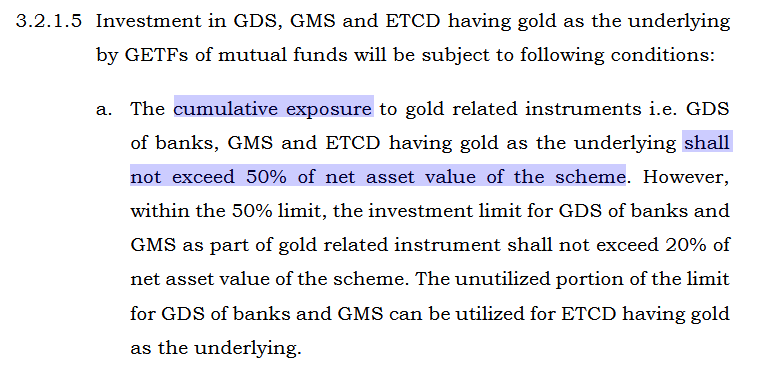

This thread also say limit 50 perc ETCDs

ref : Ask me anything about Zerodha Fund House - #477 by VishalJain