Few general thoughts on this topic -

Physical gold without intermediaries is 100% exposure to gold,

comes with a “running cost” (cost of verifying it, physically securing it, insuring it, …).

Depending on the individual’s situation and amounts involved,

for some, this still might still be the most financially optimum option.

This article goes into the details of the various costs involved.

Also checkout this recent topic-thread on bank lockers

New Bank Locker Rules - Banks liable upto 100 times the annual rent

Financial instruments, with intermediaries involved

can provide returns correlated to physical gold minus expenses.

Any of those whose operational expenses are lesser

than an individual’s expenses securing physical gold,

seem attractive alternatives to physical gold.

However, by definition, the behavior of each of these derivatives will fail to match the behavior of Gold under respective corner-cases. And the risks associated with each intermediary (however well regulated, and minuscule the risks maybe) are what one needs to consider.

If one is seeking exposure to Gold as a hedge against global economies going haywire, then those are precisely the scenarios when such financial instruments are likely to fail. No free lunch here.

Alternately, if one seeks exposure to gold with certain assumption (trust in a specific intermediary - sovereign/framework/institution) or is willing to ignore/discount certain risks, or already has an alternate hedge against such scenarios, can then opt for exposure to Gold through that route.

In addition to SGBs,

domestic and international ETFs and ETCDs,

and R-GDS/STBD # under GMS (example)

are a few options that immediately come to mind.

# - Purchasing physical gold and depositing it in a R-GDS/STBD scheme to minimize the “running costs” associated with securing physical gold.

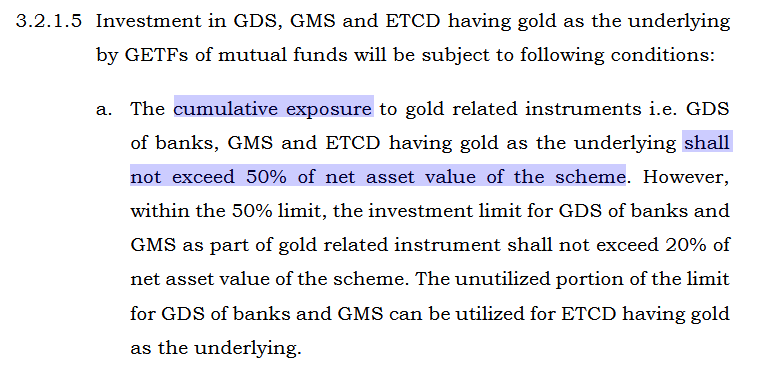

Close but not exactly.

Of the NAV,

i. Upto 20% allowed in GDS/GMS

ii. Upto 50% allowed in “gold related instrument” (inclusive of i above)

iii. >95% required to be Gold + Gold-related instruments.

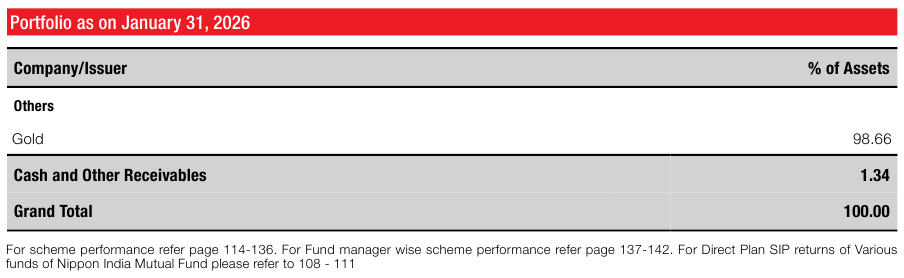

For example, recently in Jan 2026,

apparently Nippon India’s GoldBeES had ~1.34% in cash/cash-equivalent for operational reasons.

Source: Section 3.2 Gold Exchange Traded Fund Scheme of Master Circular for Mutual Funds (from 27 Jun 2024).

If you have read so far,

you may also enjoy reading this recent post on The opaque curtains of India’s gold pricing to explore some of the not-so-obvious risks associated with gold as an investment class.