2022 has been one of those rare years where there was no place to hide for nearly all the asset classes. Although Gold was no exception to it, it fared far better compared to the rest.

To put things in perspective, despite all the volatility, Gold gave double digit returns to Indian Investors.

Gold in 2022 - in INR terms

Gold in 2022 - Dollar terms

State street advisors shared an interesting article on Gold’s outlook for 2023 and here are some of the highlights:

2022- An Overview

Gold’s performance throughout 2022 could be summarized simply as “surprising.” For some investors, gold was surprising as it did not live up to performance expectations despite several supportive catalysts for the price, including rising equity market volatility as indices broadly entered a bear market; the Russian invasion of Ukraine raising the specter of long-lasting geopolitical turmoil in Europe, and multi-decade-high inflation weighing on the global growth outlook.

Conversely, other investors found gold surprising in its endurance to portfolios and how well gold held up in the face of the Federal Reserve (Fed) aggressively increasing interest rates, rising real yields, the US dollar hit a 20-year high, and sporadic lockdowns in China impacting gold demand.

4 Themes to watch out for in 2023

- a potential pause or even pivot in the Fed’s monetary policy against growing recession risks

- waning US dollar strength as other global currencies experience mean reversion

- total global demand for gold maintaining current levels

- greater economic uncertainty and ongoing geopolitical turmoil driving market volatility and demand for downside protection among investors

Balancing Act by Monetary Policymakers May Raise Risk of Global Recession

What transpired so far

-

The Fed’s hawkish turn to combat rising price inflation in 2022 came at an unprecedentedly aggressive pace increasing the policy benchmark by 375 basis points (bps) over the course of six months, applying four consecutive 75bps hikes, and bringing its policy rate to the highest level since 2008 causing double-digit fall in equity indices and the US 10-Year Treasury yield more than doubled to 3.61% in 2022.

-

The Fed may have broadly achieved its target goal of “squashing” inflation, given the decline in market expectations for US inflation and correction in financial assets. As a result, it seems more likely that the Fed may slow its pace or pause its hiking cycle in the first half of 2023. The gold price declined in response to these shifting interest rate levels, while also closely tracking the decline in inflation expectations.

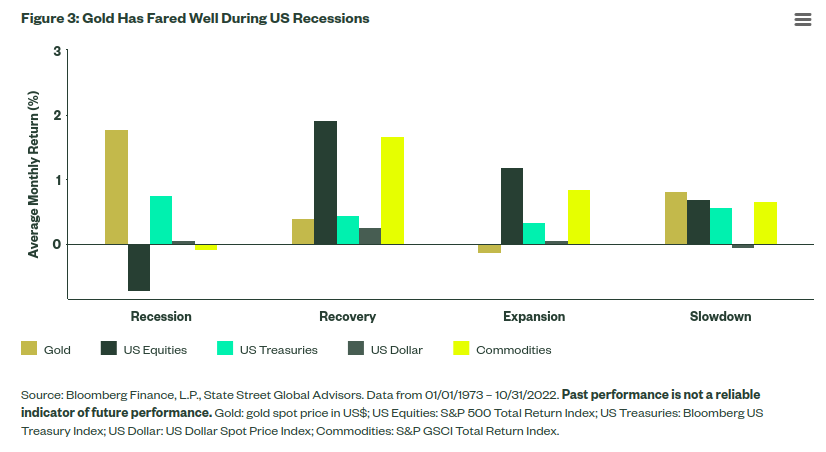

Gold is a go-to place for investors during recessions

-

Gold’s behavior during previous recessionary periods in the US is clearly in favor of yellow metal.

-

On an average monthly basis, Gold has done best during periods of recession and slowdown, during which it has outperformed US equities, US Treasurys, commodities, and the US dollar.

-

Even during periods of US economic recovery, gold has shown positive returns while keeping pace with other defensive portfolio assets such as Treasurys and the US dollar.

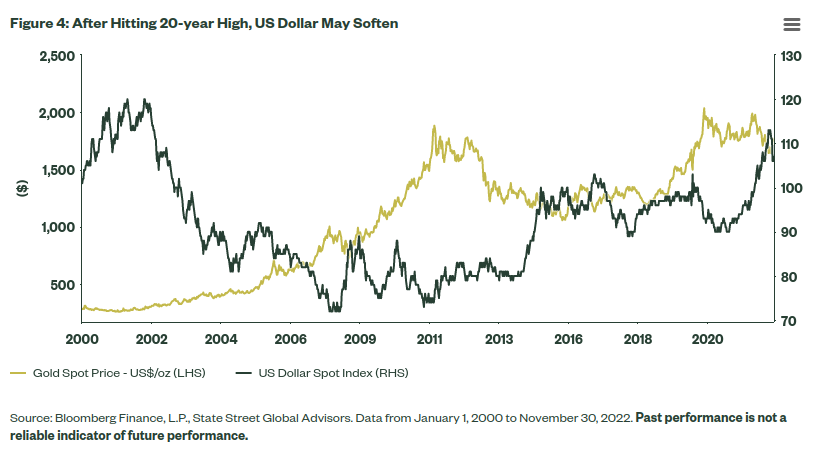

The US Dollar index is peaking as a result of rates plateauing

- Given the historical negative correlation between gold and the US dollar, gold came under pressure in the strong dollar environment that emerged this year. But expectations for a monetary policy pivot or pause in 2023, along with mean reversion in other global economies, may put pressure on the US dollar. This may lead to renewed interest in gold among US investors seeking to hedge against a more temperate US dollar environment.

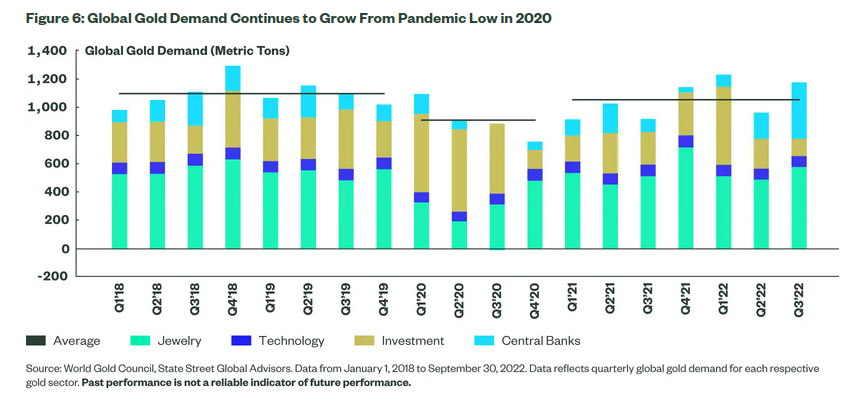

Total global demand for gold maintaining current levels

Global demand for gold in 2022 was strong among key sectors including investments, jewelry, and central banks

Overall demand is headed back to pre-pandemic levels

Barring the pandemic that had a material impact on gold demand, with a quarterly average of 913 metric tons in 2020 compared to the 2018-2019 quarterly average of approximately 1,102 metric tons. Since the drop in 2020, however, the average quarterly demand from 2021-2022 was 1058 metric tons — returning closer to its’ pre-pandemic pace and in line with longer-term trend levels. This is a healthy sign that the fundamental drivers for gold are on strong footing heading into 2023.

-

Headwinds like ongoing targeted COVID lockdowns in China may impact demand in that region, but strong investment demand in Europe and global central bank buying in 2022 are key trends that may persist into next year.

-

Central bank net buying in particular was a source of significant demand, with an estimated quarterly record of 400 tons of gold added to central bank holdings in Q3. This brought the year-to-date 2022 central bank gold demand on par with record levels for full-year demand in 2018 and 2019.

-

Investment activity in response to the current monetary policy and macroeconomic environment may continue to drive the gold price into early 2023, but there are encouraging signs that global gold investment demand remains robust with potential further growth in this sector.

-

In Q3 2022, bar and coin demand hit its highest quarterly level since Q1 2021 — led by Turkey, China, and India — and on a year-to-date basis, Europe accounts for the largest bar and coin demand. Growth among bar and coin gold demand globally highlights a persistent, sticky demand for gold investment. Overall, this is a positive sign that gold investment may see further support, particularly in an uncertain macroeconomic landscape in 2023.

Greater Uncertainty Led by Geopolitical Risk

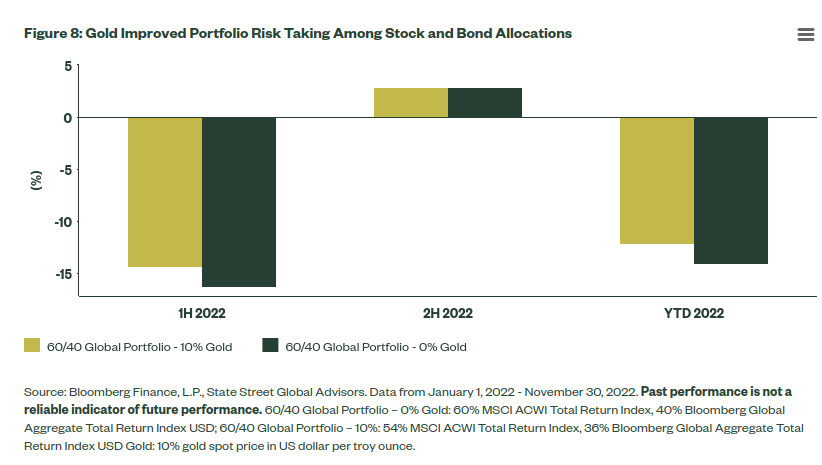

- Focusing only on gold’s -3.3% year-to-date return overlooks the benefit gold brought to diversified portfolios. 2022 saw an equity bear market, the Russian invasion of Ukraine, multi-decade-high inflation, and a breakdown of the traditional negative correlation between stocks and bonds. Taking these factors into account, gold weathered this market environment quite well. In fact, a global 60/40 stock/bond portfolio with a prorated 10% allocation to gold outperformed a portfolio without gold by 1.96% year to date (see Figure 8).

Potential Risks in 2023

The 2022 theme of uncertainty driving volatility will likely remain a top investment consideration in 2023. Potential market risks in 2023 include but are not limited to:

-

Global recession and economic slowdown led by monetary policy missteps

-

Rising and ongoing geopolitical tensions in Ukraine, Taiwan, North Korea, and Iran

-

Elevated commodity prices and rising prices weighing on consumer demand

-

Earnings cycle recession adding to volatility in equity markets

-

Tight labor market and sticky wage inflation may prolong inflation and weigh on global growth outlook

-

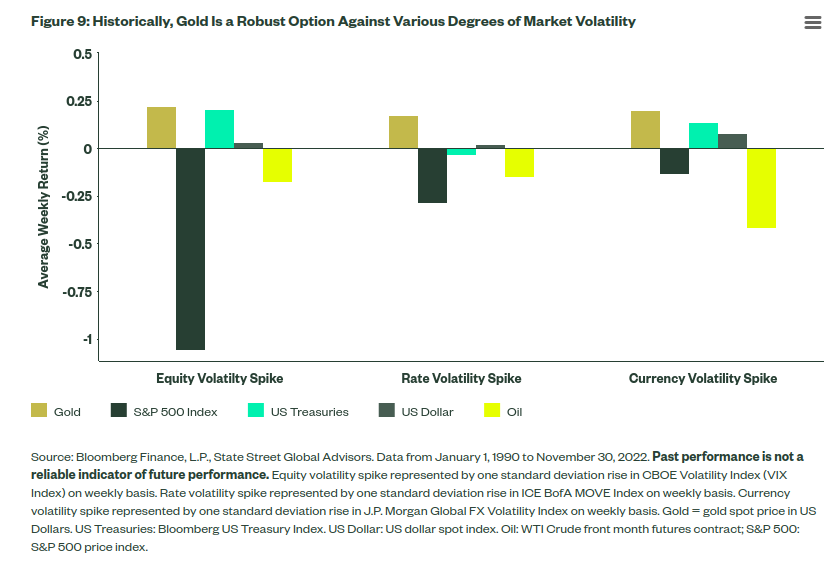

Historically, gold has outperformed stocks, bonds, the US dollar, and oil during periods of heightened volatility. This has been the case based on average monthly returns for not just implied equity market volatility, but also interest rate and currency volatility (see Figure 9). As uncertainty persists, investors may continue to turn to gold as part of a diversified portfolio risk mitigation strategy.

Outlook for 2023

Base Case (60% Probability): Gold sees a potential trading range between US$1,600/oz and US$1,900/oz. Under this scenario, the Fed pauses its current interest rate tightening cycle by mid-2023, with US growth slowing more than expected but avoiding a deep recession. As a result, the US dollar weakens slightly while global gold demand remains along long-term trend levels.

-

Bull Case (20% Probability): Gold’s potential trading range is between US$1900/oz and US$2,000/oz. In this scenario, the Fed pivots and begins to cut interest rates in response to deteriorating economic data as the US heads into a prolonged economic recession. The US dollar moderates from its peak, and global demand for gold exceeds long-term trend levels, led by investment flows.

-

Bear Case (20% Probability): Gold’s trading range slides closer to pre-pandemic levels, from US$1,500/oz to US$1,600/oz. Under this scenario, the Fed proceeds with its aggressive tightening path to bring down inflation while avoiding recession. Meanwhile, investment demand for gold falls as risk assets rally, and gold demand in China weakens throughout 2023 due to its zero-COVID policy and strict lockdown measures.

-