I often hear that good defence is great offense in the stock market. How to actual create a defense mechanism. Pls share some actionable insights as examples to understand this phrase better. Thanks,

Diversifying one’s wealth into a variety of assets / asset-classes comes to mind.

Diversification initially sounds like a defensive strategy,

as one does not chase a single asset/asset-class that is currently providing the maximum returns.

However, diversifying judiciously, improves the chances of limiting the overall drawdown of the portfolio. Combined with compounding over the long-term, one stands to achieve higher returns than other portfolios concentrated into a single/limited asset/asset-classes.

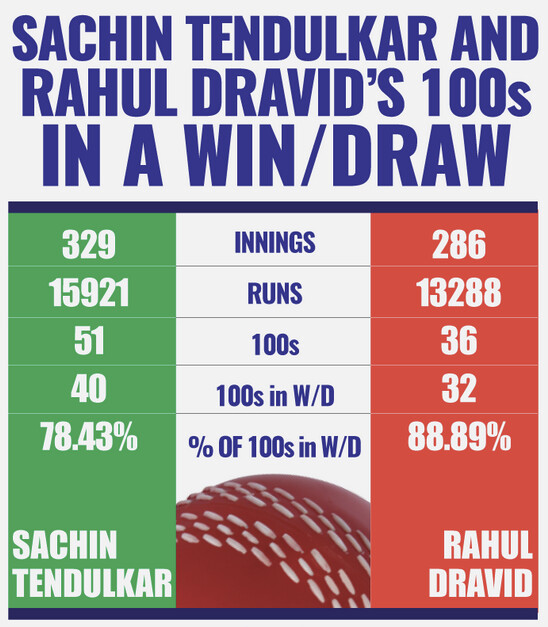

Good defense is great offense. ![]()

Old-school cricket fans out there will remember a similar aspect at play…

Dravid’s centuries in a draw or a win

is a significant 10% higher than that of Tendulkar’s.

[ Source ]

1 Like

If you have a 100, how’d you split across assets? I m not going to copy, but just thinking on how this can be looked at. Personal finance is, after all personal.

Purely from a risk perspective, here’s a handy list i like to use. Starting from the least risky asset classes, and building-up. This works very well if one has a source of income apart from the investments themselves.

Another aspect to consider is whether to adopt the philosophy of Seneca’s barbell that was most recently popularized by Nicholas Taleb’s Anti-Fragile.

Basically, If investing in various instruments to maximize returns, while…

- …lowering overall risk

- …ensuring predictable-income / future-assets

…then the barbell approach can be of relevance in this context/scenario.

Attempting to extract a few additional points of return

by investing in a “middle-of-the-road” somewhat riskier proposition

is usually worse than explicitly splitting one’s investments into 2, and,

- ,continue investing the fraction that one cannot afford to lose.

- at zero risk (as near zero in reality as possible).

- ,investing the fraction that one can afford to lose.

- at a significantly higher-risk (as high as one wishes/expects overall returns to be)

PPS: This barbell approach is also applicable outside of purely financial scenarios.

4 Likes

In the ‘barbell approach’ link that you have shared, there is this line ‘The barbell strategy advocates investing in a mix of high-risk and no-risk assets while ignoring the mid-range of mildly risky assets.’

If a retiree has this portfolio of half equity MF and half debt MF and wants to pull out money for his monthly expenses from this portfolio, do you know of a systematic way to pull out, so that his needs are met and his compounding also is happening. Your thoughts would be appreciated. Thanks,

Since, the focus in the rest of the comment is on what a retiree must do,

the first question is whether they even need to adopt a barbell strategy at all?

Does the retiree need to maximize their returns?

Or are they looking for other aspects, like (but not limited to)

- Further minimizing their risk even at the cost of ignoring some potential gains?

- Minimizing the time they need to spend on managing their finances?

- Minimizing the need to vary their expenses/lifestyle based on external factors?

- …

Based on the limited details available in this thread so far,

too broad of a question to answer comprehensively.

Here’s an overview of a few ways to model expenses/withdrawals during retirement.

One key aspect is - Is one living well within their means?

Does one have a diversified portfolio?

If yes, does one need to realize any of the gains from it, to meet ongoing expenses,

or can remain invested / re-invest and further compound?

Also a couple of calculators to try out some numbers and see how it goes.

In both the calculators, do checkout the assumptions made by each.

1 Like