We just shared this on Twitter. When the markets are going up, we all feel a bit of FOMO (fear of missing out); after all, we’re humans. But acting on that FOMO rarely ends well. Unless your primary job involves looking at the markets, it’s best not to worry about market movements, especially in bull markets. Building a simple, diversified portfolio and then doing something useful in life is the best thing for most investors.

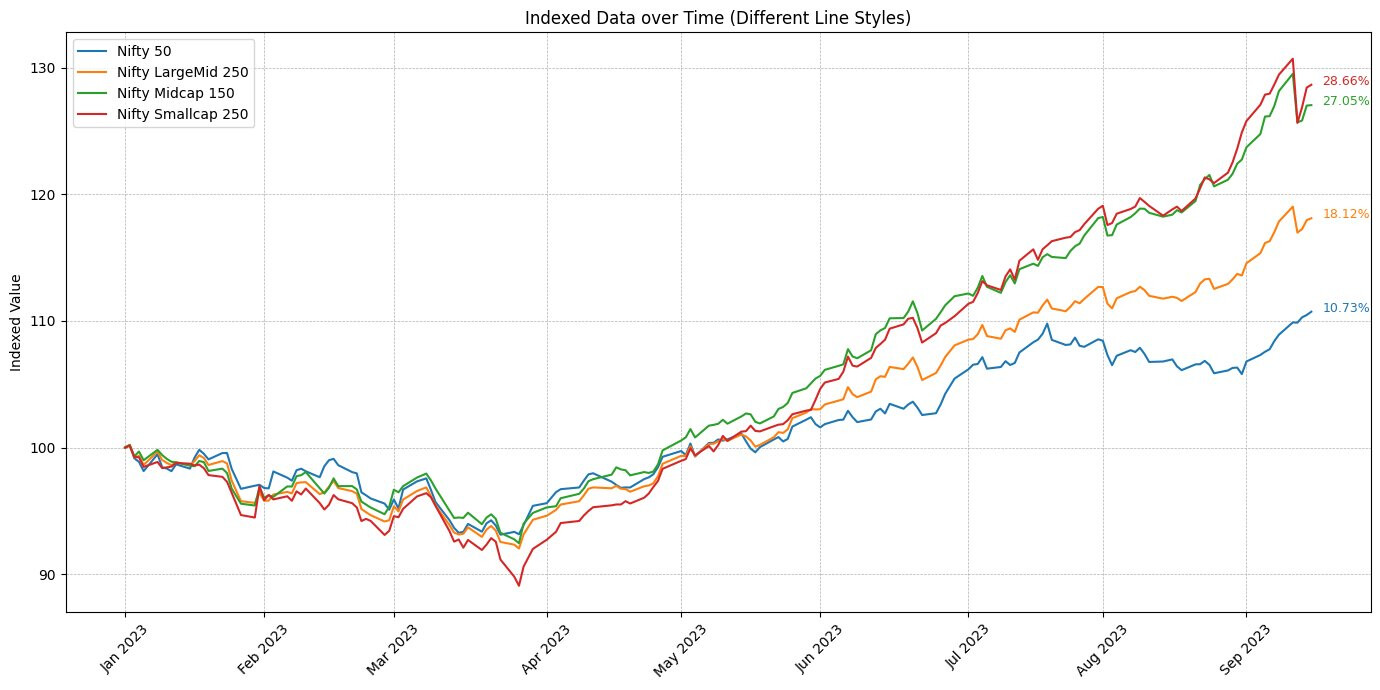

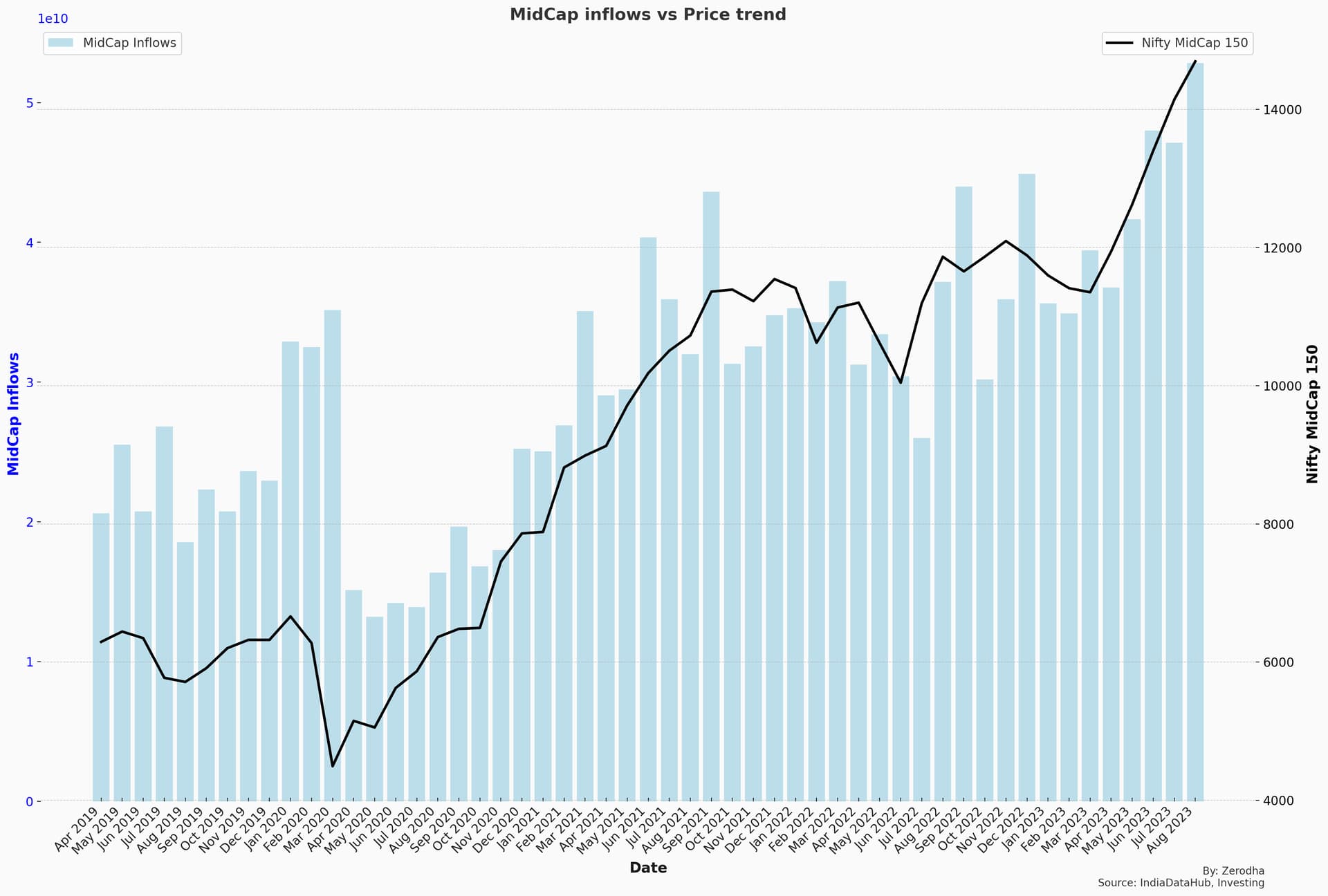

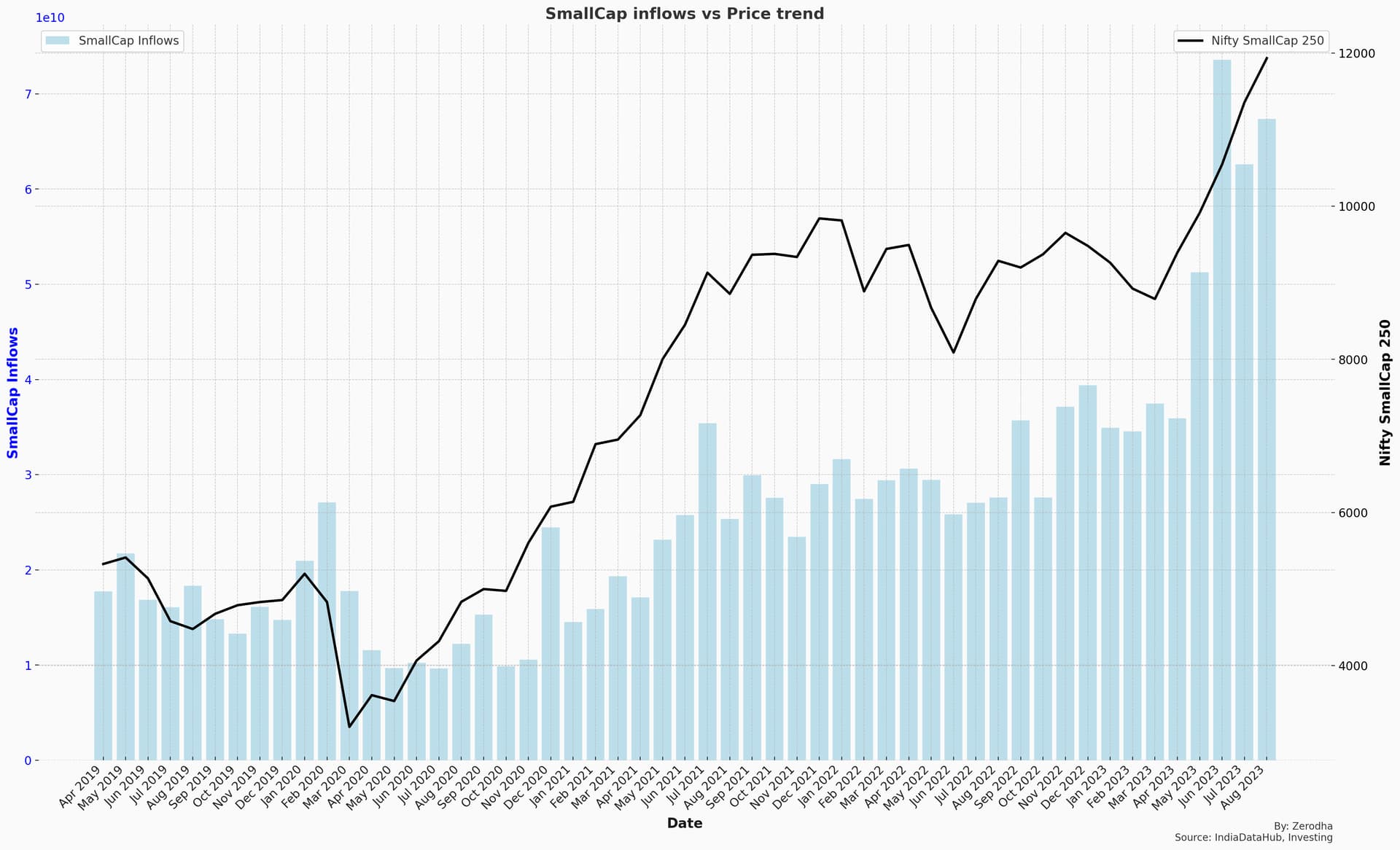

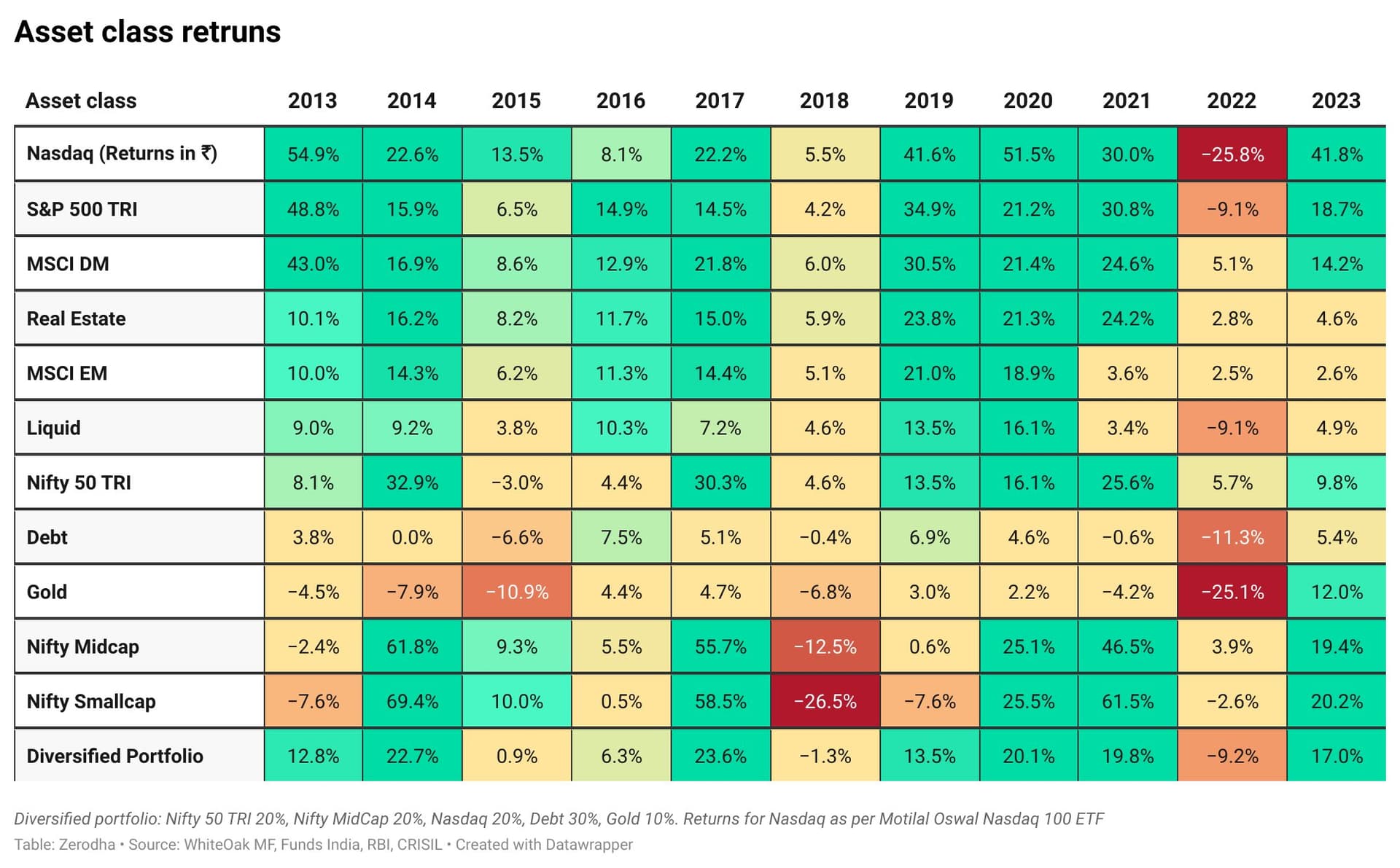

Mid-caps and small-caps have risen spectacularly in 2023.

Whenever there’s a lot of exuberance, it’s wise to remember this quote:

“Good times become good memories, but bad times become good lessons.”

Whenever something goes up, retail investors chase performance, which ends in disappointment and tears.

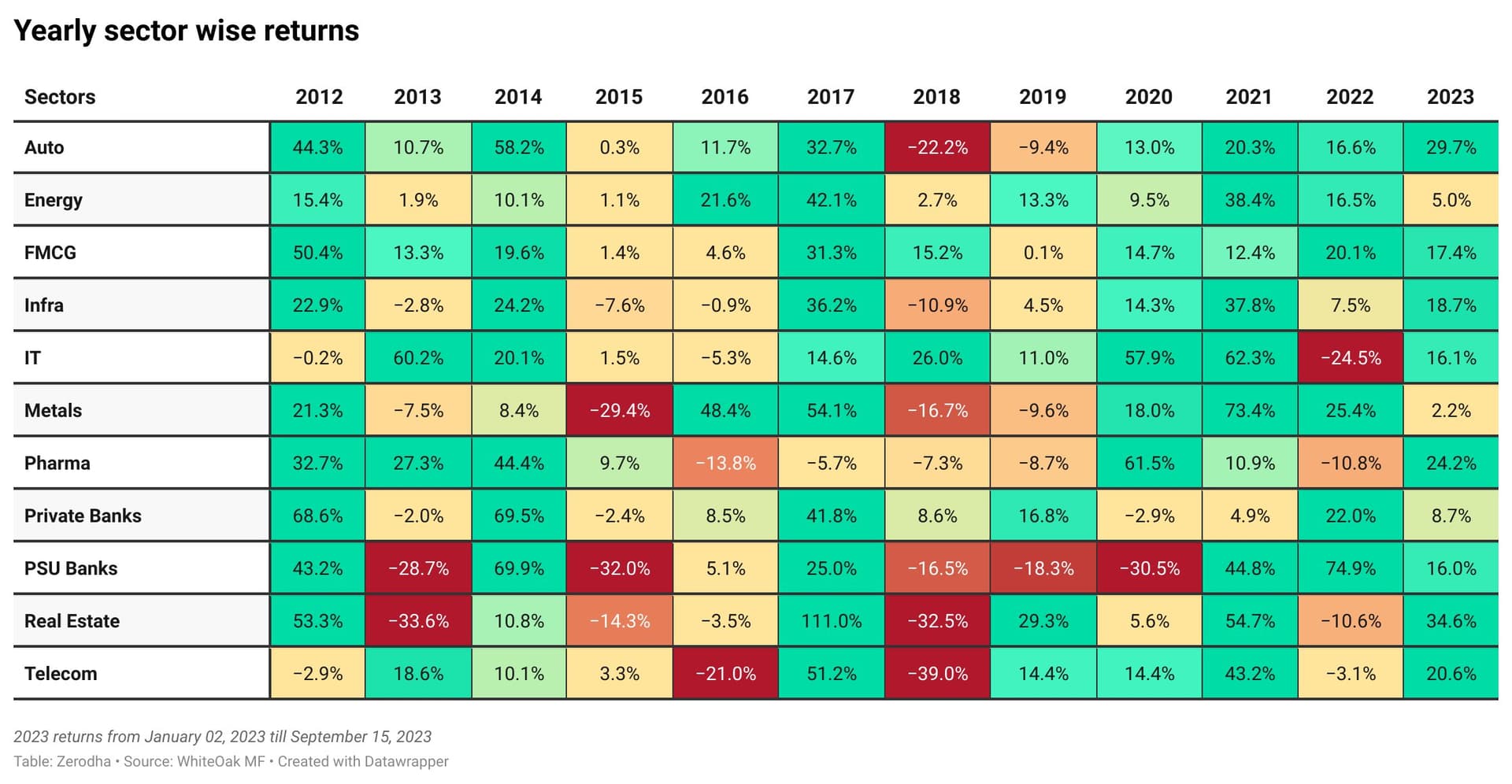

Nothing works all the time. Trying to chase performance and timing is a fool’s errand for most people. Diversifying across asset classes and sectors and doing something productive in life is the best things for most investors😬

Investing is a constant fight against human nature. You will be constantly tempted to chase performance and tinker with your portfolio. But with a few exceptions, the more activity in your portfolio, the lower the returns.

Resisting the pull of fear and greed is what makes investing easy in theory but a nightmare in practice. This is why you get paid a higher premium compared to just keeping all your money in a fixed deposit ![]()

Think of it this way: if you ignore market noise, stop obsessing about market moves, have a sensible asset allocation, and have a long-term perspective, you will automatically be better than 60-70% of all investors.

As Morgan Housel says: