There has been a lot of people on internet suggesting to park money in Gsec as the interest high cycle is going on and due to sovereign guarantee, etc.

But the current rate of GSec are highly overpriced in my opinion.

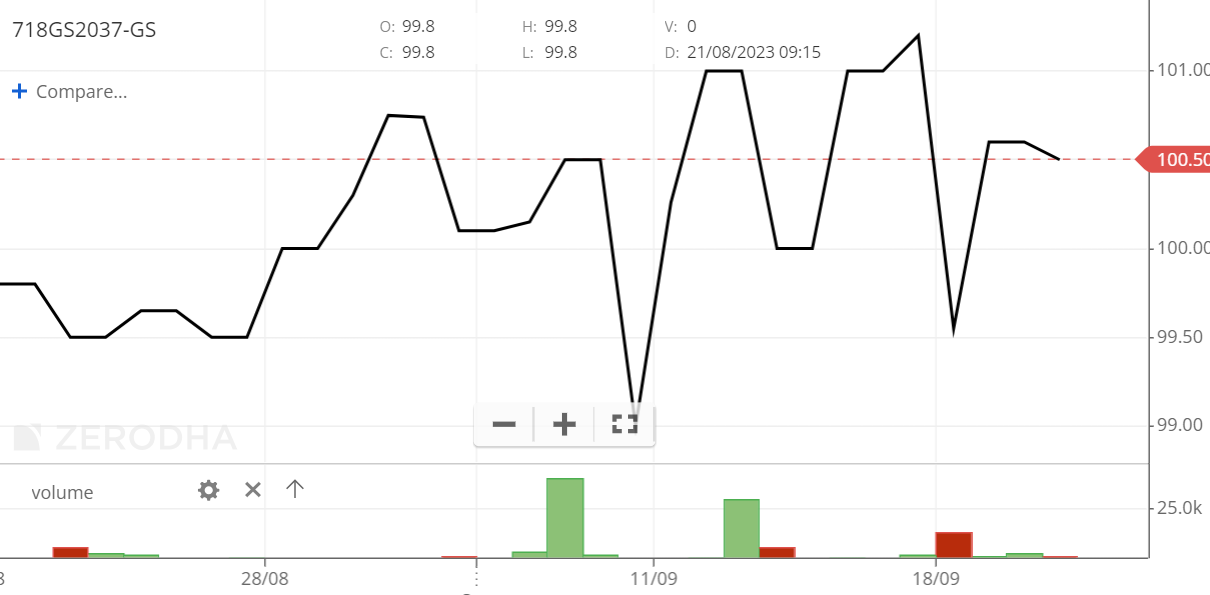

Let’s take 718GS37A23 for example.

I bought 200 units last week for ₹ 20,976.

The half yearly interest that I am supposed to get on 8th Jan 2024 and subsequently on 8th July 2024 is only ₹ 718.

The current market price for this bond per unit is ₹ 100.5, for 200 units it is ₹ 20,100.

If the price of the bond remains constant and if I sell the bond after receiving two interests. XIRR would be 3.32% only. I think I made a very poor investment, please let me know if I am missing something here.

Yes, purchasing 718GS31A23 at INR 104.88 per unit is a poor investment.

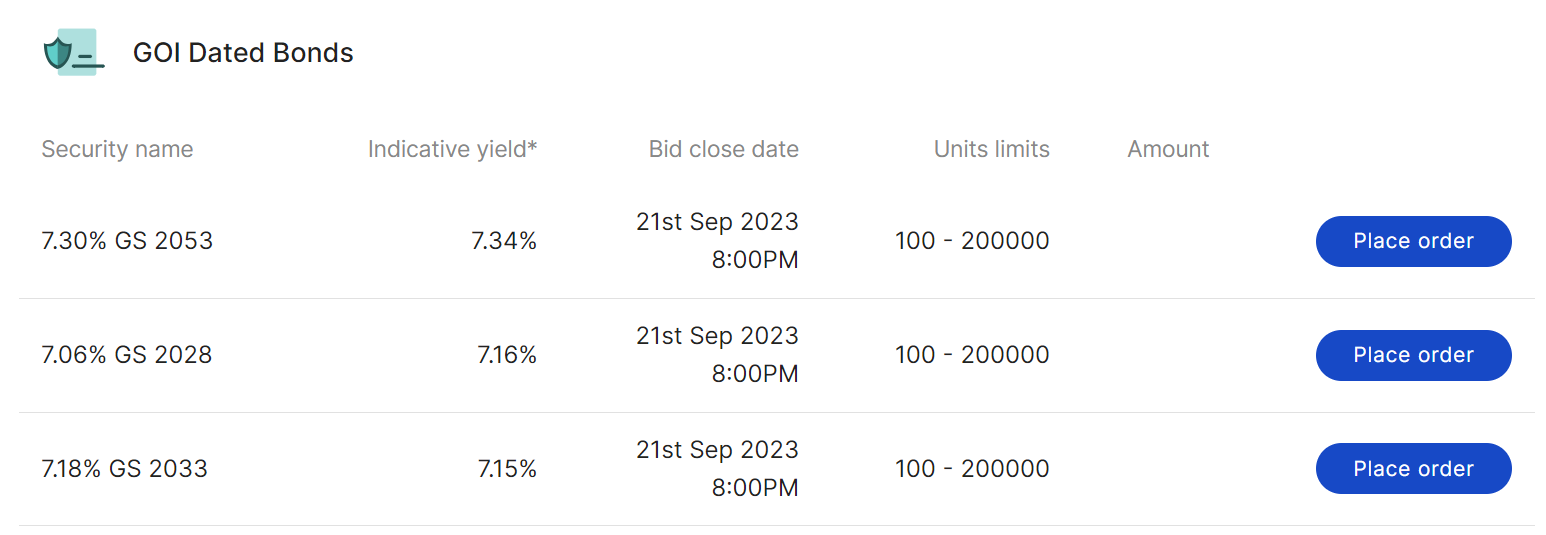

There are >1000 GSECs, T-Bills, SDLs, and STRIPs.

Many of them often trading at a discount on their face-value. (not at a premium as was the case above).

Don’t listen to suggestions of lot of people on internet.

Let’s get some concept cleared first:

Why would you buy a bond maturing in 2037 (14 year duration) and think about selling it in a year?

If your need is short term, you should invest in short term investment, not in long duration bonds like GSec with 14 yrs maturity.

First be clear what is your investment objective and then invest accordingly. Don’t go with what people are saying.

If you are going to hold this bond for 14 years, it will give pretty decent return. If you invested in it for short term gain, it wasn’t a right choice.

Now let’s come to math:

How did you bought this? In secondary market?

I don’t see its price crossing 102, not sure how did you ended up buying it at almost 105?

Or you put in a bid for auction and 20976 is the amount blocked by Zerodha?

For auction zerodha generally block higher amount which is released at a later date. So your buying price will be much lower and returns higher.

Do not use amount blocked as buying price, wait for actual price to calculate.

Also do not calculate xirr for 1 year for a bond which is maturing 10+ years later. Calculate for actual duration.

If your needs are for short term, invest in T-bills, not in long duration Gsec.

The at-par price is Rs100. If you buy it at 100 you will get the exact interest rate as mentioned in the issue. If its 718 - you will get 7.18%, If its 654 you will get 6.54%

If you buy at a higher price say 104, the final yield will go lower + you will incur a capital loss. 718 will give you an yield of 6.77 after including the capital loss.

If you buy at a lower price say 97, the final yield will be higher + you will get a capital gain. 718 will give you an yield of 7.51 after including the capital gain.

I have no idea how you paid so much money for 7.18GS2037 in the period when you said you bought them. This security was auctioned by RBI on September 14 and by RBI’s own data the price for non-competitive bids was 99.36 (Reserve Bank of India - Press Releases). Unless you place a market order on NSE/BSE or paid some brokerage, I find the price highly unbelievable.

There is little bit of an issue with trading Gsecs because RBI and the exchanges have not coordinated in creating a uniform platform for trading them. If you are interested in trading gsecs, you should use NDS-OM. You can find the daily trade data of various securities on the NDS-OM page and historical data/daily yield across tenors on CCIL website. I find this much more user friendly than NSE/BSE. My problem being that Bonds needed to be traded using yield, but exchanges only use price. Buying gsec on the exchange is useful if you want to use them as margin for you trading account, but that’s about it.

Do not use amount blocked as buying price, wait for actual price to calculate.

Yeah, this was the case. I invested using coin and on the Coin dashboard it still says Total investment: ₹20,976

Following was the sequence of events

2023-09-11T18:30:00Z - Bid placed for 718GS2037-GS, amount blocked ₹20,976.00 2023-09-17T18:30:00Z - 200 Units alloted to my demat account and ₹886.60 credited with message “Difference in Government securities purchase price reversed- 718GS37A23”

I invested a small amount to understand how these bonds work, now I understand it a lot better.

I was exploring holding bonds for a year (for LTCG) and selling them for saving on tax, but looking at the bids I can say for sure the bonds are highly illiquid.

Glad it worked out, and you got some learnings from whole experience

That is a risky strategy, especially with such long duration bonds.

As you rightly pointed out, they are illiquid, besides in this uncertain interest rate movement time, there is a high chance you end up with loss instead of gains.

I would suggest not to get into such long duration bonds, unless you have capacity to hold till maturity, or at least 5+ years.

I think you have answered it well. Last para is the clincher. Most of us are getting confused with what zerodha is blocking. Neither zerodha mentions it explicitly. Many people are shying away from investing in G secs as we are all working out yields basis what zerodha is blocking and it is working out to 4%.