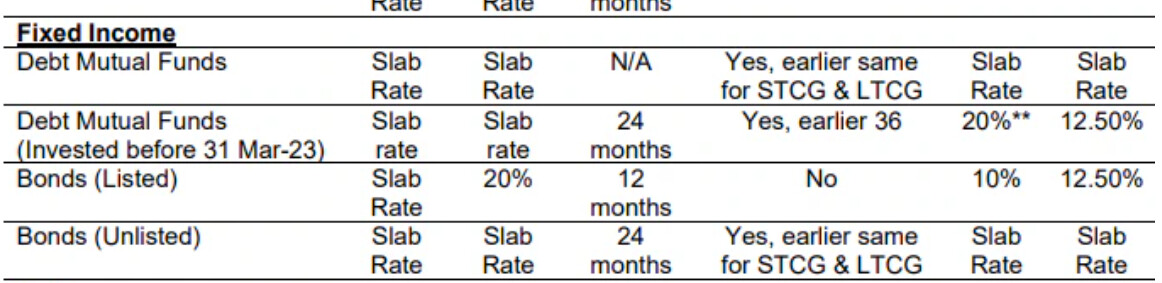

Last year in Budget 2023, FM said they are streamlining debt MF with FDs.

So from 01-feb-2023, time was given up to 31-mar-2023 where investors can buy units and the 20% with indexation benefit would be applicable for Long-term holding that is 3 years.

Those who held Debt MF for > 3 years would continue that benefit.

Purchase after 01-04-2023 would be as per new rule and stcg/ltcg all added to tax slab.

context:

I assume my computation is correct, and if it is correct, for assets which are interest linked like FD/G-Sec and not really speculative like gold / stocks / real estate where prices fluctuate…

Can a grandfather commitment be given 1 year earlier and then get nuked like this a year later?

Looks like 10X tax on this example and these are near real values of NAV checking from portfolio.

The real question is whether the interpretation is correct or not. They had committed to grandfathering the existing holdings.

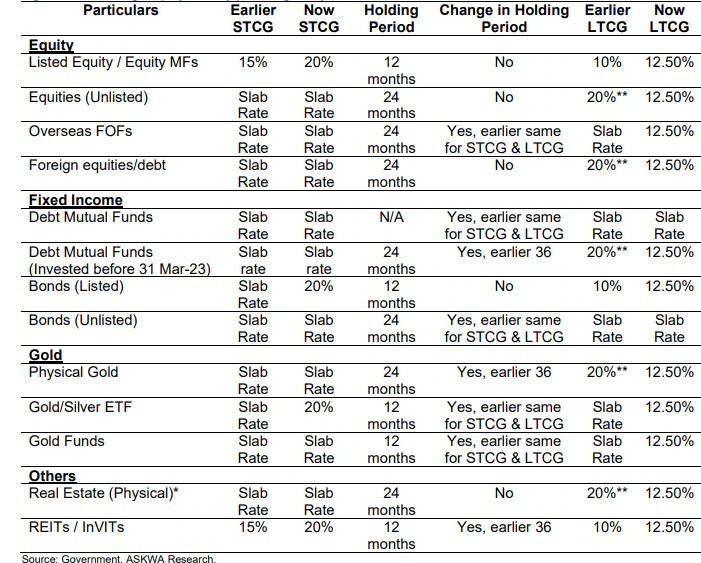

Same like grandfathering of Equities. Now imagine, case where all equity sold is flat 10 %( or 12.5%) from cost of acquisition. in 2018, there was grandfathering and is still in effect.

Ppl have tons of holdings, investing in funds of funds is something for future, but what about the existing holdings?

i will never sell anything - for emergency purpose use SWP - only mutual fund investment will be good - direct stock is still more expensive and emotion attachement will give more tax to govt

just take sometime and calculate the tax with old/new, do you see the same?

Probably thats why markets are silent, trying to communicate with FM and get clarity. Issue i see here is backtracking on the earlier commitment to these MFs.

So if someone is in 30% tax bracket, then even with an interest rate of 7%, the real interest income will be just 4.9%. Seems like govt wants everyone to just invest in equities and forget every other asset class.

That site wont be official confirmation for this anyway. We will know for sure with time.

Yeah, indian equities only. Not too bad if more people invest in equity for retirement i guess if they can stay through tough times, but middle finger to most other assets due to bad/negative post inflation returns.

They are saying the house prices have gone up 5x in last 10 years. Yeah right, maybe only the expensive ones. And so they want to give tax break to people who made money and punish people whose assets didnt move as much.

Anyway, most of this has not much impact on me due to trading income.

Are you sure about this. I think for new investments, debt is on slab - long term / short term. Question is only for older investments.

@Chirag1 I have the same concern, a commitment on grandfathering the indexation benefits on debt mutual funds was given in budget 2023 and all debt mutual funds bought before 1.4.2023 were supposed to get this benefit of LTCG @ 20% with indexation for holding period > 3 years

Now my question is can a commitment given in a budget which is passed on the floor of the parliament be reversed in the next year’s budget?

In my opinion this is an oversight. Some clarification should be sought from the finance ministry, and the best entity to do this should be Edelweiss which sells the majority of debt ETFs specifically the ones that invests in GSec etc

Prima facie, the scenario before 23/7/2024 was to treat debt mutual funds on par with FD s, so compared to tax @ slab rate this seems an improvement where LTCG @ 12.5% for holding > 2 years needs to be paid.

But someone missed the fact that for debt mutual funds bought before 1/4/2023 the tax rate was 20% with indexation benefits for holding period > 3 years, and this was a commitment given in budget 2023 based on which some of us loaded ourselves with debt ETFs in Feb/ Mar 2023.

This would need to be clarified by the ministry/ CBDT and if they don’t give a favorable reply then this needs to be contested or appealed.

The video you posted is old.

This is last year’s scenario where grandfathering was committed.

Only for fresh purchase, both stcg/ltcg would be added to tax slab.