Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

Tokyo drifting apart: The struggles of Japanese auto

It’s a bad time for Japanese automaker Nissan.

In 2024, it posted its second-biggest ever annual loss since 1999. Then, four months ago, Nissan and Honda canceled a potential blockbuster merger. Now, it plans to fire 15% of its global workforce, and is looking to scale back production.

This is not an isolated incident. Toyota, currently the world’s largest carmaker by sales volume, forecasts a 35% fall in profits from the previous year. Most major Japanese automakers have recorded declines in production in the last 12 months, with the overall market falling by 6% — the biggest since 2020.

These are all symptoms of deeper issues in the Japanese auto industry. From sheer global dominance a few decades ago, Japanese companies now find themselves with their backs to the wall, facing increased global competition and geopolitical tensions. But arguably, they have nobody to blame but themselves.

How did Japan build its car industry?

To understand Japan’s plight today, you need to understand how Japan first came to dominate car-making all over the world.

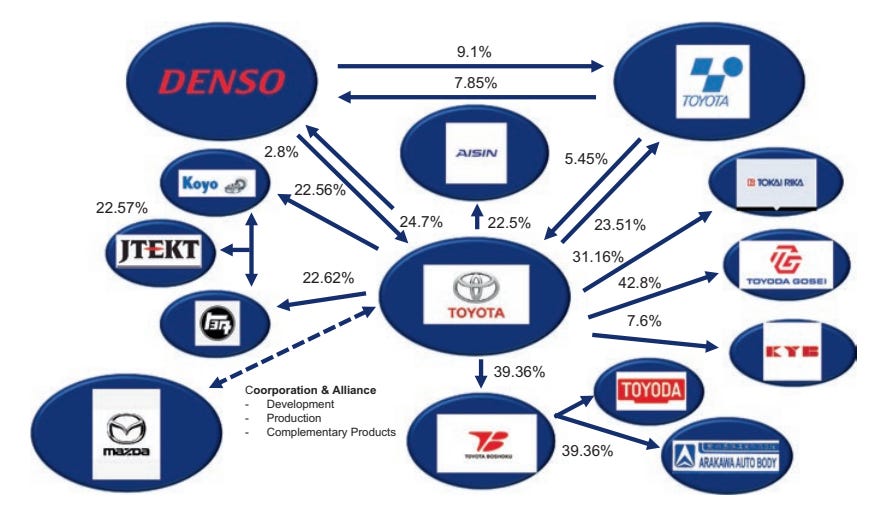

Japanese automakers are usually organized in what’s called a “keiretsu”. A keiretsu is a network of companies characterized by a major car company, linked to a large bank, and surrounded by a network of suppliers that are somehow both loyal to the network, even as they compete with each other. The car company forms the commercial heart of this arrangement. Banks provide financing to the entire network, while the constellation of suppliers provides parts to the company.

Often, these networks have substantial amounts of cross-ownership. This is what Toyota’s keiretsu structure looks like, for instance:

This unique system had powerful advantages. Risks were shared across the members of the keiretsu structure, which made it easy for its members to obtain low-interest-rate loans — both from keiretsu banks and other institutions. These relationships were structurally long-term. If the main company was in financial trouble, its linked companies could help it out. For example, in 2005, members of Mitsubishi’s keiretsu bailed Mitsubishi Motors out with $ 5B.

This keiretsu system was at the heart of Japan’s biggest managerial innovations, which still influence global companies today, many of which are famously associated with “The Toyota Production System ”.

In their heyday, Japanese automakers had flipped the auto manufacturing playbook on its head. Instead of building cars upfront, they decided to only pull parts and fire up the line when orders appeared . That choice forced them to keep inventories razor-thin and costs lean — nothing would be left in their inventories to gather dust.

Everything on their factory floors moved in tight, precise loops. This allowed people on the shop floor to spot tiny hiccups — and fix them — every day. Those micro-tweaks, known as kaizen , constantly improved their processes without big, disruptive overhauls.

There was a second feature underlying the automakers’ success: the industrial policy pursued by the Japanese government, through its Ministry of International Trade and Industry (MITI). It pursued a strategy of exporting cars to developed countries, guided by a devalued currency and relatively cheaper wages.

MITI provided ample amounts of artificially cheap credit to large firms. For example, between 1956 and 1966, it gave $50 million in low-interest, long-term loans to auto parts manufacturers. Right after World War II in 1949, the Central Bank of Japan bailed out Toyota from ruin. It also gave out huge subsidies and R&D tax breaks to auto manufacturers.

The support wasn’t just financial. In the early days, Japan protected its carmakers with import tariffs, quotas, and limits on foreign investment. It also pushed its domestic firms to learn from foreign partners, like Nissan’s technical tie-up with British carmaker Austin in the 1950s.

While this state support was crucial in creating Japan’s world-beating auto industry, it wasn’t without its problems. MITI often intervened in ways that controlled (and even limited) competition, even if it meant creating cartels in some industries. It would ask companies to merge, often even against their interests.

Because of its peculiar history, the Japanese auto market was marked by the lack of a strong monopoly. Its auto sector, for instance, always featured a range of firms — like Toyota, Honda, Nissan, Mitsubishi, Mazda, Subaru, and Suzuki. They refused to merge even when asked to do so by the state. The ecosystem was marked by a fine balance between competition and collusion. Because of this, profits for each company were fairly low.

But it didn’t work like an ideal competitive market. The Japanese valued stability more than cut-throat competition and disruption. This went all the way down to the level of workers — keiretsus offered lifetime employment and generous incentives. But on the other end, the system frowned upon bankruptcy as a natural process to kill inefficient firms. Instead, failed firms would be pushed to restructure and take state support, while keeping people employed.

What would it mean for Japanese automakers if this strategy were to eventually stop working? The answer would reveal itself in a crisis. The keiretsu unravels the early 1990s, Japan’s economy began to face a long recession.

The automaker keiretsus started running into problems. As the recession dragged on, suppliers began drifting away from their long-term relationships, choosing to sell parts outside their keiretsu . Meanwhile, automakers themselves started looking for the cheapest option, whether within Japan or overseas, instead of sticking with their usual network. This shift slowly eroded the very strength of the keiretsu system.

As the domestic market for cars was struggling, Japanese automakers began to cut costs and focus on short-term profits. Till this point, lean manufacturing had been a source of strength for them. However, now, the cost-cutting has become excessive.

Combined with mounting pressure on capital-crunched suppliers, it started causing huge quality control problems for automakers. A core strength turned into a dire weakness.

Toyota, for example, recalled its cars multiple times in 2009-11. Just last year, Toyota, Mazda, Honda, and Suzuki were all found to have provided manipulated data about car safety standards.

Some big automakers also ended up with shaky capital structures after taking on too much cheap debt. This became a serious problem, especially for Nissan. In 1999, struggling to stay afloat, Nissan entered a strategic alliance with Renault and Mitsubishi. This partnership, however, was followed by financial scandals and embezzlement allegations. Things got so bad that, eventually, its CEO had to escape Japan in a music equipment box. The state’s response to industry. The sheer scale of the crisis became too much for even the Japanese state to handle.

For two decades, Japan pursued zero-interest rates to stimulate its economy. It has also implemented approximately 30 fiscal expansion packages since the 1990s. But these failed to solve the auto industry’s problems.

Why is that? This is because of two reasons:

Artificially cheapened credit and fiscal stimuli indirectly propped up badly run firms. The state was reluctant to let these firms go bankrupt, which meant that its spending didn’t always go to productive firms.

In the pre-bubble era, Japan invested heavily in creating domestic production capacity and a large number of car variants. When things turned bad, this turned into structural overcapacity. Cheap capital only worsened this.

In short, Japan ended up spending too much for the returns it was getting. To revive itself, it tried raising taxes. In 2014, it implemented a hike in the sales tax. Within a year, car sales plunged by 5.5%. The Japan Automobile Manufacturers Association (JAMA) openly criticized the hike for hurting demand and delaying recovery.

The state then pivoted, trying to influence its companies to adopt more green technologies. Since 2010, it has enforced stringent fuel economy regulations for its cars. Their cars became more efficient as a result. But, at the same time, the regulations made it more expensive for consumers to maintain their cars.

It paired these regulations with industrial strategy. The government provided incentives and subsidies for two technologies: fuel-cell and hybrid electric-gasoline vehicles.

The first of these was an outright failure. Fuel cells run on hydrogen, generating electricity to power the car. Starting in the 2000s, Japan pushed for more Hydrogen-powered cars and the infrastructure needed to produce hydrogen. But hydrogen is expensive to produce, store, and transport, while fuel cells themselves are fairly costly to make. Due to these high costs, fuel-cell electric vehicles (FCEVs) have not seen widespread adoption. Only 8,283 fuel cell vehicles by the end of July 2023 — a far cry from the 800,000-vehicle target set for 2030. Because of this lack of demand, Japan didn’t invest in setting up more hydrogen infrastructure either, effectively dooming the project.

On the other hand, Japan did succeed with hybrids. Japanese automakers saw them as a more effective strategy for low-carbon-vehicle sales than EVs. For example, Toyota followed a “multi-pathway” strategy towards decarbonization, which involved a mix of hybrids, fossil-fuel cars, and EVs.

But this success came with an opportunity cost. Japan neglected battery-electric vehicles (BEVs). And this, as we’ll soon see, became a key vulnerability.

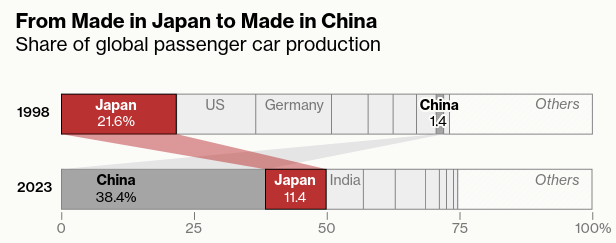

The challenge of Chinese automotives

Ironically, the rise of China’s auto sector was owed, to some extent, to Japan. To survive their domestic market crisis, Japanese automakers looked to make investments overseas. China invited them to make joint ventures with their domestic firms.

Only China dictated its terms to these companies. It negotiated for access to advanced manufacturing techniques and production know-how in exchange for market access. This helped China build a formidable fossil-fueled car industry.

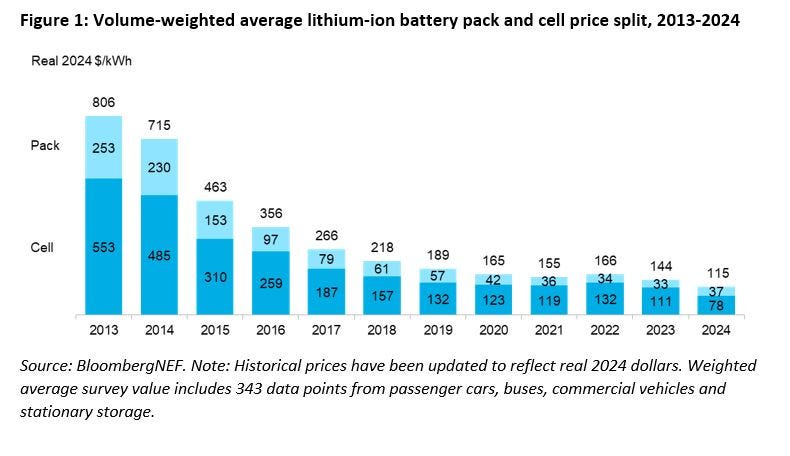

But unlike Japan, in the 2000s, the Chinese state prioritized building BEVs. They made lithium battery research a key component in their five-year plans. From 2009 to 2023, the Chinese government provided over $230 billion in subsidies and tax breaks to companies in the full value chain of BEVs, from battery companies like CATL to fully vertically integrated carmakers like BYD.

The cost of lithium-powered battery packs fell dramatically.

Despite the uncanny similarities with Japan, the Chinese auto industry does have features that distinguish it from Japan.

One big difference is how cutthroat the EV competition is in China. Unlike Japan, where stability was prized, Chinese companies are locked in a “survival of the fittest ” race, constantly trying to outdo each other. The pace of change is breakneck — new models, better tech, faster improvements — compared to Japan’s more measured, incremental style. And the Chinese government is generally more willing to let weaker firms fail, unlike Japan’s cautious approach to bankruptcy.

Secondly, many of China’s car-makers were state-owned . Many of Japan’s joint ventures with Chinese firms were with state-owned companies. These state enterprises became an important driver of Chinese control over the BEV supply chain. Today, they manage the upstream chain, which involves raw material, while the downstream chain (involving car manufacturing) is dominated by private players.

China’s system pushed many of its auto companies to failure. But those that thrived, like BYD, went for high levels of vertical integration, where they control most of their supply chain — a contrast to the keiretsu approach. This allowed Chinese firms to reduce costs, shorten development cycles, and maintain quality control.

In the space of a generation, these companies would come to threaten Japanese auto makers themselves.

Japan on defense a strange twist of fate, it is now Japanese carmakers that are looking to establish key partnerships with Chinese firms to gain access to their EV technology:

- Nissan has recently developed its new EV model (called N7) with the help of its joint venture with Dongfeng.

- Honda has collaborated with Chinese battery-maker CATL to develop lithium-ion phosphate batteries.

- Toyota has recently developed its compact sedan bZ3 in collaboration with BYD.

The Japanese government is now trying to scale homegrown EVs. Last year, it announced a $2.4 billion subsidy package to enhance its EV battery production capabilities, aiming to increase battery production capacity by 50%. It has rolled out a list of R&D incentives and tax reductions for companies investing in BEVs, and aims to replace all Japanese-produced cars with EVs by 2050.

But you have to wonder — at this point, is it all too little, too late?

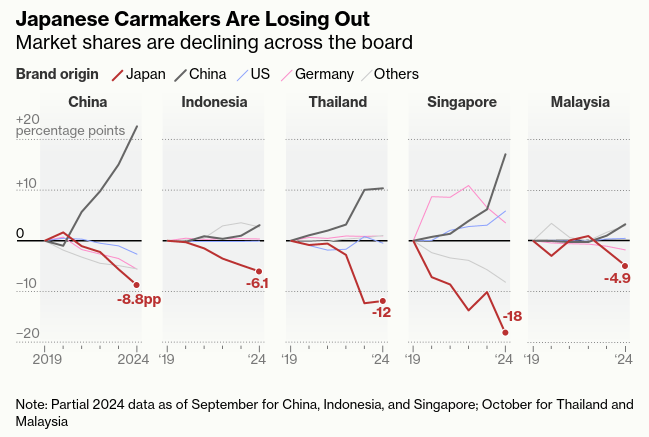

In 2023, even with some growth, battery EVs made up just 2.2% of all passenger car sales in Japan. Meanwhile, Chinese brands are tightening their grip — not just in the West, but all over Japan’s neighbourhood. Meanwhile, within China itself, the share of Japanese auto makers has nearly halved from as recently as 2020.

As tensions between China and the U.S. rise, Japan is trying to break free and build its own BEV tech. But for now, it’s still heavily dependent on China for things like batteries. On top of that, Japan’s population is aging fast and shrinking — a tough backdrop for any long-term revival.

The road for Japanese carmakers has never been more foggy.

What the Israel-Iran escalation means for markets

Early on Friday morning, Israel launched a massive military strike against Iran, targeting nuclear facilities and military installations. That’s what we know right now. By the time this piece gets to you, things may have escalated substantially.

Now, we talk about the markets at The Daily Brief , not about war. We don’t have anything particularly intelligent to say about military strategy. But an event like this hits your wallet, too. This could be a critical moment that upends global energy markets — perhaps even in ways you don’t expect.

Let’s break down what happened, why it instantly sent oil prices up by more than 7%, and what this means for everything from your gas tank to food prices around the world.

The attack and immediate response

So here’s what we know at the time of writing this. On Thursday night, in what Israeli Prime Minister Netanyahu dubbed "Operation Rising Lion ", Israel reportedly deployed over 200 fighter jets to hit more than 100 targets across Iran. These were all crucial sites: uranium enrichment facilities like Natanz, military command centers, and missile production sites.

The choice of sites sets these attacks apart from previous exchanges. Israel didn’t even try to avoid Iran’s nuclear sites; they went straight for them.

The attacks took a serious human toll. Several high-ranking Iranian military commanders were reportedly killed. Various Iranian nuclear scientists, too, reportedly perished. There have been some civilian casualties as well, including children.

In response, Iran’s Supreme Leader Ayatollah Khamenei promised “harsh punishment” — while the country raised its ‘red flag of revenge’. Within hours, Iran launched over a hundred drones toward Israel.

At least to us, this doesn’t look like a small skirmish. Netanyahu claimed this was a fight to “roll back the Iranian threat to Israel’s very survival,” and suggested that the operation would continue “for as many days as it takes.” Going by Israel’s recent history, we have little reason to doubt that.

And that means there’s a reasonable chance that tensions stay high for a while. This could easily escalate into a regional war, unless there’s enough diplomatic pressure to contain the escalation. And if that were to happen, you shouldn’t just expect a conventional exchange of blows. Everything in the region could be fair game.

And that brings us to global oil markets.

Oil Markets React

There are a million angles you could dive into, here, if you want to make sense of what’s happening. Right now, we’re just looking at oil markets.

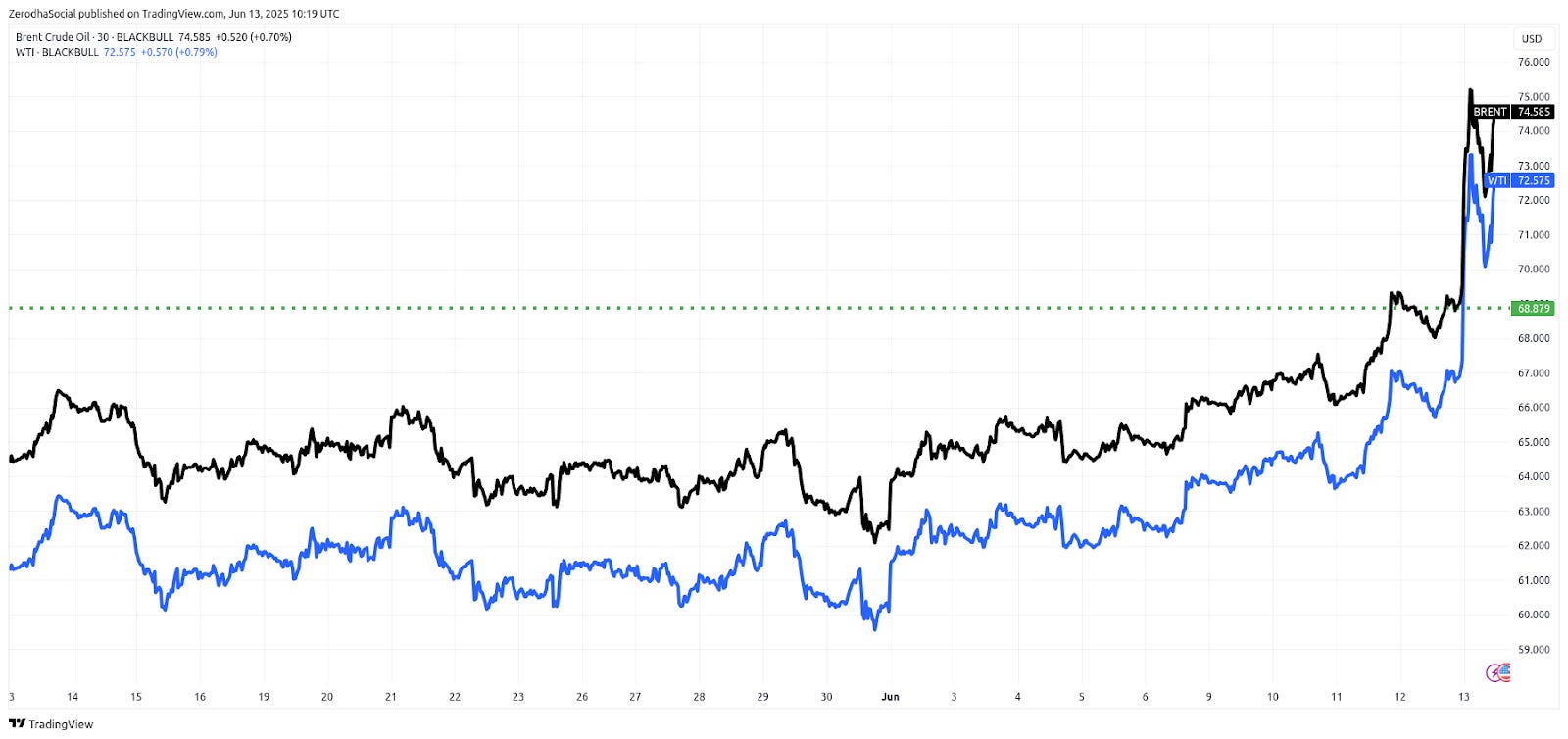

On Friday morning, Brent crude suddenly jumped by over $5 to ~$75 a barrel. This was the highest price it had seen since January. Similarly, WTI crude surged more than 7.5%, to over $73 a barrel.

These are the biggest single-day gains we’ve seen since Russia invaded Ukraine, all the way back in March 2022. And here’s the thing: we haven’t even seen actual supply disruptions yet. These market movements are purely a fear premium.

But why does that happen?

Why does the oil market react so violently whenever there’s a conflict in the Middle East? What, in people’s eyes, is suddenly in danger of going wrong?

The answer lies in simple geography and arithmetic.

The world’s most important oil choke-point

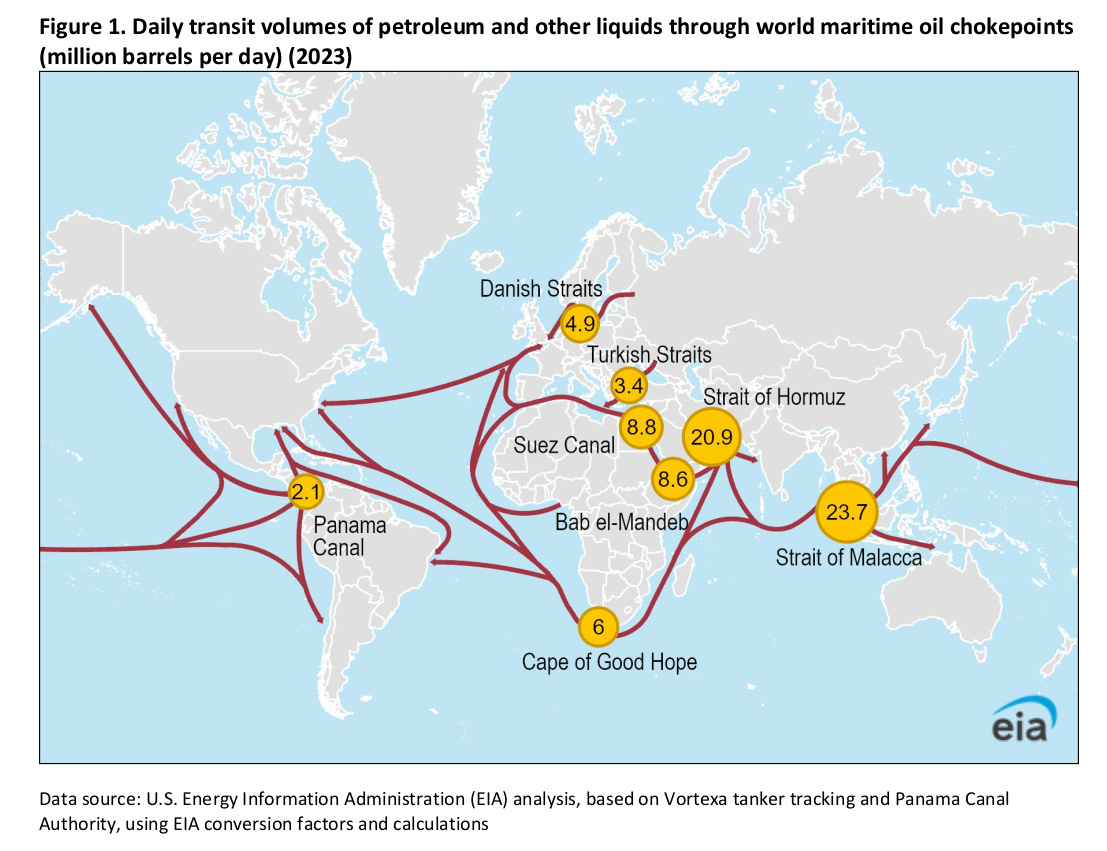

Many of the world’s largest oil producers — Saudi Arabia, Bahrain, Iraq, Kuwait, Qatar, Oman, and, of course, Iran — are arranged around a single sea, called the Persian Gulf. At the mouth of this sea is a narrow strait, just 29 nautical miles wide at its narrowest point, right between Iran and Oman. All the oil produced in the region has to pass through this one tiny waterway.

That’s the Strait of Hormuz — the jugular vein of the global oil market. Every day, about 21 million barrels of oil pass through this strait — roughly one-fifth of all the oil consumed in the world, and nearly 30% of all seaborne oil trade.

A lot of the world is entirely dependent on the oil coming out of this strait. India gets a huge chunk of its oil through this route. So do the other towering economies of the region, like China, Japan, and South Korea. Even the world’s largest oil producer, the United States, still imports about half a million barrels a day from the Persian Gulf through Hormuz — even after its shale boom.

And it’s not limited to oil. About 20% of global liquefied natural gas also transits through Hormuz, mainly from Qatar and the UAE.

Iran sits right by this strait. If it wants, it could disrupt or threaten everything shipped through the strait whenever tensions rise. With the sheer quantity of oil passing through this region, if Iran decides to play spoilsport, it could create a global energy crisis.

Worst-case scenarios: what the experts say

Here’s what this could do to oil prices.

ING’s commodity strategists have painted some stark scenarios. If Iranian oil exports alone get disrupted, even if the Strait of Hormuz is left alone — we’re talking about 1.7 million barrels per day — that alone could cause major price spikes. Now, most Iranian oil exports go to China at discounted prices, but even so, that supply gap will have to be plugged somehow.

The real problem, though, would arise if the Strait of Hormuz faces disruptions. With a third of the world’s seaborne oil at risk, analysts warn that Brent could hit record highs. JPMorgan, for instance, thinks oil could spike to $120 per barrel or more if Iran closes the strait.

At these prices, down the line, there could be significant inflation. For instance, JP Morgan says it could push U.S. inflation back up to 5%. We were finally getting to a point where it looked like we had inflation under control. But a prolonged Middle East conflict could throw all that progress out the window.

What are the alternatives?

Now, to be fair, the risk of a complete Iranian blockade is relatively low. The strait has never been fully closed in recorded history. Even so, what happens if the Strait of Hormuz does get blocked?

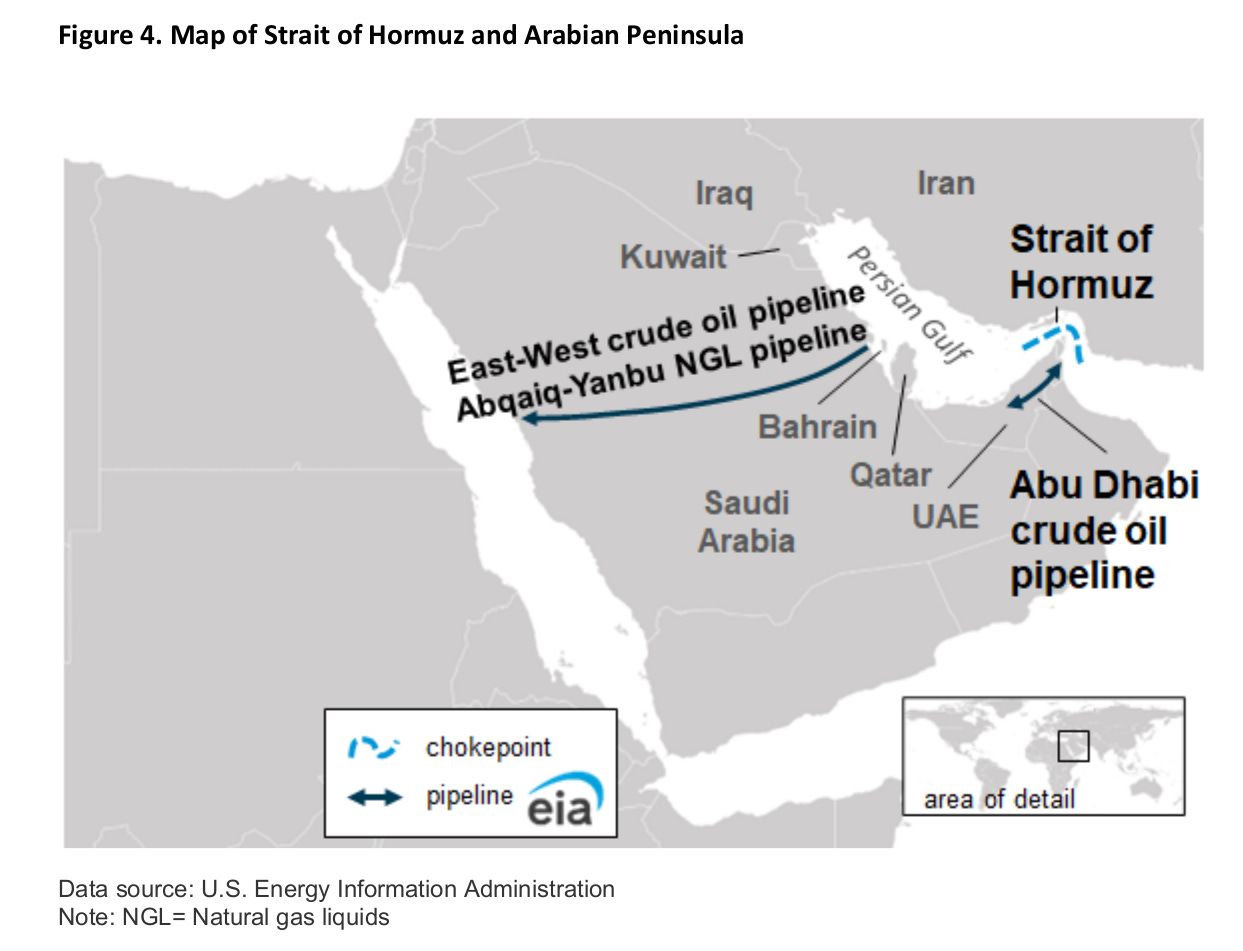

Suddenly, any oil-laden ship destined for anywhere in the world would be trapped. Consider a ship carrying Persian Gulf oil to Europe. Normally, it would pass through Hormuz, then turn around the Red Sea, and cross over to the Mediterranean through the Suez Canal. If Hormuz is blocked, though, that oil can’t even start this journey.

The only alternative would be to transport oil overland through pipelines. And there, the options aren’t great. Saudi Arabia has an East-West pipeline that can bypass the strait. But that can just move about 5 million barrels per day. The UAE has a smaller pipeline to Fujairah.

Combined, these alternatives might pull out about 3-4 million barrels per day, out of the 21 million that normally flow through Hormuz. The world still loses access to roughly 17-18 million barrels per day, with no realistic short-term alternatives.

Iran knows this leverage intimately. By just threatening shipping in those narrow waters, they can still choke off everyone else’s supply. And that gives them a lot of power.

What about safety nets?

Now, the world does have reserves of oil to deal with a situation when new supplies are choked. OPEC, for instance, has spare production capacity of more than 5 million barrels per day, mostly sitting in Saudi Arabia and the UAE. The International Energy Agency also has 1.2 billion barrels in emergency stockpiles across member countries.

In a normal supply disruption, this spare capacity and these reserves could help stabilize markets. But here’s the catch – most of that spare capacity is also in the Persian Gulf. If we’re dealing with Strait of Hormuz disruptions, that safety net becomes useless. It’s like having a fire extinguisher locked in a burning building.

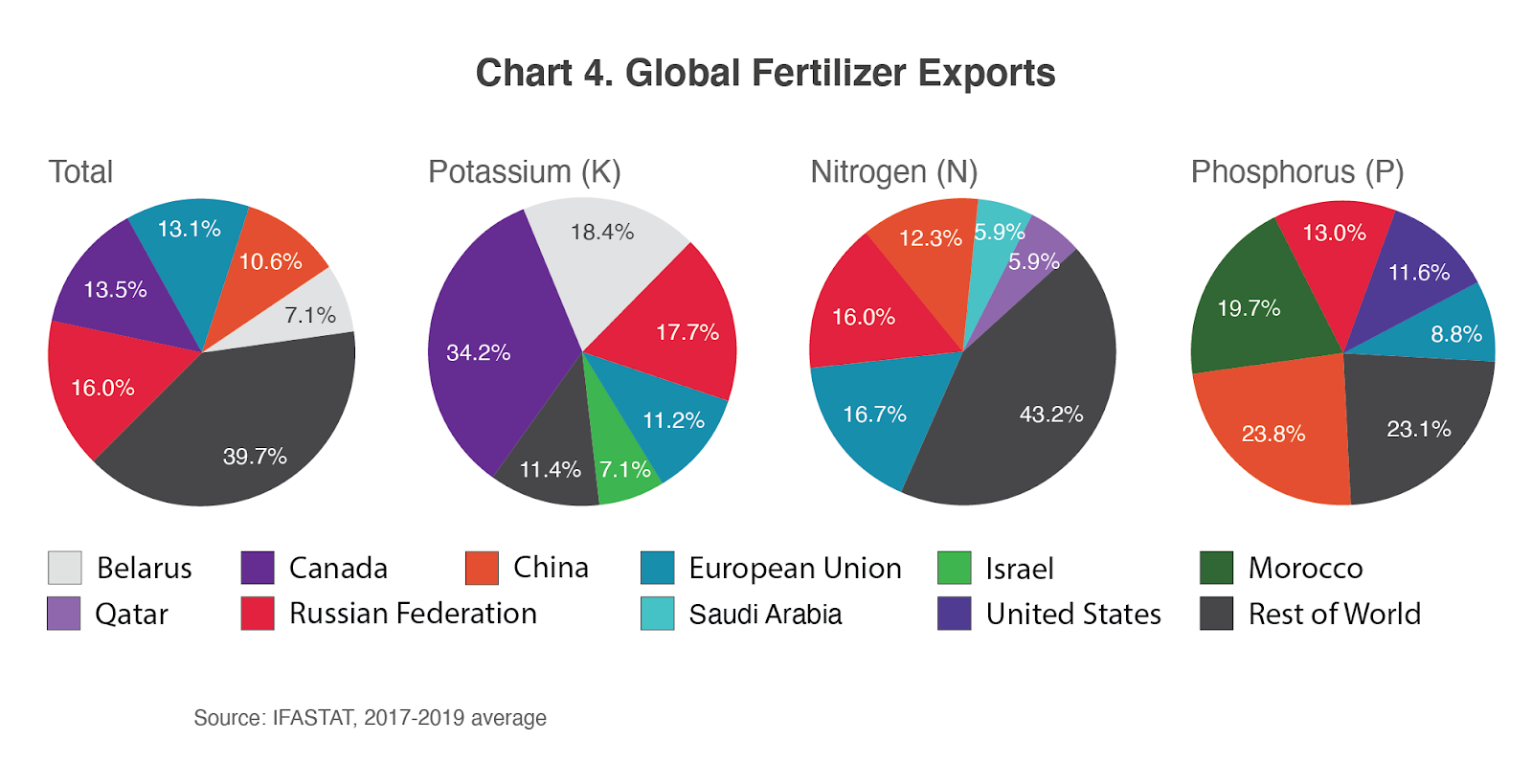

The fertilizer connection you haven’t thought about

There’s another hidden story within this story, which could hit your grocery bill just as hard as higher gas prices: fertilizers.

The Middle East and North Africa region — what we call MENA — is crucial for global fertilizer production. The region produces about 30% of the world’s nitrogen fertilizer exports. And many of its top producers — like Qatar, Saudi Arabia, and Oman — surround the Persian Gulf. These are ripe targets in the current conflagration.

All of this comes against a backdrop of fertilizer prices that are already climbing. According to the World Bank, by April this year, global fertilizer prices were 11% higher than they were last year.

Iran itself is a significant player in petrochemicals — they exported $67 billion worth of oil in 2024, their highest revenue in a decade. And often, you need petrochemicals to make fertilisers. If Iran so wishes, billions of dollars worth of products like methanol, liquefied petroleum gases, and other chemical compounds — essential building blocks for fertilizer production — could suddenly be knocked out of the market.

Leave the Persian Gulf aside. Even if natural gas prices in general go up because of the conflict, fertilisers could take a hit. After all, natural gas isn’t just used for heating your home — it’s the primary raw material for producing nitrogen fertilizers. So, if natural gas prices spike, fertilizer production costs shoot up worldwide, not just in the region, but everywhere. Europe, America, China, India — everyone feels the squeeze. And that means higher fertilizer prices, which drive up food production costs. Ultimately, this could all show up in your grocery bill.

Remember what happened during the early stages of the Ukraine war when fertilizer prices spiked? Food prices went through the roof, contributing to social unrest in dozens of countries. A prolonged Middle East conflict could do exactly that.

Regional wars can have global implications.

Whenever there’s a serious problem in the Middle East, the entire world is nervous — because, in that part of the world, a regional conflict has truly global implications. What started as an Israeli strike on Iranian nuclear facilities could end up affecting everything from petrol prices to food costs. The consequences could last for months or even years to come.

Tidbits

Reliance offloads majority stake in Asian Paints for ₹7,704 crore

Source: Reuters

Reliance Industries, through its affiliate Siddhant Commercials, has sold 3.5 crore shares of Asian Paints in a block deal worth ₹7,704 crore. The shares were offloaded at ₹2,201 apiece, slightly below the previous close of ₹2,208.80. This sale reduces Reliance’s holding in the company from 4.9% in March 2024 to just 0.9%, marking a major exit after nearly 17 years of investment. The transaction comes amid growing competitive pressure in the paints sector and potential antitrust scrutiny faced by Asian Paints. The sizable offload adds near-term supply overhang to the stock, which has underperformed the Nifty 50 for two consecutive years. The move also reflects Reliance’s ongoing capital rotation strategy as it repositions its portfolio.

NHAI plans ₹20,000 crore fundraise via two InvIT rounds in FY26

Source: Mint

The National Highways Authority of India (NHAI) is set to raise ₹20,000 crore through two rounds of its National Highways Infra Trust (NHIT) InvIT in FY26. This marks a departure from its earlier approach of a single annual invocation. The proposed monetization includes 24 highway stretches totaling 1,472 km, with a larger target of ₹50,000–60,000 crore under consideration. These rounds follow a strong monetization record, with the highways sector having already achieved ₹1.58 lakh crore against the ₹1.6 lakh crore NMP-I target for FY22–25. NHAI will also auction assets to private InvITs under the Toll-Operate-Transfer model for the first time. NHIT currently counts over 350 institutional investors, and a public InvIT is in the pipeline to widen participation. This move aligns with the ₹10 lakh crore NMP-II goal set for FY26–30, where highways are expected to contribute ₹3.5 lakh crore.

iPhone Exports from India to the US Surge 3x in 2025 amid trade diversification

Source: Business Standard

Between March and May 2025, Foxconn exported nearly $3.2 billion worth of iPhones from India, with 97% of that volume headed to the United States — a sharp increase from the 2024 monthly average of just 50%. In May alone, iPhone exports to the US reached nearly $1 billion, while March saw a record $1.3 billion, marking the highest-ever monthly figure. Tata Electronics also witnessed a rise in US-bound shipments, climbing from 52% in 2024 to 86% in March-April 2025. Apple reportedly chartered flights in March to ship $2 billion worth of iPhones, and sought faster customs clearance at Chennai Airport, aiming to reduce processing time from 30 hours to 6. These shifts come as Apple prepares for possible tariff hikes in the US on Chinese imports. Foxconn has committed $1.5 billion to expand its manufacturing footprint in India, underscoring the ongoing strategic realignment of Apple’s supply chain.

- This edition of the newsletter was written by Pranav and Bhuvan.

Join our book club

Join our book club

We’ve started a book club where we meet each week in JP Nagar, Bangalore to read and talk about books we find fascinating.

If you think you’d be serious about this and would like to join us, we’d love to have you along! Join in here.

Have you checked out The Chatter?

Have you checked out The Chatter?

Every week we listen to the big Indian earnings calls—Reliance, HDFC Bank, even the smaller logistics firms—and copy the full transcripts. Then we bin the fluff and keep only the sentences that could move a share price: a surprise price hike, a cut-back on factory spending, a warning about weak monsoon sales, a hint from management on RBI liquidity. We add a quick, one-line explainer and a timestamp so you can trace the quote back to the call. The whole thing lands in your inbox as one sharp page of facts you can read in three minutes—no 40-page decks, no jargon, just the hard stuff that matters for your trades and your macro view.

Go check out The Chatter here.

Subscribe to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets, both in India and globally.

Thank you for reading. Do share this with your friends and make them as smart as you are ![]()