Got this message on tradingqna . Little investigating and it reminded me of the incident when I had blown my entire trading account on an expiry day in the early 2000’s. Sharing it for benefit of other option traders.

What has happened in the above case is that client had bought 26200 CE and 26300 PE of Banknifty which expired yesterday. Theoretically you’d assume that buying both of this should be equal to 100 atleast on expiry if market closes within 26200 and 26300.

Banknifty was at 26270 at 3.15pm, calls were available at around 55 and puts for 25. Together costing you Rs 80, but theoretically it should be atleast 100. It is very easy to think of this as a risk free trade and take a position by buying both calls and puts just before market close. But this can be disastrous, and here is why.

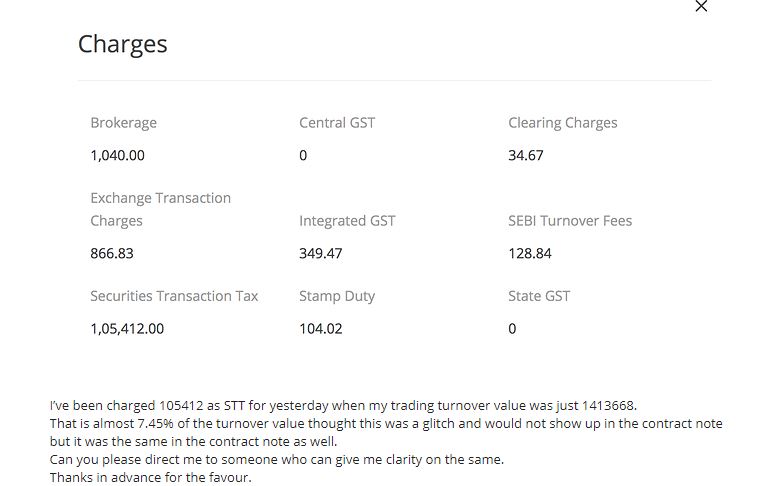

STT for in the money options is 0.125% of the contract value. Almost 32 points for calls and 32 points for puts (Bank nifty). What this means is, even though the theoretical value is 100, if position held to expiry/exercise, it is worth only 36 points (32 on buy calls and 32 on sell calls go away as STT. So 100-64). Now by buying at 80 and letting to expire, you would have got back only 36 after STT - causing a 60% loss on the position.

This post explains the STT issue when trading options. Do read.

ps: The new CTM fix ensures if STT is more than the premium, then it doesn’t eat up more as it can be expired worthless. But STT still eats up exponentially more if you hold buy option positions on expiry and let it exercise.

Long time back, I had gotten into similar position. That too by taking additional leverage thinking it is guaranteed profit - blew up the entire account. Had to go back to telemarketing, and the life lesson learnt that day was

Markets are super efficient with lakhs of professional traders and programs scouting for money making opportunity. If a trade comes across that seems too good to be true or as if it is high return guaranteed profit, it probably isn’t.

Thanks Nithin for sharing your experience and the learnings

I think this even applies to investors also in addition to traders

Things too good to be true should be taken with a bucket of salt (not even a pinch of salt) - we see it in SMS tips on stocks, we recently saw it in a certain buyback of a certain “gem” of a stock, and now might happen in a supposed open offer (my speculation)

People get led astray when they see so-called “promised” profits in this market, at the end of day, nothing is promised, and we need to fight even for 1 rs profit here.

Dear @ksksat, answer of your question lies in the analysis by @nithin. You have to calculate the result yourself by available option premium. The general philosophy is - when expiry is very near and market/stock is not abnormally violent, then market forces bring the option premium value to a point where exercising deep ITM or ITM option will be equal to selling it before expiry. Means either no method will have specific edge or may be squaring off will be little beneficial. Thats why future prices and ITM Option premium often available with the discount to the spot prices at the very end on expiry days.

It will be decided by combined market forces and you are a part of it. Will depend upon last minute calculation by buyers and sellers and also their psychology/temperament. add to the fact whether it is a liquid or not so liquid counter. So someone buying ITM in the last minute may have different reason - Someone buying for squaring off sell position to release margin, someone may have falsely concluded that it is a profitable position, some other may be buying because its really a profitable position and there may be few more reasons, God knows!

If you let contracts expire in the money, you wouldn’t have to pay that exponentially higher STT.

Yes there will be an impact on how the premium trades on the last day of expiry. Today it typically trades at a discount to the intrinsic value because of the much higher STT. Going forward, this discount wouldn’t be there. Also option writers would typically have benefited more slightly because of this higher STT as people come to the market and cover at a discount to intrinsic value. Going forward, this small advantage goes away from the writer.