Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, we’ll tell you why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

- Heads, US wins, tails, India loses?

- The many complexities of India’s corporate bonds market

Heads, US wins, tails, India loses?

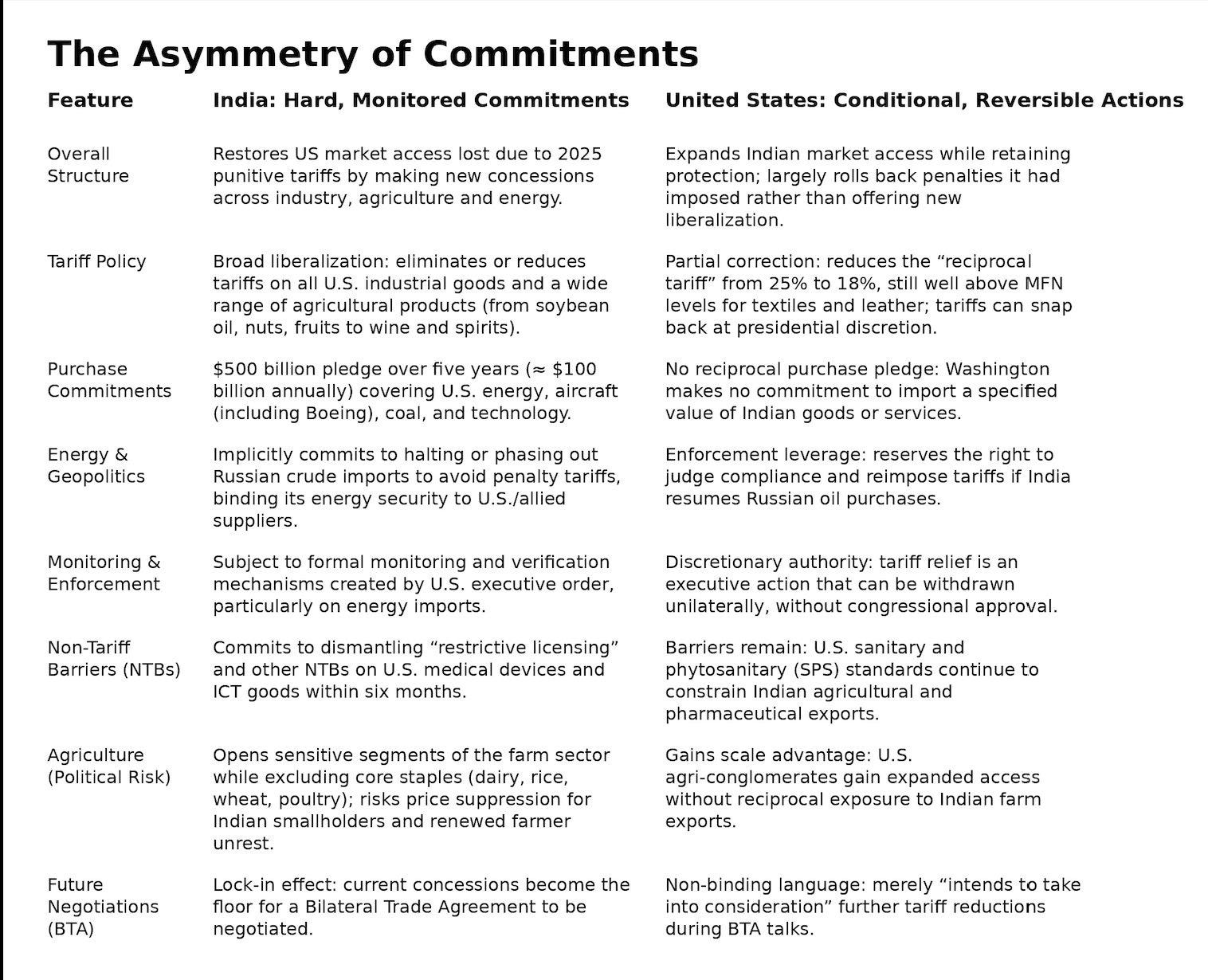

It took roughly a year for the United States to go from diplomatic handshakes with India, to coercing India with steep tariffs — and then, this week, back to something resembling a deal.

So before we talk about this deal, it’s worth briefly recounting the timeline leading up to it.

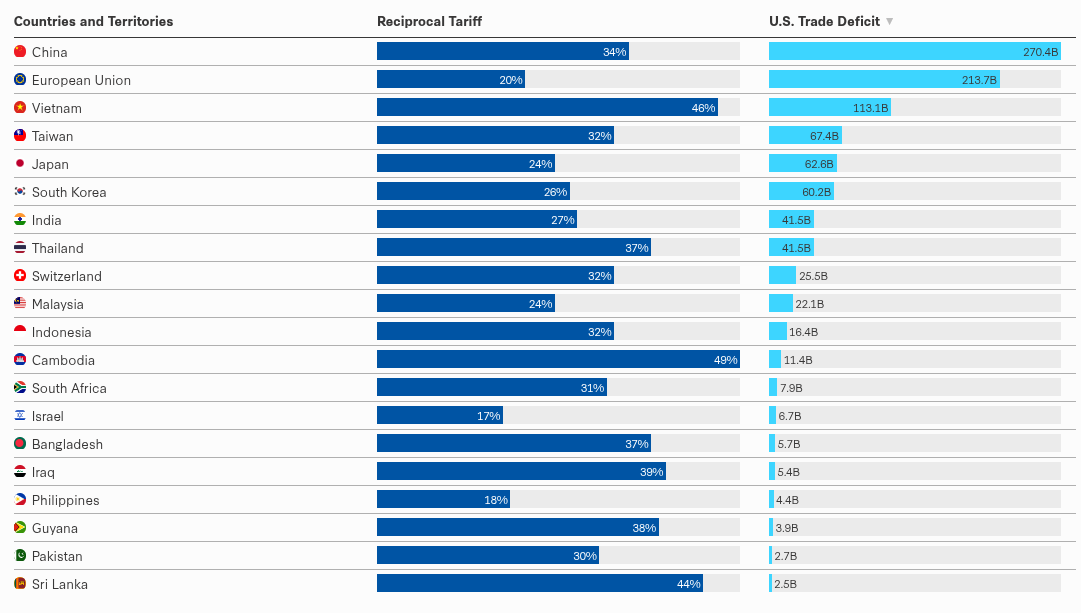

In February 2025, Prime Minister Modi and President Trump agreed to negotiate a trade deal by autumn 2025, with an ambitious target of expanding bilateral trade to $500 billion by 2030. But then, in April, the US unveiled its “Liberation Day “ tariff plan on many countries — including a 26% tariff on Indian goods, with a 90-day pause for talks.

By July, those talks had gone nowhere, and the pause expired. Then, in August, the US slapped on an additional 25% penalty, explicitly citing India’s purchase of Russian oil. In sum, India was now facing a 50% tariff rate .

For six months, Indian exporters bled. Trade volumes to the US fell 18-24%. Gems and jewellery exports plunged 44%. Textiles, leather, and seafood — India’s most labour-intensive export sectors — took the worst hits.

Then came the thaw. By December, India’s Russian oil imports had dropped to their lowest in two years. Talks between both countries were re-opened. And now, in February 2026, an interim trade deal was announced.

However, unlike, say, the recently-signed India-EU free trade agreement, the India-US deal doesn’t feel like a balanced compromise between two parties. If the terms of this interim deal are anything to go by, it’s quite clear that there’s an unequal power dynamic that the US has exploited in their favor.

The trade mix

To understand what’s at stake, let’s start with what the two countries actually trade.

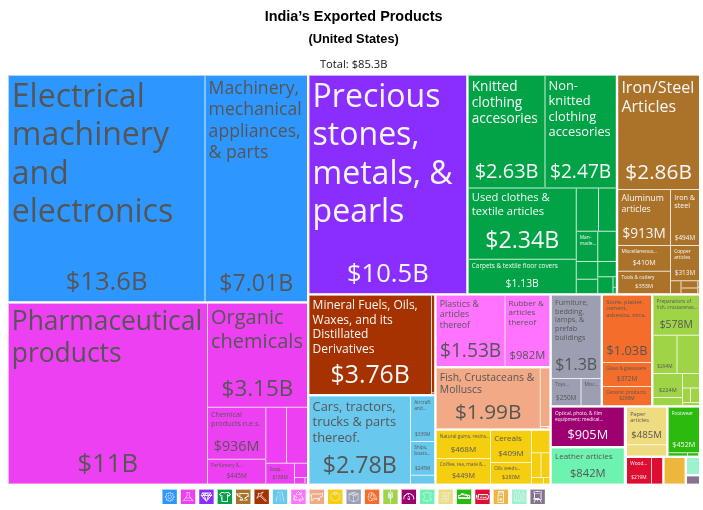

India’s exports to the US are dominated by labour-intensive and mid-tech goods: electronics, gems and jewellery, textiles and apparel, pharma, petroleum products, and so on. The US is one of the few countries that, so far, India has had a consistent trade surplus with — exporting considerably more than what we imported.

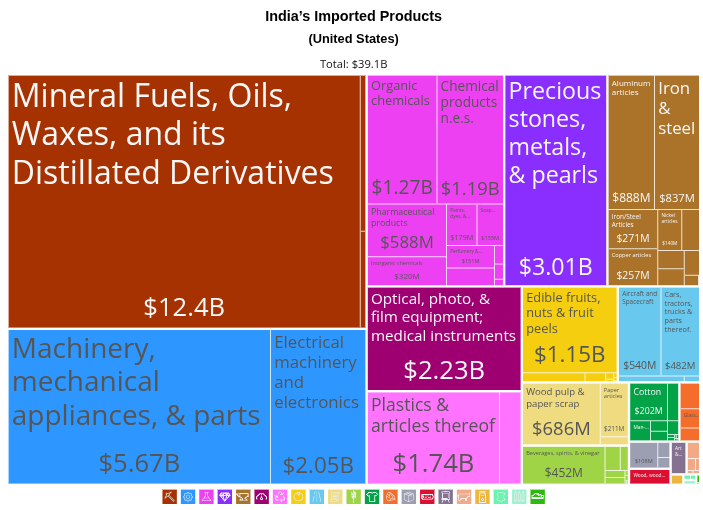

American exports to India look very different: aircraft, oil and gas, machinery, medical devices, defence equipment. These are higher-tech, capital-intensive goods where the US has clear comparative advantages.

There is some complementarity between these two economies. India sells the US things that rich American consumers want . In return, we import from the US the key factors we need for our industrialisation journey.

In our story on the India-EU deal, we mentioned why trade complementarity is important in a trade negotiation. But, somehow, despite complementarity existing between India and the US, it has, to a degree, not factored into negotiations with Washington. It has used the enormous leverage of its rich consumer base by slapping high tariffs on us.

How have Indian exports so far dealt with this? When tariffs hit 50%, Indian exporters didn’t slash prices. As per the Kiel Institute, 96% of the tariff costs were passed through to American importers and consumers. Indian firms maintained their margins, but at the cost of shipping lower volumes to the US.

At the same time, though, our exporters tried to find new non-American trade outlets. Shrimp exporters pivoted to China and Southeast Asia, where shipments surged 60% even as US volumes dropped 27%. Gems and jewellery redirected to the UAE, Hong Kong, and Belgium.

But these were temporary survival strategies, not permanent solutions. Low-margin sectors like cotton garments and footwear — which compete directly with Vietnam and Bangladesh — couldn’t easily pass costs along or reroute supply chains.

Sovereignty over all

Before we get into the terms of the deal, how should we understand it?

Previously, we looked at the India-EU FTA with a sovereignty-complementarity lens. In short, there are goods that India sells that Europe wants, and vice versa — in these industries, free trade is an obvious choice. However, in certain goods, India would want to protect strategic industries (like dairy). The thinking is that allowing foreign imports there might threaten domestic market share, and even create unemployment.

But, while the EU deal had a healthy spread across this spectrum, the US deal is far more lopsided in favor of (American) sovereignty. Let’s start with how it is so with the most striking conditionality: energy .

The 25% penalty tariff on Indian goods has now been removed. But, there’s a condition attached to it: if India resumes Russian oil purchases, the penalty is reimposed immediately. The US will be keenly monitoring whether India breaks this condition.

This is extraordinary. Trade deals routinely address tariff schedules, market access, and non-tariff barriers. But rarely are they conditioned based on how a country plans its energy security. As we’ve covered earlier on The Daily Brief, India began importing Russian crude not because of geopolitical alignment, but because it was extremely cheap.

Besides energy, the interim deal involves a commitment from India to buy $500 billion worth of American goods over the next five years — focused on energy, aircraft, defence equipment, and technology. Plus, all American industrial goods will receive duty-free access to India. But there is no reciprocal commitment from the US to buy Indian goods.

The deal essentially locks India into being a large and growing market for American industry, without a corresponding guarantee that Indian products will find expanded access to American shelves. We’ll also be importing more of our oil and gas needs from the US, a leading producer of the same. It will likely be more expensive, and analysts warn it could reverse the recent moderation in domestic retail inflation.

Some Indian exports did win favourable terms. Cut and polished diamonds, jewellery, silk products and aircraft parts all secured zero-duty access. These goods reflect genuine complementarity. The US doesn’t produce cut diamonds or generic drugs at scale, while aircraft parts feed directly into Boeing’s supply chain. These are sectors where tariffs would have hurt American industry as much as Indian exporters.

But for India’s most labour-intensive exports — textiles, apparel, leather, footwear, and so on — the tariff stays at 18%. These are sectors that employ tens of millions of workers and compete directly with Vietnam and China. An 18% wall is survivable, and relatively better than competitors. But it’s not an opening.

In essence, India has made what seem to be binding commitments, while the US has not.

America First

The deal makes more sense when viewed not merely as trade diplomacy, but as an extension of America’s own industrial policy.

Take the $500 billion purchase commitment, which is concentrated in sectors that have been prioritized the highest by the US government. For instance, the US has the CHIPS policy which attempts to revive its semiconductor industry and reduce dependence on China. Aerospace, meanwhile, is too strategic an industry for the US — after all, Boeing is part of a global duopoly . Even energy exports are shaped heavily through government policy.

The deal effectively expands the Indian market for American producers, underwritten by a bilateral trade commitment rather than competitive market dynamics.

At the same time, beyond India, the US is using tariffs to bolster the supply chains it has control over. Take the textile tariffs, for instance. The US maintains the USMCA — its free trade agreement with Mexico and Canada — with strict “rules of origin “ for garments. Under the USMCA, a shirt made in Mexico using North American yarn or fabric can enter the US duty-free. It forces brands to source from Mexican factories that use US yarn, effectively subsidising American farmers and nearshoring manufacturing in one move.

However, perhaps the US doesn’t view the USMCA as enough to protect American supply chains. So, a shirt made in India gets slapped with higher tariffs. This tariff differential protects the North American supply chain, even if it means kneecapping someone else. Indian textiles are hardly just competing against tariffs. They’re up against a deliberately-engineered production network.

But, all this comes at a short-term cost to the American consumer. As the Kiel Institute’s research shows, the 18% tariff functions as a consumption tax on Americans. But the Trump administration appears willing to accept that trade-off for now. The logic, whether it works or not, is to protect American supply chains, even if it means Americans pay more.

No other choice?

If the terms are this lopsided, why did India even sign?

The most straightforward answer is that a 50% tariff is catastrophic. At 18%, Indian goods are still competitive relative to China (~30%), Vietnam (20%).

But the deal did very little to expand India’s access to the US market . Tariffs went from the pre-Trump average of 2.4% to 18%, not from 50% to 18%. India simply regained access it had effectively lost, at a significantly higher price. In contrast, in the EU deal, Indian textiles won zero-duty access and the potential to create new jobs.

At the same time, how long our relative competitiveness in the US against other nations lasts is also unclear. For instance, Bangladesh, one of the largest textiles exporters in the world, has also signed an interim trade deal of their own with the US. This, in turn, has left Indian exporters concerned.

In such a situation, countries don’t really compete based on the competitiveness and quality of their products. They simply compete on how quickly they can agree to the terms of the US.

However, India did have some strategic calculations of its own in this deal. For instance, securing access to high-end GPUs and semiconductor components is, at this point, a national mandate. And those are primarily owned by American firms. India’s AI ambitions, its digital infrastructure buildout, and its data centre expansion all depend on these components. That’s why the deal facilitates trade in GPUs and data centre equipment.

Perhaps, this deal was constructed keeping the power dynamic in mind . It is very hard for India to replace demand from the richest market overnight. We also need advanced tech from the US to bolster our manufacturing. So, one could argue that, knowing this asymmetry will exist any which way, India chose certainty over confrontation.

But this interim deal will now be the baseline for a future trade agreement. We can’t say for sure what a final deal will look like, but the new asymmetries created by the interim trade deal will feed into further negotiations. In that, India will have no choice.

The art of the deal

For India, the immediate calculus behind this deal was damage control . Escaping a 50% tariff wall, securing technology access, and maintaining a competitive edge over peer countries were all rational objectives.

But the price of all this might, perhaps, be too heavy. We have effectively surrendered our autonomy in how we source energy, while also still accepting high tariffs on many labor-intensive sectors, and increasing our dependency on the US.

For the US, the deal is a template for more coercive economic statecraft. While most countries use tariffs to climb up the value chain, the US seems to be using them to push countries down the ladder.

Is this dynamic sustainable? As we’ve covered before, India’s recent flurry of signing trade deals is a hedge to ensure that no single partner — be it the US or China — can hold this kind of leverage again. The EU deal is part of that hedge.

But, for now, the leverage that the world’s richest consumer market holds is very real.

The many complexities of India’s corporate bonds market

Over the last few months, India has been thinking hard about reforming its market for corporate bonds.

In December last year, the NITI Aayog released a detailed report making a case for India to strengthen this market, along with a roadmap for how India could get there. Little more than a month later, the Economic Survey made a forceful case for the same cause, positioning corporate bonds as a critical pillar our economy still needed to build. Then, mere days later, the Finance Minister’s budget speech announced two concrete changes in this direction: a framework for corporate bond indices, and one for total return swaps. And within the week, the RBI followed up with draft directions to bring those announcements to life.

By the standards of Indian policymaking, this is a blistering pace. It signals that the government is treating this project not merely as an aspiration, but as a concrete agenda. There’s good reason for this urgency. We’re in a unique geopolitical moment. With Russia largely frozen out of global indices and China contending with deep structural problems, the world is actively searching for stable emerging markets to park their money in. This is a big opportunity for us to capitalise on.

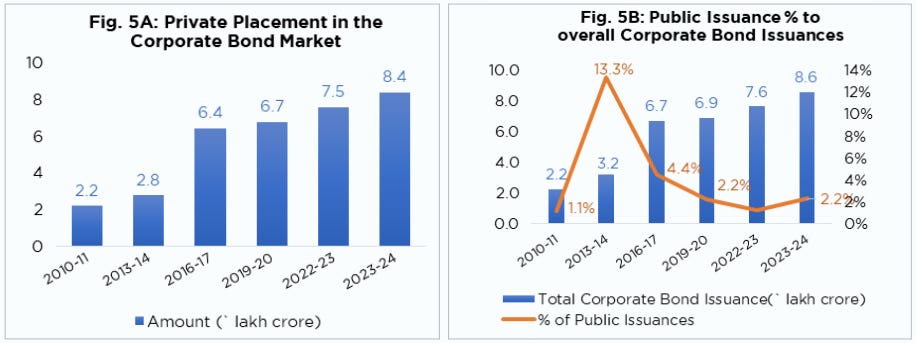

This isn’t the first time the government has tried. India has been trying to deepen its corporate bond markets for years — and to be fair, this has had a real impact. Outstanding corporate bond issuances have tripled from ₹17.5 trillion in FY2015 to an estimated ₹53.6 trillion by FY 2025. In the last five years, India’s commercial sector has expanded its non-bank financing at a CAGR of over 17%.

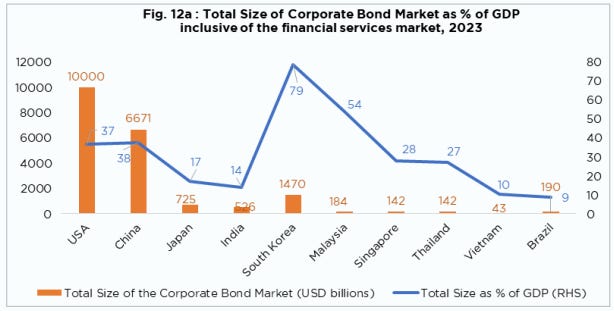

While this trajectory is reassuring, growth rates can deceive. India’s corporate bond market still accounts for only about 14–16% of our GDP. That’s low by global standards. For instance, in South Korea, corporate bonds amount to nearly 80% of GDP. In Malaysia, they come to 54%. The market has been growing, yes — but in absolute terms, it remains startlingly thin.

Where do we fall behind? For that, let’s begin with the first principles.

Businesses need bond markets

Let’s begin with why this reform project is so critical.

Businesses, simply put, need money to grow. According to the Economic Survey, access to finance is arguably the most binding constraint facing Indian businesses, and MSMEs in particular. But where does that money come from?

Imagine, for a moment, that you run a mid-sized Indian company that needs capital to expand. You have one realistic option: go to a bank . Issuing debt on the bond market is expensive, cumbersome, and — unless you happen to be among a very small club of highly-rated firms — has few customers.

So you go to the bank. But banks have a structural problem that puts a hold on their long-term lending. They fund themselves primarily with short-term deposits — which people can withdraw at relatively short notice. Meanwhile, if they lend over a long horizon, they get paid slowly, over many years. This creates a mismatch between the money they owe and the money they’re owed . That can create risks.

To compensate, banks do two things: one, they price in more risk, lending at higher rates. Two, they simply limit how much long-term credit they extend. India’s bank credit to the private sector stands at roughly 50% of GDP — modest next to China’s 194% or Vietnam’s 125%. Simply put, Indian banks alone can’t compensate for the lack of other funding sources.

In theory, a well-functioning corporate bond market should solve several problems at once. One, it pulls in entirely new pools of capital to finance Indian businesses: insurance companies, pension funds, mutual funds, and more. Two, a market enables price discovery . When multiple buyers compete for a bond, the market decides a “yield” that reflects genuine consensus about the issuer’s creditworthiness. The better a borrower is, the lower its borrowing costs could be. Three, bonds let investors tailor their investments to their own cash flow needs. Over time, this should compress the risk premium borrowers pay.

These are already meaningful benefits. And when you zoom out, the case for a deeper bond market is even more compelling.

An economy that channels most of its credit through banks is an economy with a single point of failure. Banks, by their nature, tend to face the same problems at the same time. They hold similar asset classes, respond to the same monetary policy signals, and are governed by the same capital adequacy rules. When conditions tighten, they tend to pull back collectively . Credit dries up across the board. At such times, even solvent, healthy firms are unable to access loans.

A functioning bond market, as the legendary economist Alan Greenspan called them, is a spare tire for the economy. Even if banks pull back, bond investors continue to provide financing. They also, incidentally, make monetary policy work better. When the RBI adjusts rates, corporate bonds are repriced almost immediately. Bank lending, in contrast, takes a long time to reflect those new rates.

None of this is controversial. Everyone agrees, in principle, that India needs a deeper corporate bond market. Creating one, though, is easier said than done.

Where the market breaks down

India’s corporate bond market isn’t held back for any one reason. It’s trapped in a web of reinforcing problems, each of which makes the others harder to solve. Here’s a sampling of some of the biggest ones, though this isn’t an exhaustive list.

Getting in is too hard

Issuing a bond to the public, in India, means navigating an obstacle course of overlapping regulators.

Depending on the specifics of the issuance — who’s issuing, who’s buying, what form the security takes — the same transaction may fall under the purview of SEBI, the RBI, IRDAI, or the Ministry of Corporate Affairs. Each regulator brings its own disclosure requirements, its own timelines, and other compliances.

Combined with advertising and legal fees, this friction makes it much more expensive to issue publicly tradable bonds. It’s easier to go to a bank or an NBFC. If you do issue bonds, you’re much more likely to go for an off-market private placement.

This challenge would be easier to solve if the public markets offered materially cheaper funding or longer tenors. But that isn’t the case either.

The biggest buyers are absent

If there was a lot of demand for publicly traded bonds, the markets would be more attractive. It would offer lower interest rates and more attractive terms — which may have been worth the added hassle. But structurally, the buyers who should anchor such a market are largely absent .

Think about who needs bonds the most. To buy a bond is to buy a fixed, predictable cash flows stretching for years. Anyone that has already committed to making payments far into the future — insurance companies, pension funds, provident funds — are natural buyers for such a product. Bonds can give them reliable income streams far into the future.

In India, however, the buying power of these institutions is heavily constrained.

Insurance companies, for instance, are legally barred from investing in anything rated below AA . While the EPFO — which manages over ₹25 trillion in retirement savings — can legally invest below that grade, in theory, its accounting practices just don’t allow for it. It doesn’t mark its portfolio to the market, which means it only recognises losses all at once, in the case of an actual default. Rationally, then, it follows a “zero-loss” culture that shuns even marginal risk.

And so, India’s richest entities — those who would naturally love the high, fixed interest that a bond with medium risk can give them — sit most of the market out. They invest solely in the debt a handful of pedigreed issuers, which are usually either finance companies or government-backed PSUs. This creates a missing “middle-market”. India’s manufacturers and infrastructure builders — those who need financing the most — are cut off.

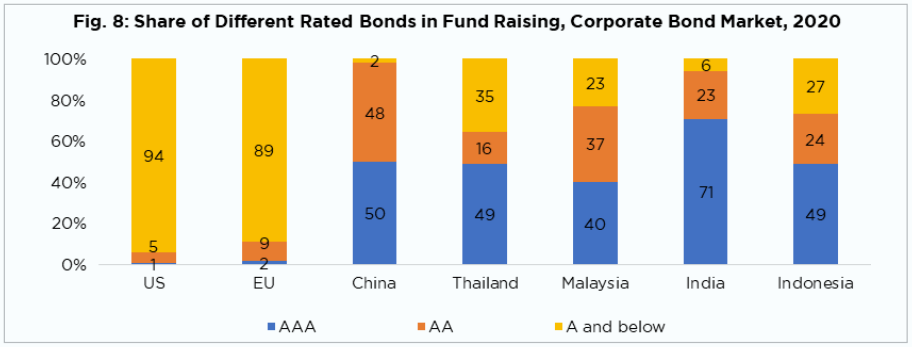

Consider this: in FY 2023, 94% of India’s corporate bond issuances were rated AAA or AA. Everything else, together, accounted for just 6% of fundraising. This is almost an inversion of mature markets: in the US and EU, top-tier AAA issuances make up only 1–2% of total volume, with the vast majority of the market serving A-rated and lower issuers.

When a company’s rating slips even one notch below AA, it effectively loses its entire institutional investor base overnight. This steep cliff discourages new issuances, and concentrates the market at the very top.

The government crowds everyone out

There’s another reason there’s such little demand for India’s corporate debt: there’s simply too much safe debt to buy.

As we detailed in our budget special, India runs a large fiscal deficit — which means we issue sovereign debt at scale. That state-backed debt competes with companies for the same pool of domestic savings. And more often than not, it’s more attractive than the alternative. Our government’s level of borrowing pushes up yields on government debt. Since most corporations aren’t as safe , they must offer even better yields to attract investors.

Additionally, most major financial institutions are obligated to invest in this debt. Life insurers, for instance, must invest at least 50% of their corpus in government securities. Banks, too, have similar mandates for much of their capital.

Other countries have pulled themselves out of this bind. In South Africa, for instance, for many decades, pension funds and insurers had to invest up to 53% of assets in public sector debt. Their corporate bond markets, predictably, were moribund. When those mandates were repealed in the late 1980s, its corporate bond market became much more liquid.

There isn’t really a market after issuance

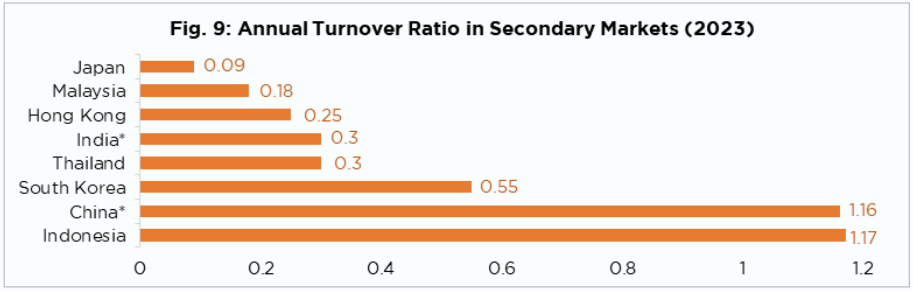

With such little demand for corporate debt, our bond markets are barely markets at all. Once you buy a bond, there’s practically nowhere to sell it. Most investors simply hold their bonds to maturity. To be fair, bonds are never the hottest traded securities on any market. But India’s secondary market for corporate bonds is exceptionally shallow. The annual turnover ratio for Indian bonds sits at 0.3 , compared to 1.17 in Indonesia or 1.16 in China.

Without a secondary market, investors need a premium to hold on — which acts as a direct tax on every issuer.

This is partly a problem of infrastructure . India’s corporate bond market lacks a market-making ecosystem. There are no intermediaries that can constantly quote two-way prices. And so, any seller needs to find a bona fide buyer for a trade to go through. There would be more market-makers, perhaps, if India had a corporate bond repo market or facility, like there is for sovereign debt. These would allow a market maker to borrow cash against their existing bond holdings to fund new purchases. Without a way to monetise inventory cheaply, market-making is an unrewarding business.

Neither does India have an active derivatives market , that would allow investors to customise their risk. We’ll come to that in the next edition.

All of these leaves little incentive for anyone to go through the pain of a public issuance. As a result, 98% of capital raised through corporate bonds in FY 2024 came via private placements, which are negotiated bilaterally, and are invisible to the broader market. Public issuances, which accounted for 13% of the market a decade ago, have shrunk to just 2%.

The feedback loop

None of these challenges exist in isolation; they all feed each other. This is a market with major supply bottlenecks, limited demand , and major frictions in matching supply with demand. And that creates an additional chicken-and-egg problem. Thin liquidity discourages issuers, which narrows the market, which further reduces liquidity.

For problems so wicked, one-shot solutions simply don’t exist.

With this background, in the next piece, we’ll look at what the RBI’s recent changes actually do. We’ll explore which knots they begin to untie, and which ones remain firmly in place.

Tidbits

- The National Highways Authority of India has accepted a ₹9,500 crore bid from Road Infra Investment Trust (RIIT), backed by the National Investment and Infrastructure Fund (NIIF), to monetise five highway stretches under the toll-operate-transfer (TOT) model. This is one of the largest TOT deals so far.

Source: PSU Watch - The Gujarat government has signed a letter of intent with Elon Musk’s Starlink to bring satellite-based internet connectivity to the state, making it one of the first Indian states to formally engage with the company. The move comes as Starlink awaits regulatory approvals to launch commercial operations in India, where it will compete with Jio’s satellite broadband plans.

Source: TOI - The RBI is now allowing banks to extend collateral-free loans of up to ₹25 lakh to micro and small enterprises with a good track record, up from the earlier limit of ₹10 lakh. The enhanced guarantee coverage is aimed at improving credit access for smaller businesses that often struggle to offer security against loans.

Source: ThePrint

- This edition of the newsletter was written by Manie and Pranav

Tired of trying to predict the next miracle? Just track the market cheaply instead.

It isn’t our style to use this newsletter to sell you on something, but we’re going to make an exception; this just makes sense.

Many people ask us how to start their investment journey. Perhaps the easiest, most sensible way of doing so is to invest in low-cost index mutual funds. These aren’t meant to perform magic, but that’s the point. They just follow the market’s trajectory as cheaply and cleanly as possible. You get to partake in the market’s growth without paying through your nose in fees. That’s as good a deal as you’ll get.

Curious? Head on over to Coin by Zerodha to start investing. And if you don’t know where to put your money, we’re making it easy with simple-to-understand index funds from our own AMC.

Thank you for reading. Do share this with your friends and make them as smart as you are ![]()