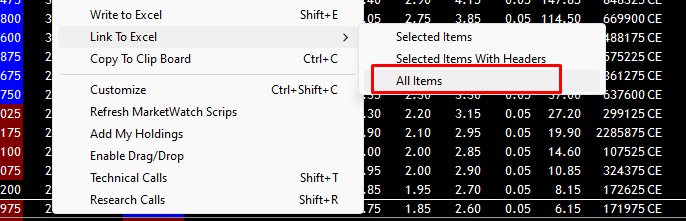

currently, I am using sasonline alphatrader which is exactly the once “pi” of zerodha.

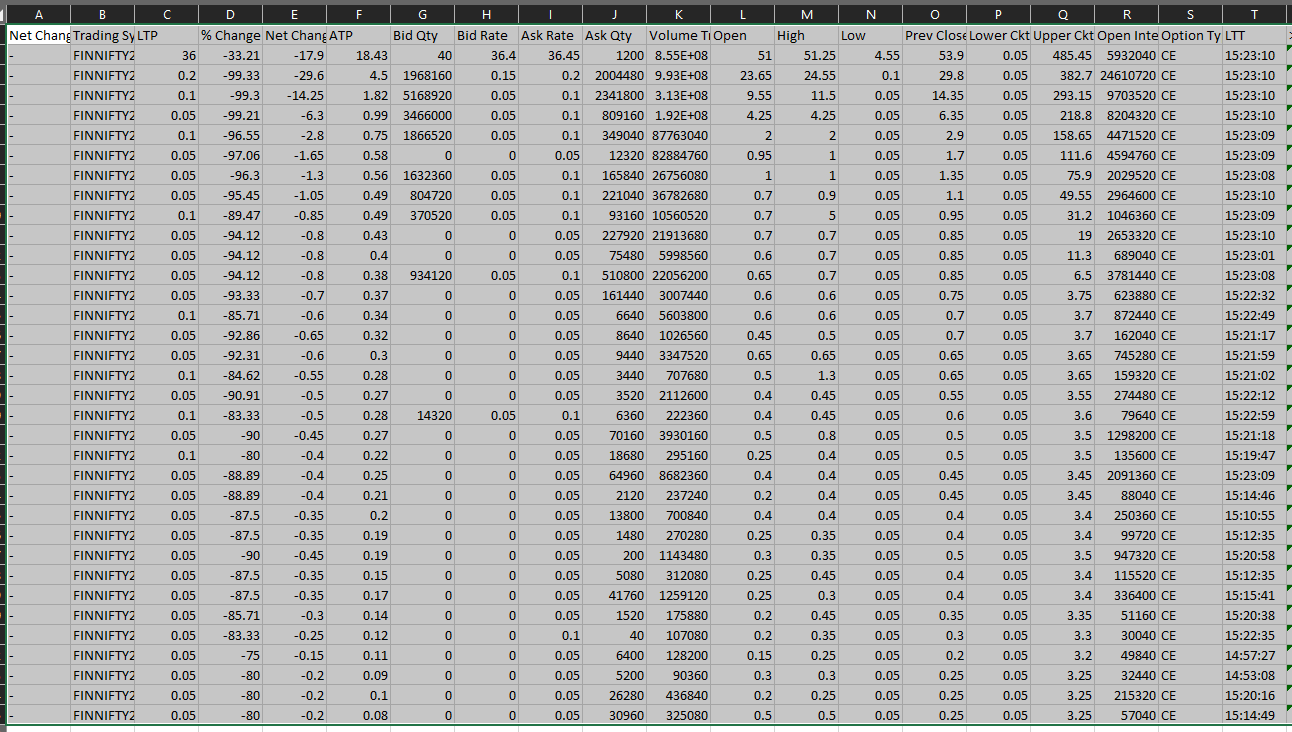

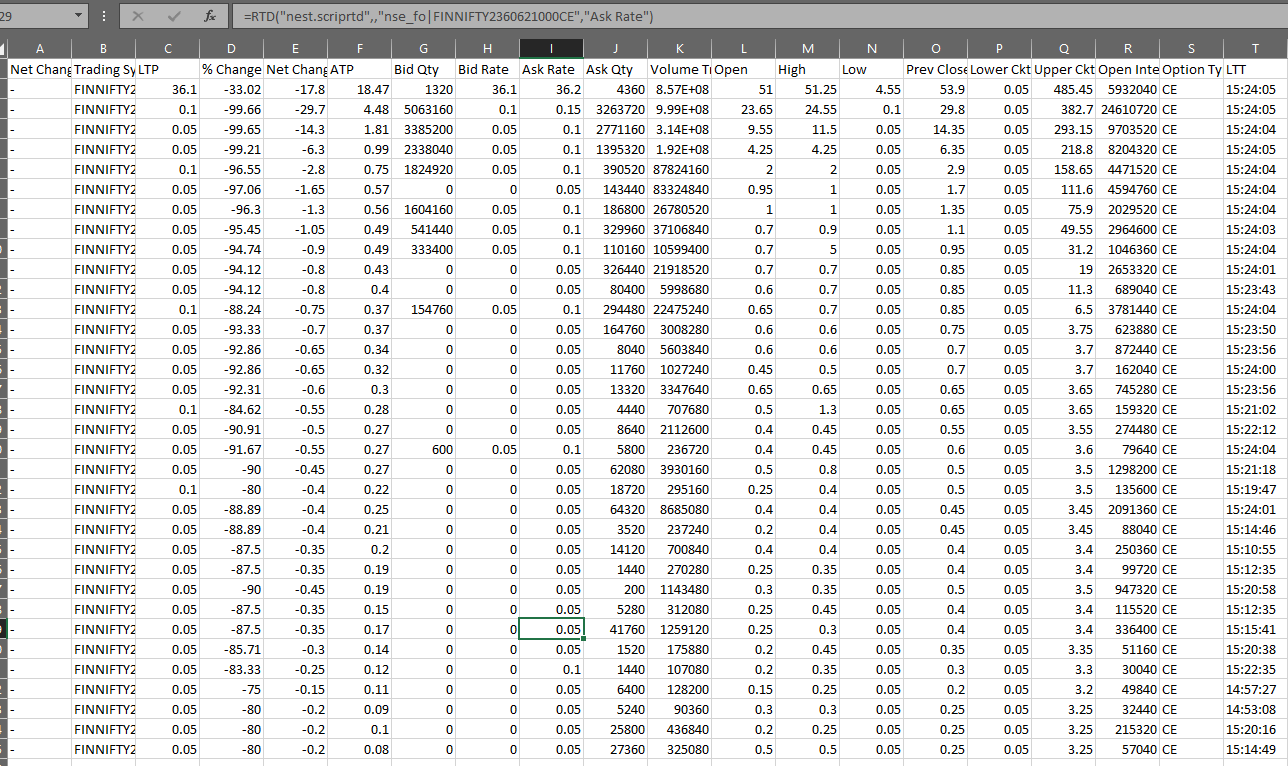

My strategy relies much on finding the current open as compared to a particular high/low value. This is pretty much easy with excel soon after premarket is over, at around 9:08. I have in my hand the scripts I need to work for the day.

Alphatrader feeds are instant and rarely stops feeding to excel. I tried fyersone excel link, which stops live feeding to excel most times.

The problem with alphatrader is that SASONLINE laid out a rule that one needs to have minimum 10k in trading accounts to access their products. Well, I don’t trade with sasonline. I use their platform but they already charge maintenance for it. I am just not glad with the 10k min balance like in banks.

So, anyone who can kindly help me with platforms that can link to excel?

Hi,

i was looking to find open price calculations.

i saw sensibull option chain calculator, but the thing is nse IV & other tools IV is not matching with Sensibull.

can u message or post here as how ur figuring open price around 9:08 ? how much is ur accuracy % ?

OP is most likely referring to Cash mkt(Equities) Open price which is a fixed value after order matching (Equilibrium price).

What you seem to be looking for is to derive Options pricing at mkt open (9:15 am). probable open.

You cannot determine the exact price(100% consistently bcos of mkt forces), but knowing the latest value of Spot after pre-open, you can approximate.

Even then Futures premium varies through out so accuracy cannot be really determined.

Instead if you just used the delta of your strike plus prev day premium added to pre-open spot, you’d really be as close as can be.

There is no limit to the complexity you can add with changing IVs that affect greeks. Few times decay occurs earlier at open, few times max near mkt close etc. some times there is spike in first 5-10min, other times not (its

all dynamic)

Thanks chirag for the reply.

Yes i am looking for deriving the OP for options CE, PE pricing & how much it can spike within few seconds of market opening (9:15).

I calculated values through delta, but it’s not coming closer because IV plays the role. Now the confusion with IV is nse data & other OI tools have different IV’s not same : who got the best accuracy not sure ? as u said its dynamic, that’s true , but m trying to find the probability range which occurs most of the time.

what all greeks (IV, delta, vega?) should be taken care mostly while determining open price & initial high, low which might occur in first minutes.

Also pre-market order & after market orders play a crucial role in FnO options : what i observed is if i had placed sell order of my overnight positions before 9am : chances of executing at a higher price (if prediction goes right) is more than placing an order between 9 to 9:08 am or let’s say i placed a limit target order at 9:14am. while this article speaks something else : What are pre-market and post-market sessions and orders in NSE and BSE?

I observed few times that if i had place a target order at 9:14 at higher price, chances of executing it becomes low even though it reached that high price in initial seconds : maybe because of that FIFO - priority basis.

i didnt want to stir up a hornet’s nest but those IV tools and NSE are very dinosaur.

IMO, Sensibull with the Black 76 model is better. The concept of single IV at a strike vs NSE different IV for CE/PE has too many flaws. I dont know if they’ve shared the formula to derive same values publicly.

that 10% interest rate is too vague, mkt even prices STT/cost etc, on expiry day options trade close to 30-min weighted closing and there is no simple way to do all this.

Best greek derivation is from Futures price not spot, and in pre-open even the Futures price is not known so its a dark alley. You might have observed in sensibull, for weekly expiry, the effective Futures rate would be something discounted to the Monthly traded one. All very complex stuff to wrap the head around it.

Again, im assuming, but Sensibull derives IV(greeks) from price you see ( as in they dont derive price ), so its mkt forces that eventually make the spread/trade.

Anyway, i dont need that accurate pricing so i dont indulge. I just let pricing stabilize or go with an approximation as written earlier. More often than not, order punched within few seconds of mkt open stays in “pending validation” and it sucks.

thanks for all the helpful responses. Apologies, I couldn’t jst commit to my own post. So, here I am days later, opening up my query.

I am just looking for a software that could link a custom list of stocks. Currently, alphatrader of SASonline has these feature. @viswaram thank you very much.