Goldman Sachs recently shared a report titled “The Rise of Affluent India” - Affluent here refers to that group of the population who have a decent amount of money - here the number has been defined as someone who has income above 10000$ (Over Rs. 830000 per annum)

The report has generated a lot of buzz on social media esp. Twitter as it extrapolated lots of interesting data points and charts about the theme. Here are some of the highlights:

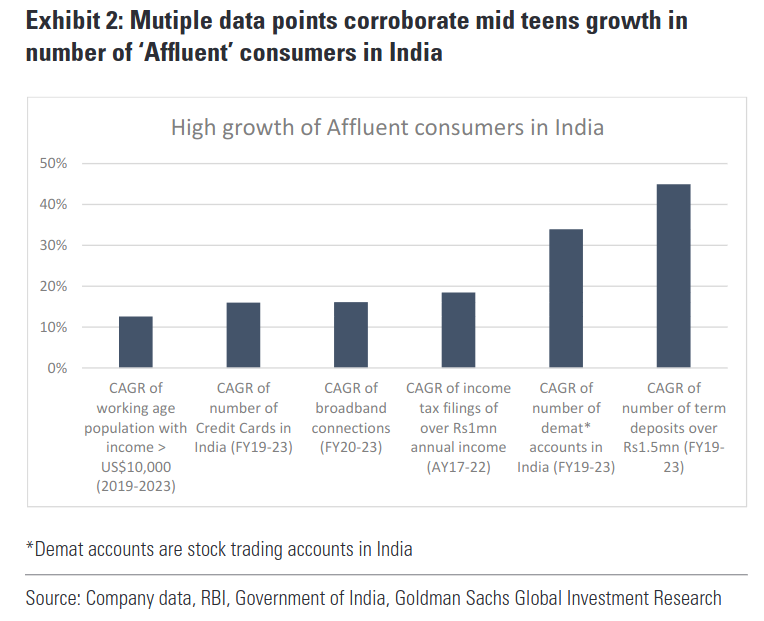

The rapidly growing cohort of ‘affluent’ consumers in India

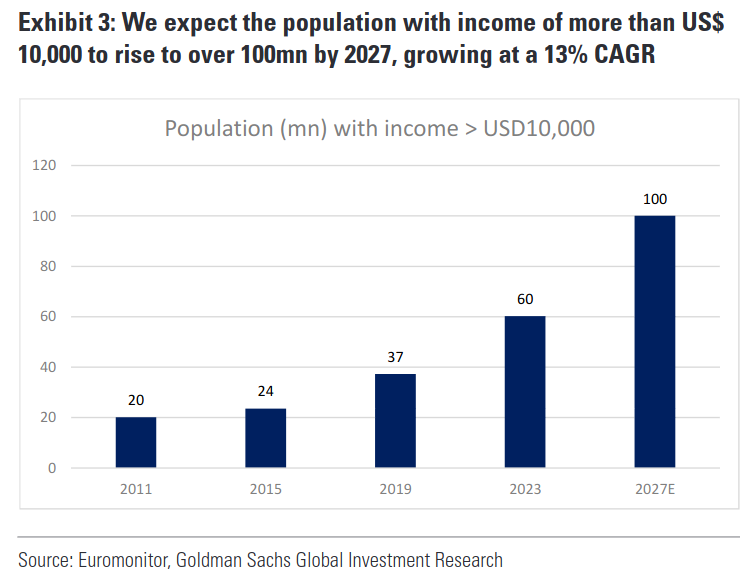

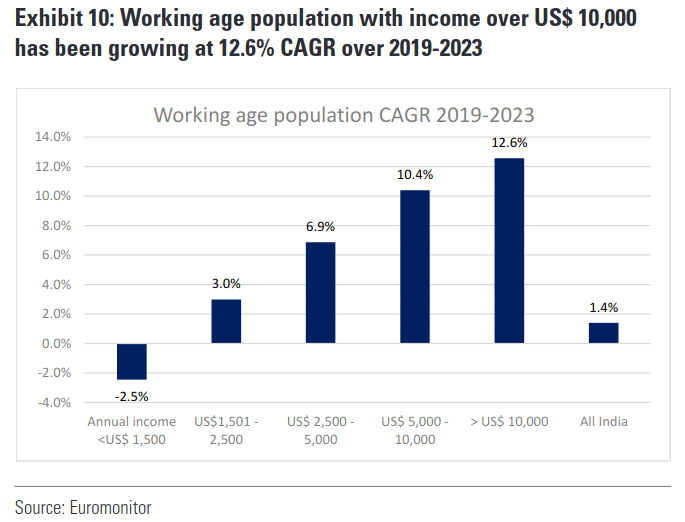

- Compared to India’s average per capita income of ~US$2,100 ( 174000 in INR terms) , The top 4% of the working-age population in India has a per capita income greater than ~US$10,000 (830000 in INR terms) per annum. Referring to this top-income consumer cohort as ‘Affluent India’, ‘Affluent India’ comprises nearly 4.4 crore of the working-age population in 2023.

Corroborating data across tax filings, bank deposits, credit cards, and broadband connections, GS estimates that this consumer cohort has grown at a 2019-23 CAGR of over 12%, compared to ~1% CAGR of India’s population. If the current trajectory continues, we expect ‘Affluent India’ will grow to ~100 million consumers by 2027.

Stronger wealth effect in the past few years:

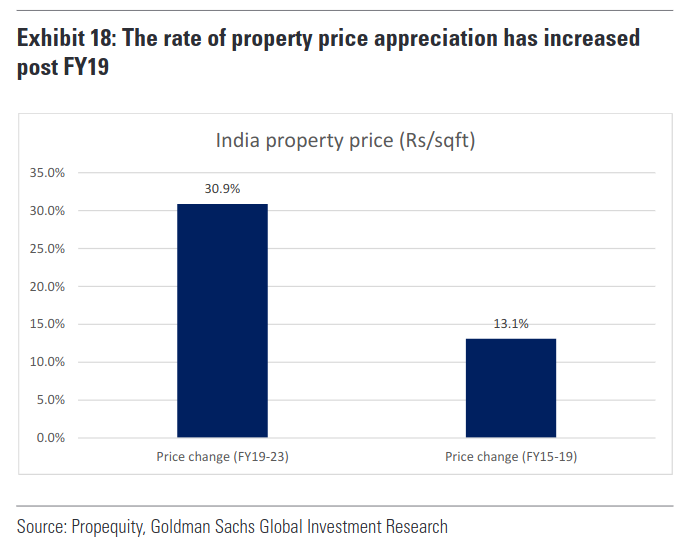

Property prices have seen a change in trajectory

While property prices have not risen as sharply as gold and equities, there has clearly been a change in the pace of increase in property prices in India in the past few years.

The average property prices in India have risen ~30% over FY19-23, compared to a much slower increase of ~13% over FY15-19, according to Propequity data.

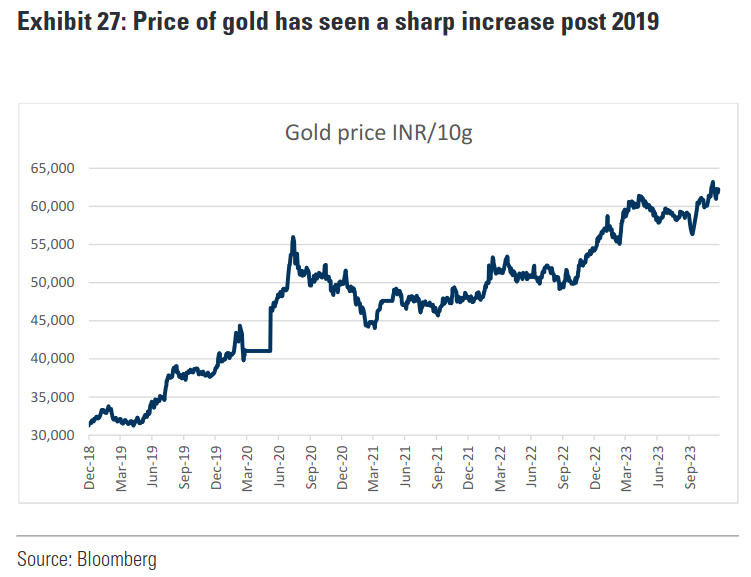

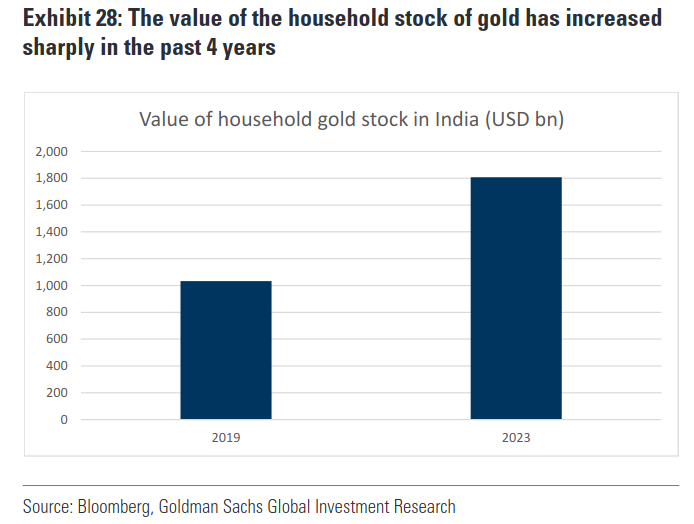

Indian households own ~10% of global physical gold, which has appreciated sharply over FY20-23

Indian households own ~10% of global physical gold, which has appreciated sharply over FY20-23 Indian households hold ~25,000 tons of gold representing ~10-11% of the world’s physical gold stock, as per the World Gold Council. The price of gold has increased from an average of Rs39,900/10gm in January 2020 to an average of Rs62,200/10gm in December 2023, a ~65% increase. The value of the total stock of household gold in India has increased from US$1.1tn to US$1.8tn over 2019 to 2023. This sharp increase would be a key component of the rising wealth effect on ‘Affluent India’.

While a significant amount of gold is held as jewelry in households, it is still seen as a store of value and this contributes to the wealth effect.

Equities - rising value of holdings and increasing participation in the market

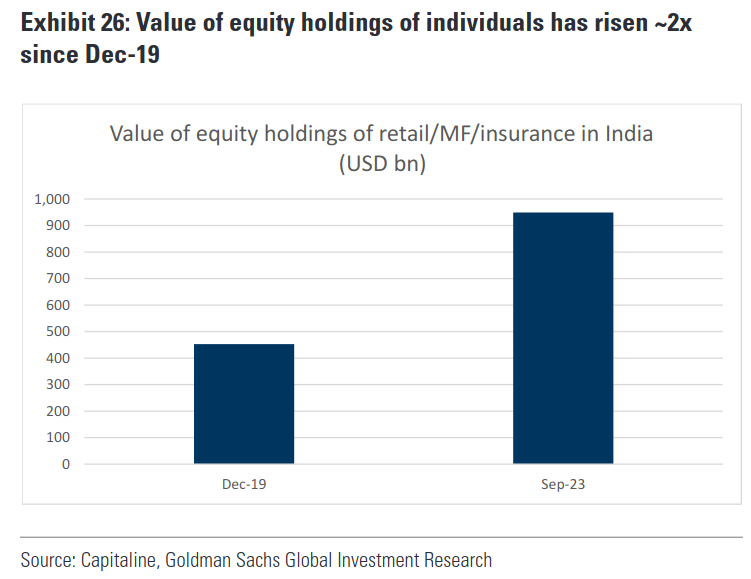

The market cap of the Indian stock market has risen by 80% from 1st January 2020 (just before the COVID disruption led market fall) to 1st January 2024. In the same period, we have also seen the participation of retail investors rising in the Indian equity market.

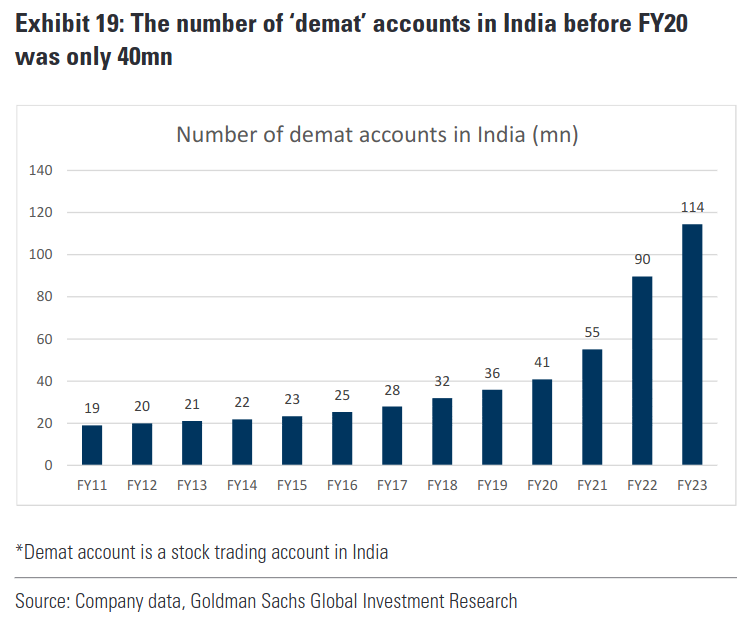

Growth in demat accounts

The number of ‘demat accounts’ (electronic accounts to trade shares in the stock market) has increased from ~4.1 crore in FY20 to ~11.4 crore in FY23.

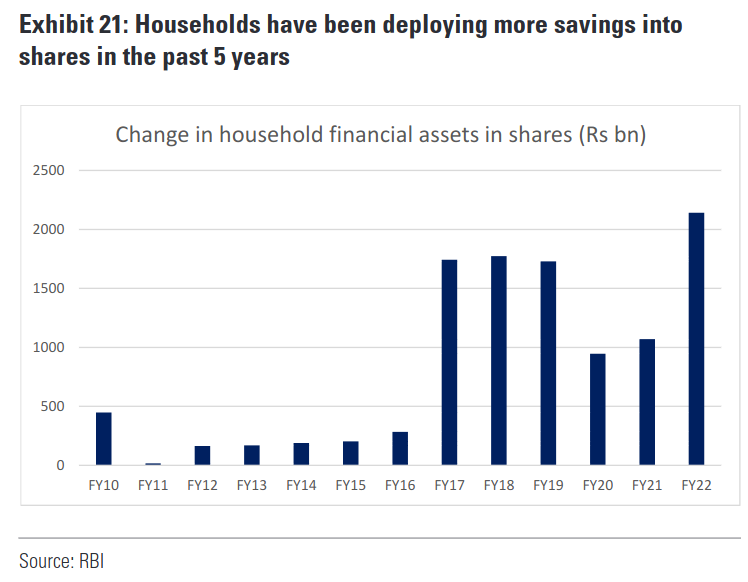

Also, the net flow of household savings into shares has seen a large increase since FY17 and has been consistently high over FY17-23, which could imply continued rising participation in the equity markets, in a period of strong market returns.

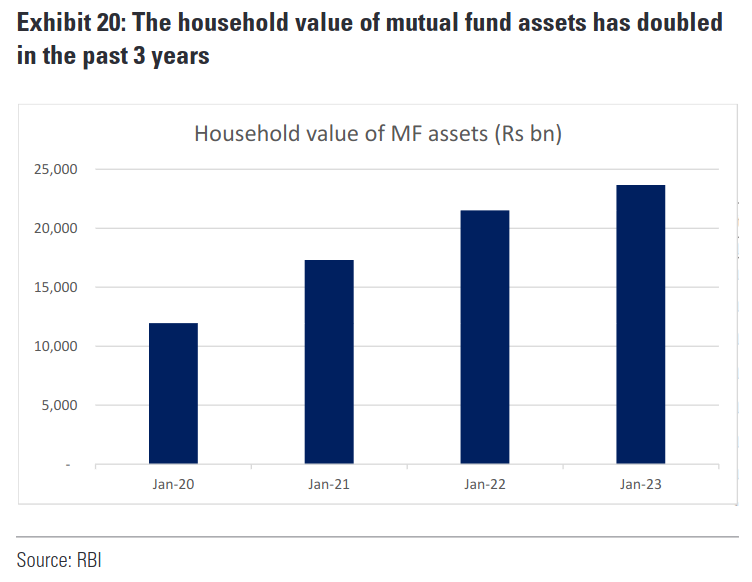

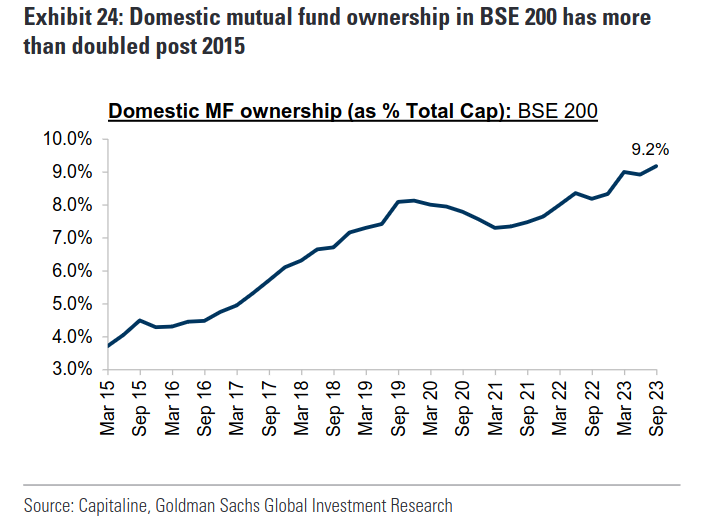

The ownership of equities by consumers is held through direct retail shareholding and through mutual funds.

Both of these have seen an increase in the past few years. The total ownership of BSE 200 by direct retail investors has increased from 8.5% in Dec-19 to 9.8% in Sep-23, while the ownership of domestic mutual funds has increased from 8.1% in Dec-19 to 9.2% in Sep-23.

Top end consumption growing much faster than broad based consumption

In the past 3 years, As per GS, there has been a large divergence in the growth rates of consumer companies and categories in India. One of the key factors driving this is that companies that address consumption from the top end of India’s income pyramid have grown much faster compared to companies in the same category that address broad-based consumption in India.

Premium players within the same category growing faster:

In most industries, companies that address relatively more affluent consumers have been growing faster than companies that address broad-based or mass consumption. These trends are visible in FMCG (Nestle India growing faster than Hindustan Unilever), footwear (Metro growing faster than Bata), fashion (Trent growing faster than V-Mart), passenger vehicles (SUVs growing faster than entry level cars) and 2-wheelers (Eicher growing faster than the industry).

Within companies, premium segments have grown faster:

Within the same company, one can see a sharp divergence in the premium portfolio and the mass

portfolio. HUL’s premium portfolio has grown 2x that of the company’s overall revenue growth. For United Spirits, the ‘Prestige & above’ segment brands have grown much faster than the ‘popular’ segment brands. These trends are in concurrence with the data showing the much faster growth of Affluent India, which is likely to

continue going forward.

Companies exclusively addressing premium consumers growing rapidly:

Companies in categories that largely address top income consumption like jewellery (Titan), travel (Makemytrip, Indian Hotels), premium retail (Phoenix Mills), premium online beauty (Nykaa) and premium healthcare (Apollo Hospitals) have seen strong growth.

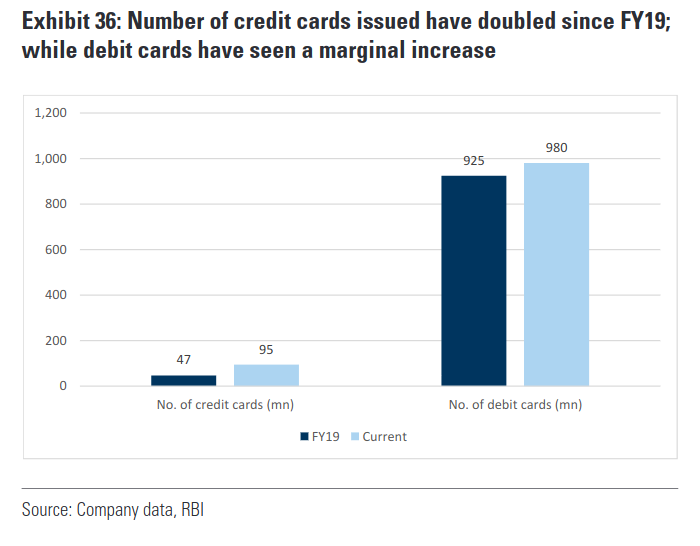

Credit Card spending has increased 2.5x since FY19:

Credit cards tend to be largely used by upper-income consumers. There are slightly more than 9 crore credit

cards in India (having grown from slightly below 5 crore in FY19). Many consumers have more than one credit card. Thus, most credit cards are likely to be owned by GS’s definition of ‘Affluent India’, which compares to ~6 crore consumers. The total spend on credit cards has increased 2.5x if we take the trailing 12 months vs FY19.