The IMF released its famous World Economic Outlook report on the global economic development in the near and medium term future. Here are a few highlights from the report and what it means to the markets.

Introduction

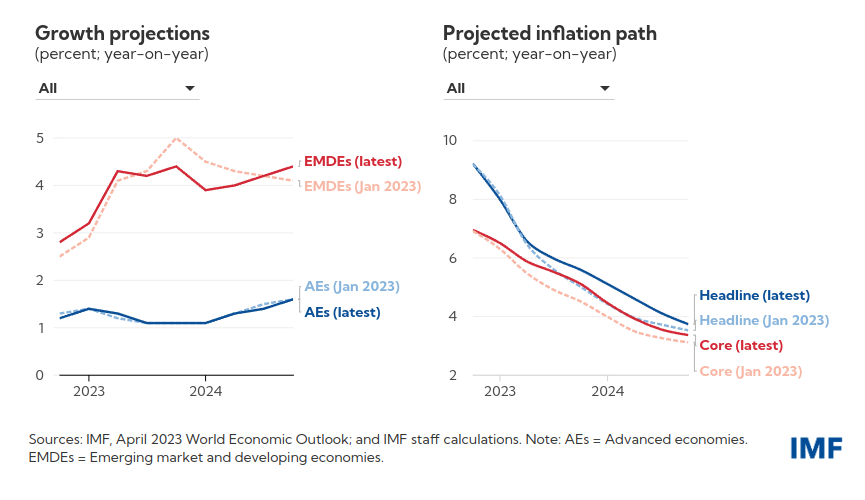

Global inflation will fall from 8.7% in 2022 to 7 % this year and 4.9 % in 2024. Some of the key pointers:

- The economic recovery from the shock of a war in Ukraine and the pandemic has been strong.

- China’s economy makes a solid comeback post the reopening.

- Supply chain looks secure in the global order, while food shortages and energy dislocations are waning.

- The result of strict tightening of the monetary policies by central banks should push inflation back towards the targets.

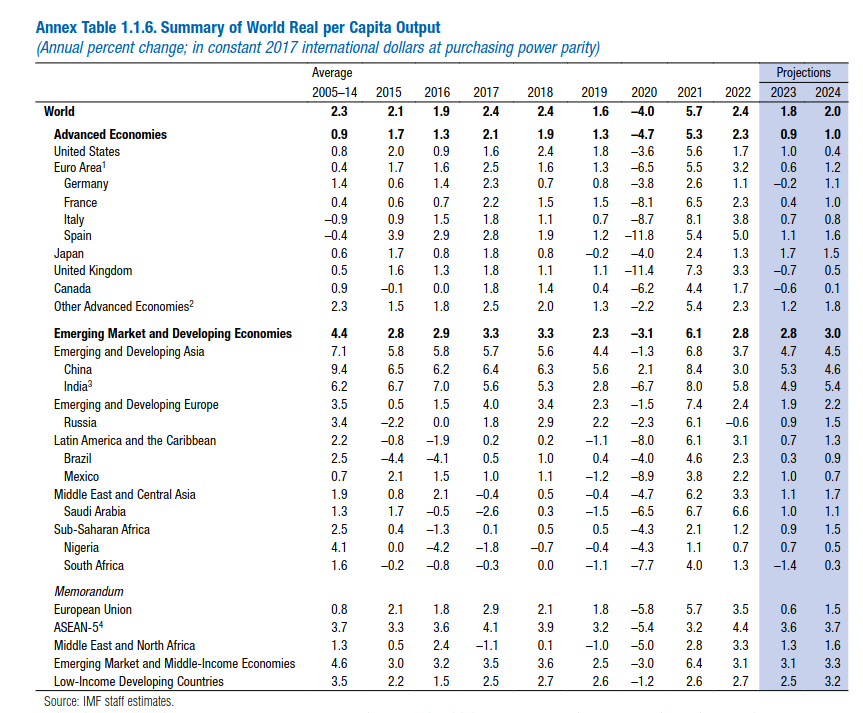

Growth and inflation

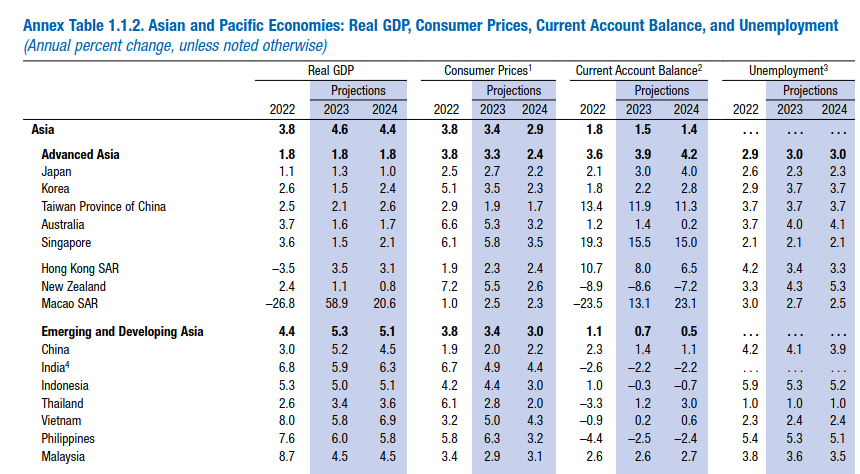

The economic deceleration is more evident in Advanced economies (AEs) as opposed to the Emerging market and developing economies (EMDEs). The fall of inflation hasn’t been as fast enough as estimated before.

The slump in AEs like the Eurozone and the UK is worrying where growth is expected to fall to 0.8% and -0.3% this year before rebounding to 1.4% and 1% respectively. The only silver lining is activity shows signs of resilience as labor markets remain very strong in most AEs.

What this means…

We could anticipate seeing more indications of output and employment softening at this stage in the tightening cycle. However, the IMF report’s estimates have been revised upwards for the last two quarters, suggesting better-than-predicted aggregate demand. In total, the monetary policies could be further tightened or stay tighter for longer than currently predicted.

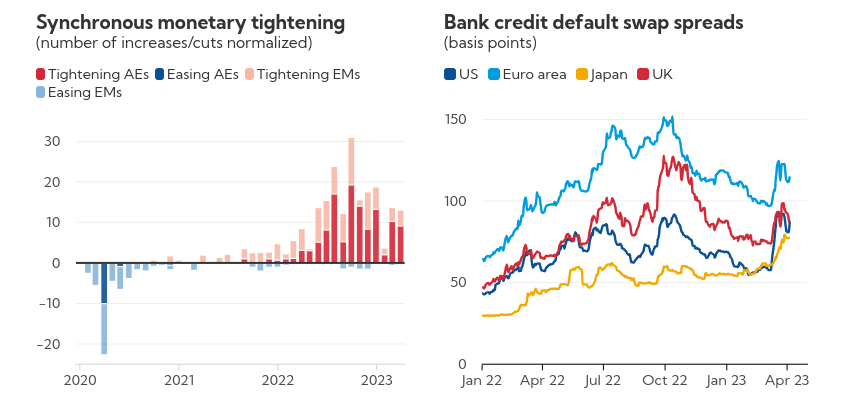

Now that the monetary policies have been tightened sharply over the last year, there have been some aftereffects; this triggered substantial losses on long-term fixed-income assets and raised funding costs.

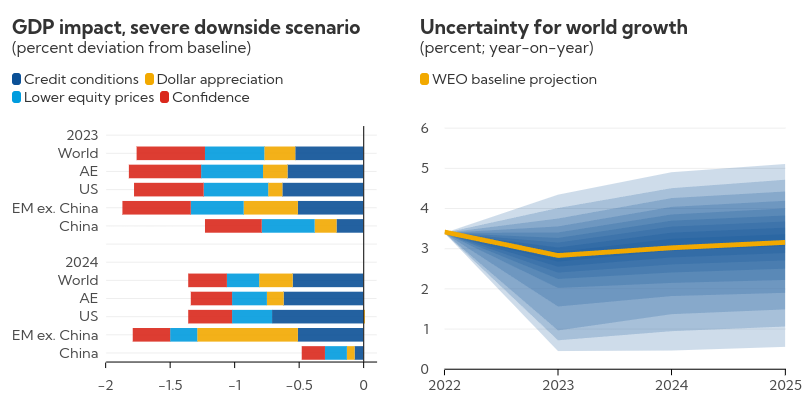

A sharp tightening of global financial conditions—a ‘risk-off’ event—could have a noticeable impact on credit conditions and public finances, especially in EMDEs. What happens then?

Large Capital Outflow >> Sudden increase in risk premiums >> Dollar appreciation >> Decline in global activity >> Decline in spending and investment

If this becomes a reality, then the IMF predicts that the global growth rate could slow to 1% this year. The chances of this scenario materializing is said to be 15%.

Note on policies

“With financial instability contained, monetary policy should remain focused on bringing inflation down, but stand ready to quickly adjust to financial developments.”

Walking on a thin wire, financial regulators ought to beware of the remaining financial hiccups ballooning into full-fledged crises by strengthening oversight and actively managing market strains. What this means for economies like India is ensuring access to the Global Financial Safety Net.

In line with its Integrated Policy Framework, the IMF suggests exchange rates should be allowed to adjust as much as possible unless it brims to financial stability risks or threatens price stability.

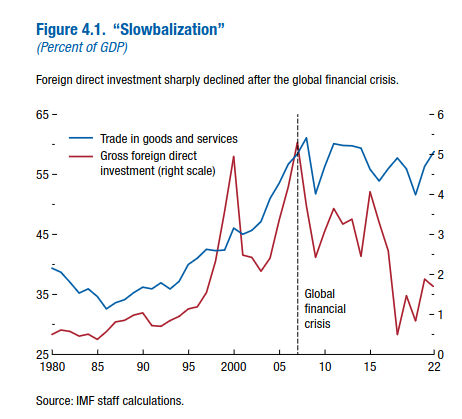

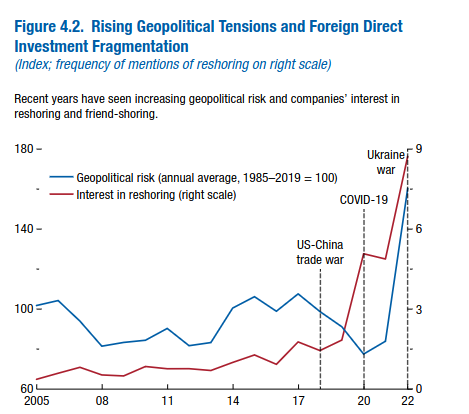

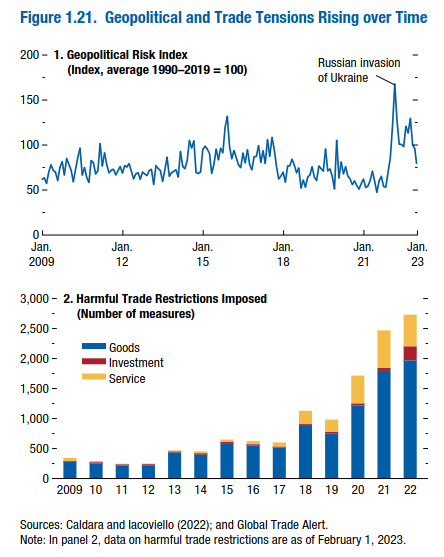

Slowbalization

Rising geopolitical tensions and the uneven distribution of the gains from globalization have contributed to increasing skepticism toward multilateralism and to the growing appeal of inward-looking policies.

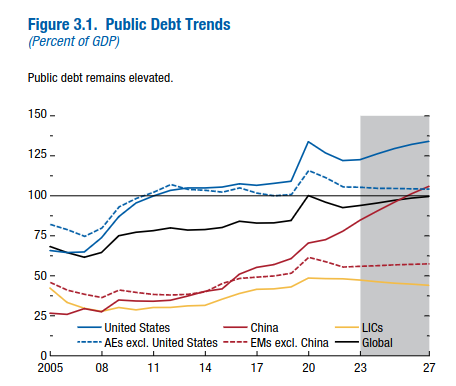

Public debt levels have soared through the roof as a result of the pandemic and economic upheaval over the past 3 years.

Monetary policy tightening has led to sharp increases in borrowing costs, raising concerns about the sustainability of some economies’ debts.

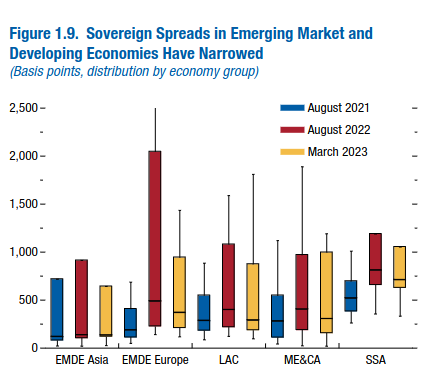

Among the EMDEs, the average level and distribution of sovereign spreads increased strikingly in the summer of 2022, before coming down in early 2023. The effects of the latest financial market turmoil on EMDE sovereign spreads have been limited so far but there is a tangible risk of a surprise increase in the coming months should global financial conditions tighten further.

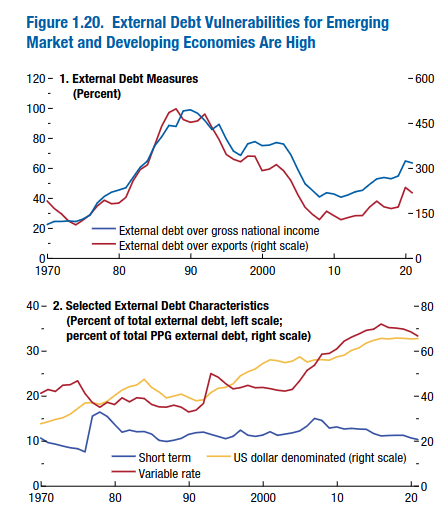

About 56% of low-income developing countries are estimated to be either already in debt distress or at high risk of it. About 25% of emerging market economies are also estimated to be at high risk. A higher share of external debt is now issued at variable interest rates and in US dollars, implying greater exposure to monetary tightening in AEs.

The war in Ukraine has reinforced this trend by raising geopolitical tensions and splitting the world economy into geopolitical blocs. Barriers to trade are steadily increasing. They range from the imposition of export bans on food and fertilizers in response to the commodity price spike following Russia’s invasion of Ukraine to restrictions on trade in microchips and semiconductors and on green investment that are aimed at preventing the transfer of technology and include local-content requirements.

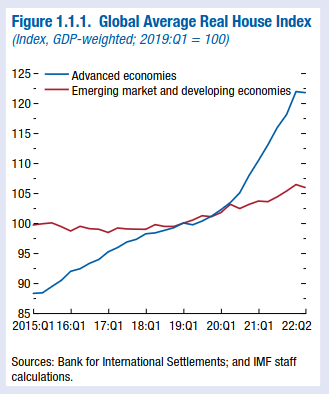

Housing markets and prices are likely to cool more and be more sensitive to policy rate hikes in economies in which house prices rose more during the pandemic.

Economies with high levels of household debt and a large share of debt issued at floating rates are more exposed to higher mortgage payments, with a greater risk of experiencing a wave of defaults.

In economies in which house prices increased rapidly and affordability declined, but household debt levels remained moderate up to the recent onset of monetary tightening, a more gradual price decline is expected, which could improve affordability.

Public debt as a ratio to GDP (“debt ratios” henceforth) has soared across the world during

COVID-19. In 2020, the global average of this ratio approached 100%, and it is expected to remain above pre-pandemic levels for about half of the world. The recent rise in sovereign debt holdings of domestic financial institutions, particularly in emerging markets, has further exacerbated the costs of high public debt, including by limiting the resources available for domestic institutions to lend to the private sector and by aggravating the risk of adverse sovereign-bank feedback Loops.

Closing pointers

-

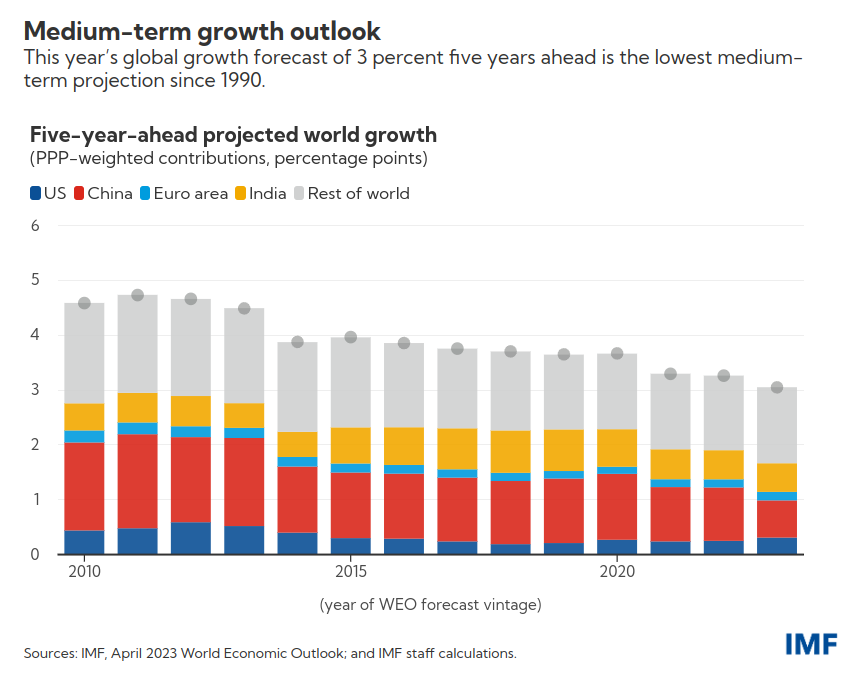

5-year ahead growth projections declined steadily from 4.6 % in 2011 to 3 % in 2023.

-

Rapidly growing economies like China and Korea also face the heat this time around with growth slowdowns.

-

Global growth will bottom out at 2.8% this year before rising modestly to 3.0 % in 2024. Global inflation will decrease, although more slowly than initially anticipated, from 8.7 % in 2022 to 7.0% this year and 4.9% in 2024.

-

Financial institutions with excess leverage, credit risk or interest rate exposure, too much dependence on short-term funding, or located in jurisdictions with limited fiscal space could become the next target.

You can refer to the full report here.