The RBI just published the October 2022 bulletin. We read it so that you don’t have to. Here are a few highlights:

Statement by Governor Shaktikanta Das:

Policy actions driven by domestic considerations in advanced economies will have global spillovers, such as tightening financial conditions, and volatility in financial markets due to the integrated nature of the global financial system.

Economic activity in India remains stable. While real

GDP growth in Q1:2022-23 was low, the late recovery in kharif sowing, comfortable reservoir levels, improved capacity utilization, rising bank credit & government expenditure are supportive of aggregate demand and output.

Inflation remains high due to large supply shocks, domestic demand, and global financial

market volatility.

The recent fall in commodity prices including crude oil may ease inflation.

The inflation trajectory remains uncertain due geopolitical tensions and nervous markets.

High-frequency data for Q2 indicate that economic activity remains resilient.

Private consumption, urban demand, ad rural demand are recovering. The festival season after 2 years of COVID will add to the recovery.

Investment demand is picking up and can be seen in the

growth of domestic production and import of

capital goods in July and August.

Credit to the commercial sector rose to `9.3 lakh crore in this FY from 1.7 lakh crore last FY.

Seasonally adjusted capacity utilisation of the manufacturing sector improved from 73.0% in Q4 to 74.3% in Q1:22-23—the highest level in three years.

Non-oil non-gold imports remained resilient but merchandise exports growth faced headwinds in an unsettled external environment

The monsoon rainfall was 7% above the long period average (LPA) as on September 29. Kharif sowing was 1.7% above the normal sown area as on September 23.

The production of kharif foodgrains as per the first advance estimate is only 0.4% below the first advance estimate.

The reservoir levels are at 87% of the full capacity on September 29, 2022 as against the decadal average of 77%.

Industrial activity reflected in the growth of Index of industrial production (IIP) (y-o-y), slipped to 2.4% in July.

The manufacturing purchasing managers index (PMI), however rose to 56.2% in August.

Services PMI rebounded to 57.2 in August from 55.5 in July.

Real GDP growth for 2022-23 is projected at 7.0 %.

Q2 at 6.3%, Q3 at 4.6%, and Q4:2022-23 at 4.6 %.

The growth for Q1:2023-24 is projected at 7.2%.

Imported inflation pressures felt at the Beginning of the financial year have eased but remain elevated across food & energy items. Edible oil price pressures are likely to remain contained on improved supply from key producing countries and measures taken by the Government.

There are upside risks to food prices. Cereal price pressure is spreading from wheat to rice due to the likely lower kharif paddy production.

The lower sowing for kharif pulses could also cause some pressures.

The delayed withdrawal of monsoons and intense rain spells in various regions have already started to impact vegetable prices, especially tomatoes. These risks to food inflation could have an adverse impact on inflation expectations.

Assuming crude at US$ 100 per barrel in H2:2022-23 inflation is projected at 6.7% in 2022-23, with Q2 at 7.1%, Q3 at 6.5%, and Q4 at 5.8% with risks evenly balanced.

CPI inflation is projected to further reduce to 5.0% in Q1:2023-24.

If high inflation is allowed to linger, it invariably triggers

second order effects and unsettles expectations.

Surplus liquidity in the banking system moderated to 2.3 lakh crore during August - September 2022 (up to September 28) from 3.8 lakh crore during June-July.

This FY (up to September 28), the US dollar has appreciated by 14.5% against a basket of major currencies. Indian Rupee (INR) has only depreciated by 7.4% against the US dollar during the same period.

Our interventions in the forex market are based on

continuous assessment of the prevailing and evolving

situation from the point of view of our approach.

During the pandemic, forward guidance was helpful in anchoring market expectations. In a policy-tightening cycle it’s hard to provide consistent forward guidance given the highly uncertain environment.

In fact, forward guidance may even destabilise financial markets.

Current account deficit (CAD) for Q1:2022-23 is placed at 2.8% of GDP with trade deficit at 8.1% of GDP.

Various leading indicators, including global PMIs, point to weakening of global growth momentum and downside risks to global trade.

India’s import growth, though decelerating, outpaced export growth.

Services exports continued to grow at a robust pace amidst resilient demand for software and business services and modest recovery in travel services.

On a balance of payments (BOP) basis, exports of services grew at a robust pace of 35.4% (y-o-y) in April-June this year.

Remittances rose by 22.6%. The net surplus on exports of services is expected to partly offset the higher trade deficit.

Net foreign direct investment (FDI) improved to US$ 18.9 billion in April-July 2022 from US$ 13.1 billion a year ago.

Foreign portfolio investors (FPIs) returned with net inflow of US$ 7.5 billion during July-September after an outflow for nine consecutive months.

India’s foreign exchange reserve of US$ 537.5 billion as on September 23, 2022 are favourable compared to peer economies.

~67% of the decline in reserves during the current FY is due to valuation changes from an appreciating US dollar and higher US bond yields.

India’s external debt to GDP ratio is the lowest among major EMEs. In the final analysis, we remain confident of meeting our external financing requirements comfortably.

Inflation and GDP projections:

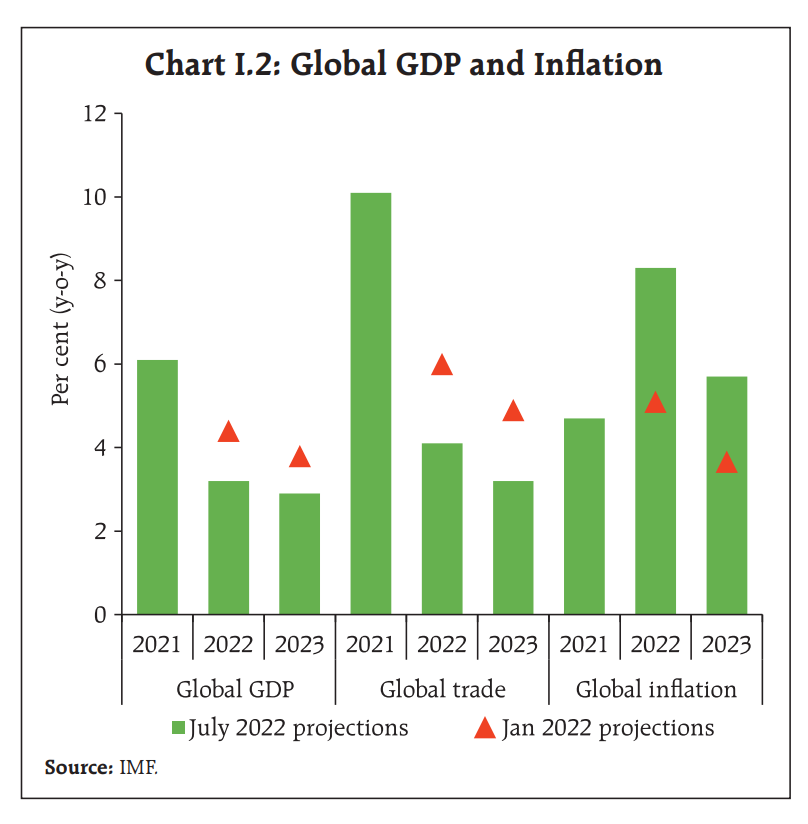

Global GDP and inflation projections:

Global economic prospects have weakened significantly since the April MPR.

Global trade is slowing down & recessions fears in major economies are rising. The global composite Purchasing Managers Index (PMI) contracted Aug 2022 for the first time since June 2020.

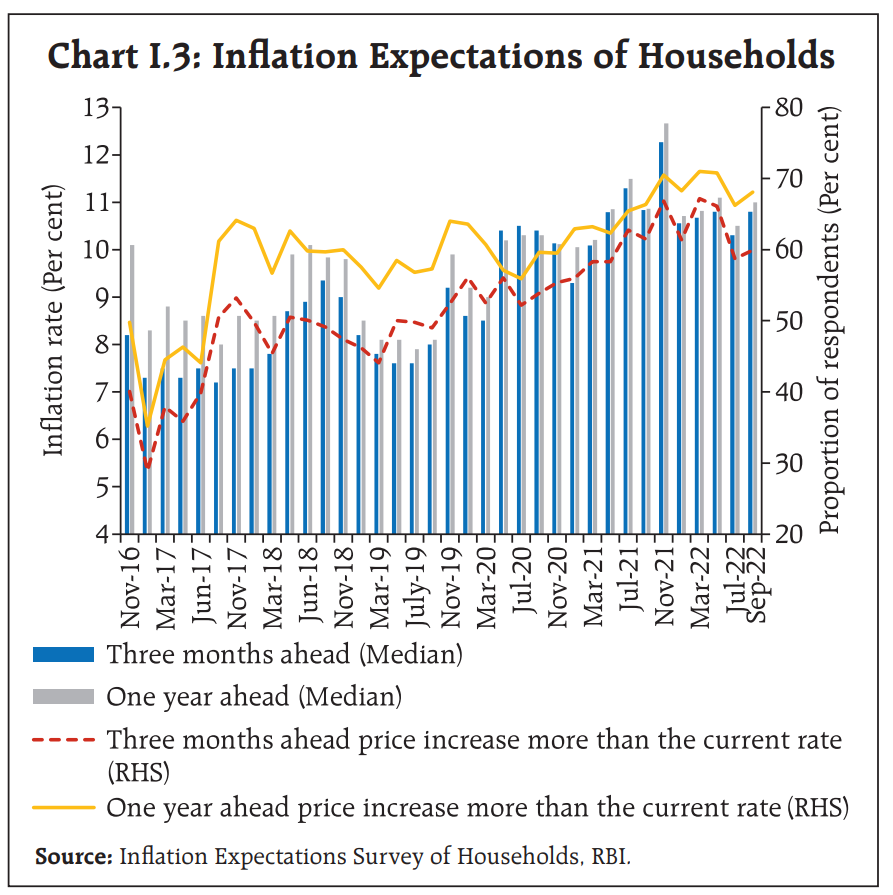

Household inflation expectations remain eleveated:

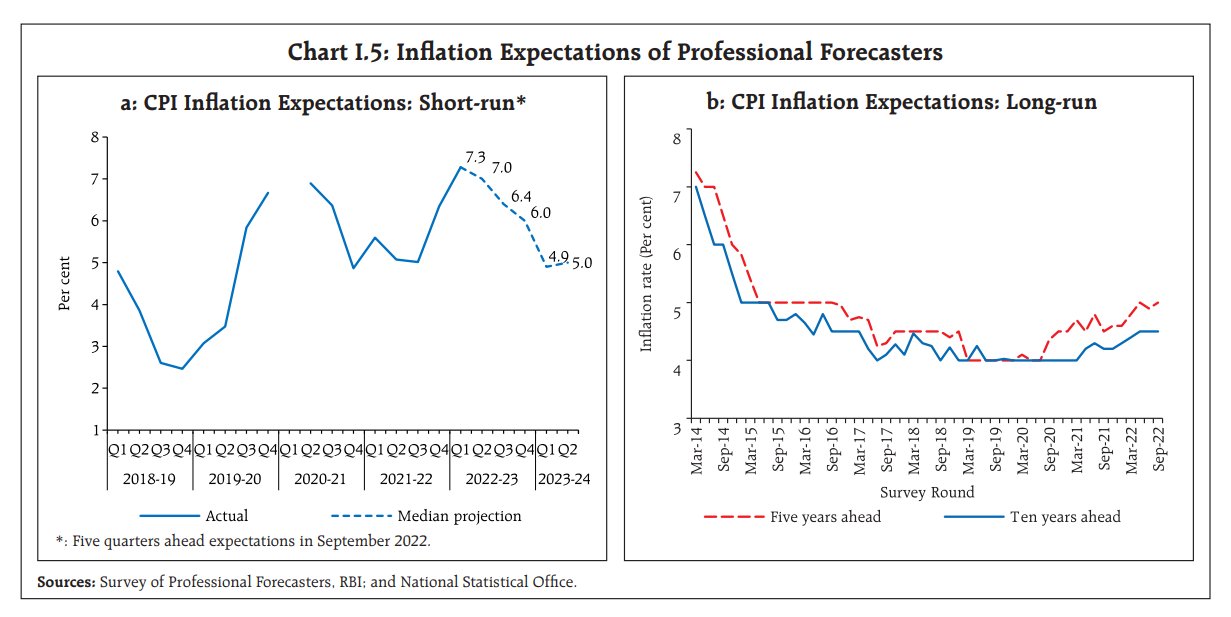

Will inflation moderate according to forecasts?

Supply shocks are a source of significant amount of inflation:

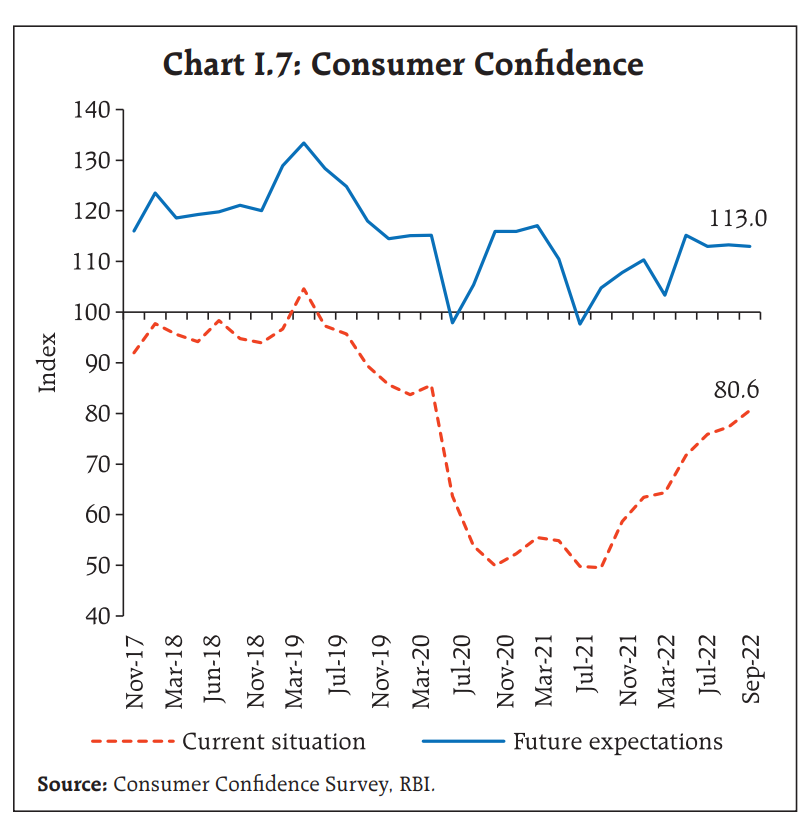

Though overall confidence remained in the pessimistic zone. Households remained optimistic for the year ahead:

Services sector companies expected slight moderation while infrastructure companies expected a minor uptick in Q3:2022-23 in terms of the overall business situation:

Growth projections

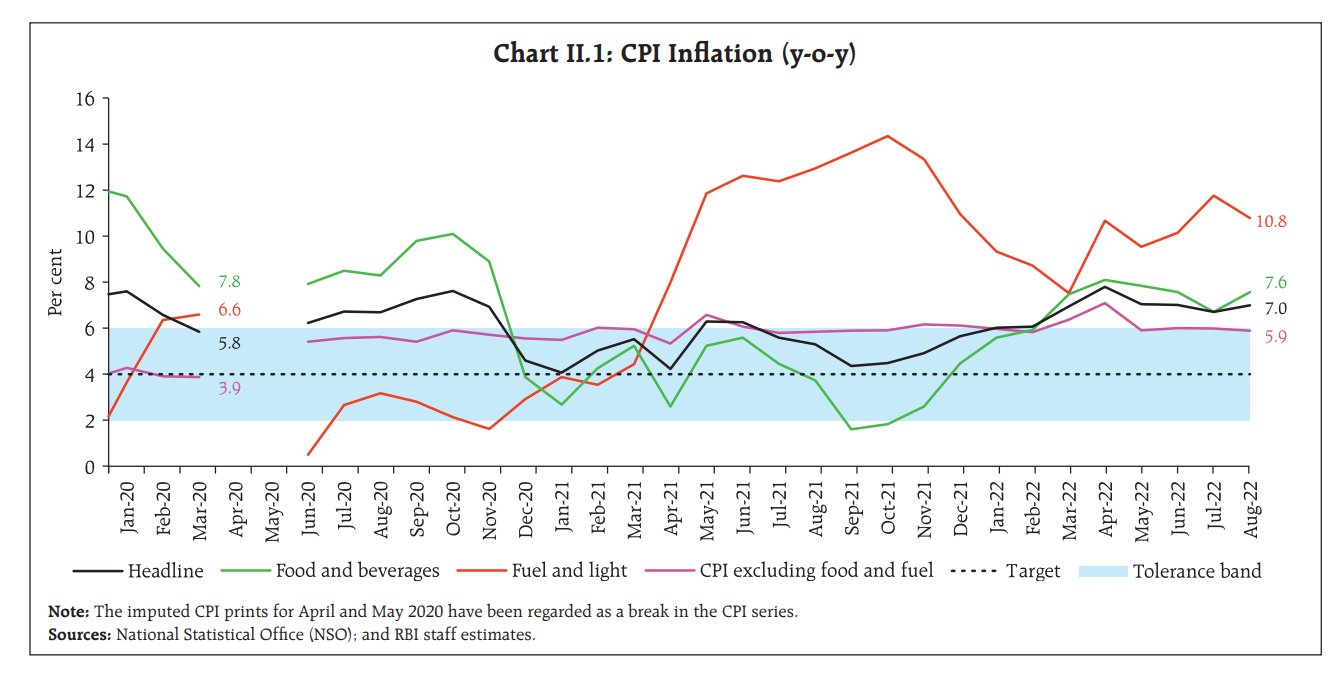

Component wise inflation

This is fascinating. Supply-side shocks from food along with fuel price shocks contributed to high demand while aggregate demand conditions continued to exert downward pressure on inflation:

**During March-August 2022, goods inflation contributed 86% of headline inflation. Perishables like milk, tomatoes, potatoes, and edible oils were the main drivers. **

Durable goods contributed 12.8% and services 14%>

One of the worries is core inflation (CPI excluding food & energy) is becoming sticky.

This is being driven by increase in the prices of clothing, footwear, household goods, personal care items, fast-moving consumer goods (FMCGs) health, transport and communications goods:

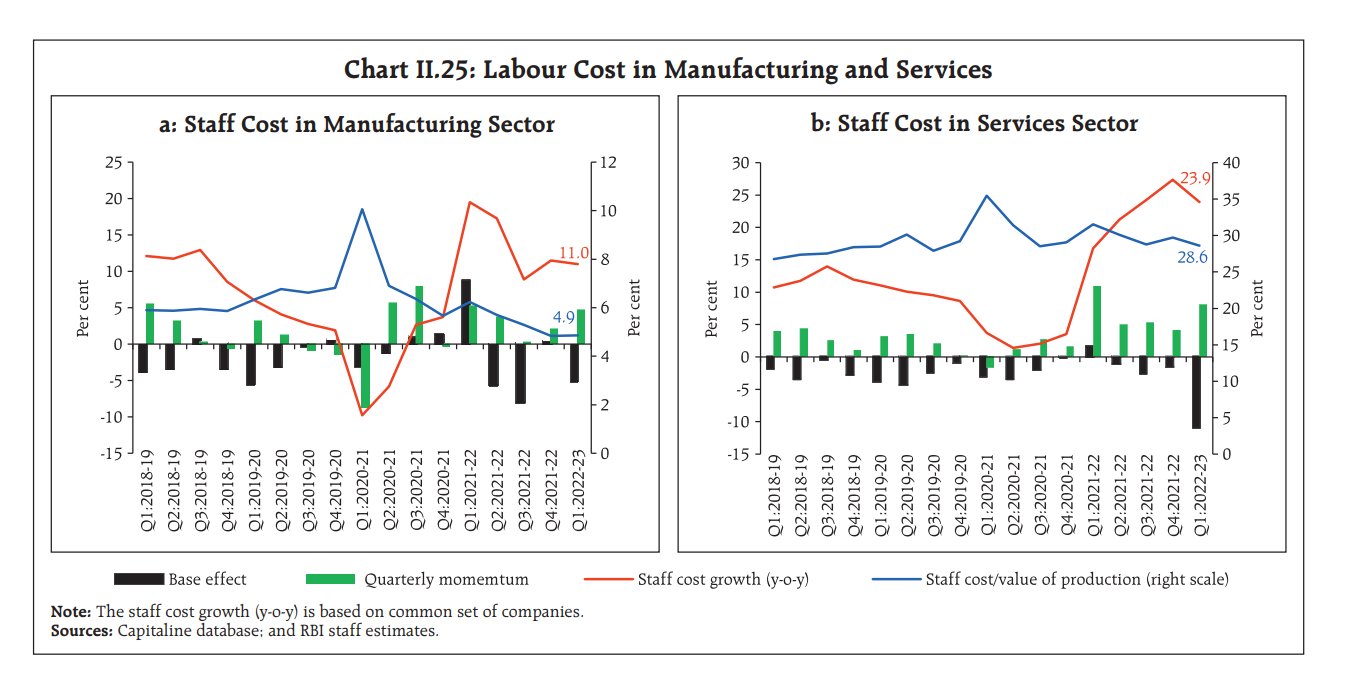

Labor costs:

You can read the full report here: