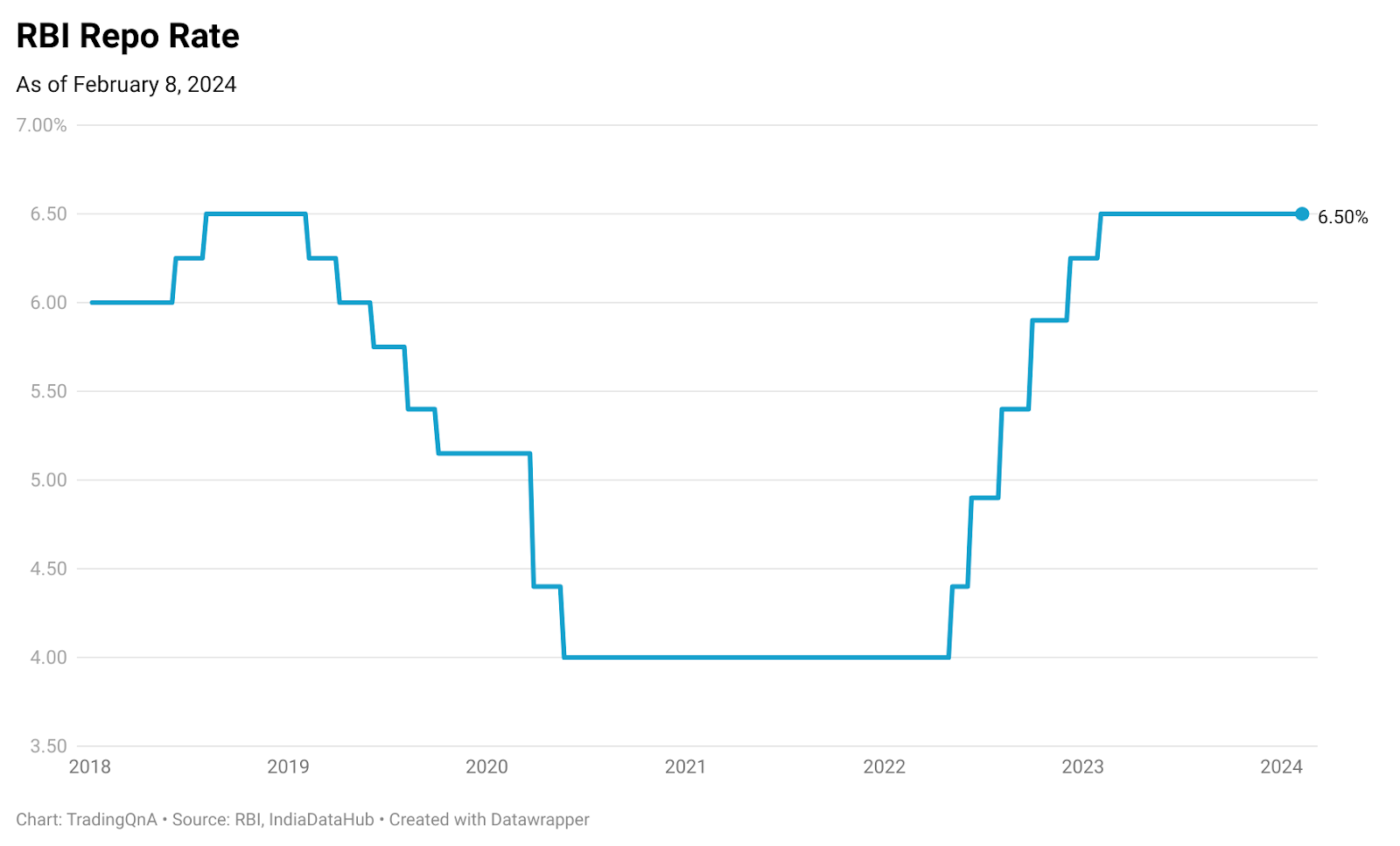

In its latest meeting, the RBI Monetary Policy Committee kept the repo rates unchanged at 6.5%. This is the sixth straight meeting where the RBI decided to keep rates unchanged.

5 of the 6 MPC members voted to keep the repo rate unchanged. One member voted to reduce the rates by 25 basis points.

Policy stance

The MPC also decided to remain focused on the withdrawal of accommodation to ensure that inflation progressively aligns with the target, while supporting growth.

An accommodative stance means the central bank is prepared to expand the money supply to boost economic growth. Withdrawal of accommodation will mean reducing the money supply in the system which will help control inflation.

View on Financial Markets:

Financial market sentiments have been fluctuating with changing views about an early pivot by central banks in advanced economies (AEs). The likelihood of lower interest rates has spurred rallies in equity markets, although uncertainty about the timing of interest rate reduction is reflected in bidirectional volatile movements on both sides in the US dollar and sovereign bond yields.

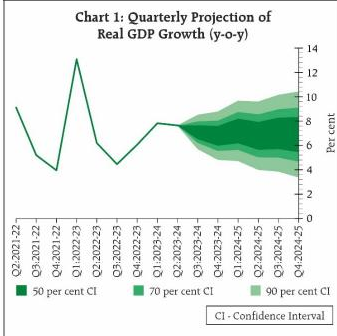

On the domestic economy:

Domestic economic activity is holding up well and is expected to be backed by the momentum in investment demand, optimistic business sentiments, and rising consumer confidence.

Looking ahead, recovery in rabi sowing, sustained profitability in manufacturing, and underlying resilience of services should support economic activity in 2024-25.

Among the key drivers on the demand side, household consumption is expected to improve, while prospects of fixed investment remain bright owing to an upturn in the private capex cycle, improved business sentiments, healthy balance sheets of banks and corporates; and the government’s continued thrust on capital expenditure.

Improving the outlook for global trade and rising integration in the global supply chain will support net external demand. Headwinds from geopolitical tensions, volatility in international financial markets, and geoeconomic fragmentation, however, pose risks to the outlook.

GDP Projections

Taking all these factors into consideration, real GDP growth for 2024-25 is projected at 7.0% with Q1 at 7.2%; Q2 at 6.8%; Q3 at 7.0%; and Q4 at 6.9%.

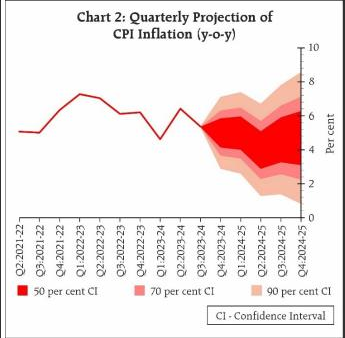

Inflation:

On the inflation front, large and repetitive food price shocks are interrupting the pace of disinflation that is led by the moderation of core inflation. Geopolitical events and their impact on supply chains, volatility in international financial markets, and commodity prices are key sources of upside risks to inflation.

From 4.9% in October 2023, CPI inflation increased successively in the next two months to 5.7% by December. Food inflation, primarily vegetable price increases, drove the pick-up in headline inflation, even as deflation in fuel deepened. Core inflation (CPI inflation excluding food and fuel) softened to a four-year low of 3.8% in December.

Going forward, the inflation trajectory will be shaped by the evolving food inflation outlook. Rabi sowing has surpassed last year’s level. The usual seasonal correction in vegetable prices is continuing, though unevenly. Yet considerable uncertainty prevails on the food price outlook from the possibility of adverse weather events. Effective supply-side responses may keep food price pressures under check.

Taking into account these factors, CPI inflation is projected at 5.4% for 2023-24 with Q4 at 5%. Assuming a normal monsoon next year, CPI inflation for 2024-25 is projected at 4.5% with Q1 at 5.0%, Q2 at 4.0%, Q3 at 4.6% and Q4 at 4.7%.