Buy all stocks in the same ratio of a particular index

Buy Index fund or ETF

If I go for option 1, I will be eligible for all corporate actions. But, one corporate action which troubles me is dividend. I am not a fan of dividend. I would prefer capital appreciation instead of dividend for the obvious reason that dividend will be taxed at 30 percent. If I just buy an ETF, then the value of dividend gets added to the NAV of the scheme. Ultimately at the time of sale, it will result in capital gain which is at a lower tax rate. Expense ratio of index funds and ETFs is much lower than the tax rate multiplied with dividend yield.

Am I getting this right? Or I am missing out on something?

The reason for this query is I am holding most of the IT and FMCG large caps. And the dividend that I get from these go into 30 percent tax bracket.

So I was planning to sell off individual stocks in the same ratio of its weight in the index. Let me elaborate this.

Lets say I have a total value of FMCG stocks of 10L.

I will buy FMCG ETF of 10L. If HUL takes 30 percent weight, I will sell HUL valuing 3L and so on. If I do that as per my current calculations I wil get able to cover as much at 9L from my current holdings. 1L will be the ones which I am currently not holding and they have negligible weight.

What will I save?

Dividend yield on fmcg is around 3 percent. Thats 30k. Tax on that is around 9k.

ETFs have 10 percent haircut on pledge for margin. Stocks have at least 20. All my stocks are pledged. So I will get at least extra margin of 1L. Even if I consider 5 percent return on the same its another 5k per annum.

What are my costs.

Cost of these trades to be executed one time.

Expenses of the fund or etf annually.

Opportunity cost of funds when I have to unpledge the stocks worth 10L and again pledge ETF after 2 days.

I would really appreciate if you guys would give your analysis on this.

I will add few points to further thought process, without giving verdict on any side.

Not all stocks you want to hold will be available in ETF, especially in proportion you want. So you might end up holding both stock and ETF. This complicates the matter when you want to get rid of a specific stock due to market condition. Eg. There is Big negative news out in HUL and now you no longer want to hold it. But you can’t just sell it alone in ETF now. You either sell everything or Hold everything

Pledge

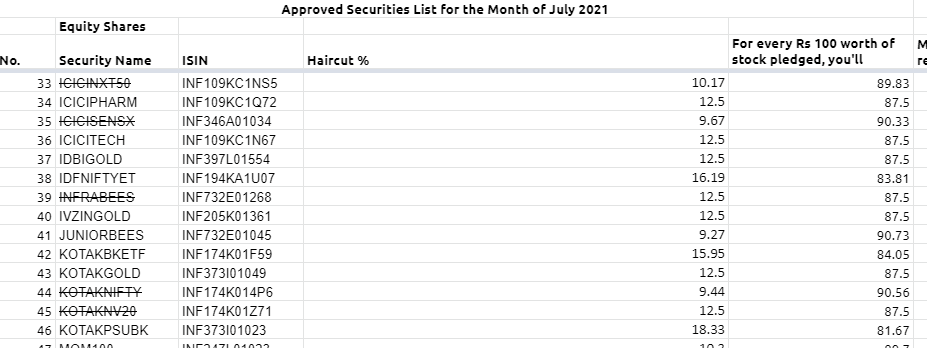

This is not true for all ETFs. Have a look at Zerodha list

While some are under 10, mostly they are debt etf or gold. Stock etf most are above 10, some as high as 18. Also remember that not all ETFs will be available for pledging.

Right now it isn’t in the proportion of index weight. But with 10L I should be able to sell to the extent its included in ETF.

Yes. Agree. I will end up both stock and ETF.

Well. Totally agree on this. I will not get exit from the stock. When I was considering this, I had it in my mind that I won’t be selling these for very long time. But what you said makes sense.

I should have actually check the exact haircut. I did see the icicitech which is 12.5. FMCG was only an example. I was first planning to do this with IT ETF from icici. Its liquid enough and also already in the approved list.

I was anyways not gonna implement this so early with fmcg because it will take minimum 2 months by the time it comes to approved list. Also will have to wait and see the liquidity.

Stocks are more than 20 percent. So I still feel the minimum difference will still be 10 percent on an average.

My point was about the CG that may arise on the one-time sale, when you “convert” your stocks to MF units. Since you listed the cost of selling the shares (which is more or less just the taxes, with Zerodha), I thought you may want to consider the CG aspect of this sale as well.

If I am not wrong, it was before dividend was taxable in the hands of the unit holder. But yes, if its declared then the sole purpose of whatever I said is lost.

Yes. This too has to be considered. But another way to see it, I will be spreading my capital gains in two years.

I would have to pay capital gains tax now when I convert stock to ETF and again when I sell ETF.

My cost of acquisition will increase for capital gains calculation in future. But since I am not considering sale of these stocks for very long, the cash flow now is worth considering. Or at least opportunity cost of those funds are to be considered.

Yes. Thought about that too. There is also timing risk with this. Stocks will be sold when market is live and mutual fund allotment will be at the end of day NAV.

Can make a difference upto 2 percent.

Expense ratio will be slightly higher too. All of these costs will almost be equivalent to the tax on dividend that I am trying to save.

May be I can bring down the difference to less than 0.5 percent by placing order for the fund before cut off time and selling stock at 3.15 or so which will be very close to closing price.

That SBI ETF declaring dividend was weird scenario. EPF trust holds a boatload of that ETF and It was done with the sole purpose for EPF to book some income which can be used for yearly interest.

In my opinion, Stay away from that SBI ETF, and you will not face that problem of dividend

True. I was anyways considering IciciTech and IciciFmcg.

Icici fmcg is still at NFO stage. So even if I decide to do this, it will be at least after 6 months from now.

I will quantify all the negatives you guys have given me. Only of its really worth the trouble I shall go head. Otherwise No.

I chose SBI as AMC for my ETF because it was Government owned and it had a massive corpus of 96,000 crore. Also they will have their own market makers so that the issue of liquidity creation is avoided. I am sure the backlash that this has caused will make them rethink and do what Brittania did - issue bonus debentures or something else.

I wish the ETF also created two categories growth and dividend option.

I am told that for nifty 50 etf, SBI, Nippon and Icici are good AMCs. Among these three name, sBI stand out. Anyways lets see what they do during the current year.

Yes, there is nothing wrong with SBI per se. I am just trying to give some history why they declared dividend.

Yes of which around 80% would be because of EPFO holding and hence ETF’s decision making is also biased towards that. EPFO wanted money and hence they did some jugglery to get money to them. Retailers got unanticipated tax bill in the process.

And since EPFO is dominant investor, there is nothing to stop this in future. Hence I said stay away from that particular ETF. Nothing against SBI AMC.