Certain mistakes can prove to be costly to your investing journey. Let’s understand what these are and how to avoid them:

Mistake 1: Starting without a financial goal

Before investors start investing, the very first step is to have a financial goal in place. How do you want your money to work for you?

It may be a much-needed vacation, building a dream home, or a retirement. Investors should try encapsulating their goals into a financial statement. For instance, “I want to save Rs.50,00,000 to meet my daughter’s fees when she goes to college after 10 years.” A financial goal must have a clear goal, with time in hand and the target corpus needed.

Remember, an investor’s goal is unique and should not be compared with other investors. So, avoid jumping on the bandwagon of investing in popular NFOs or IPOs without having a firm goal in mind.

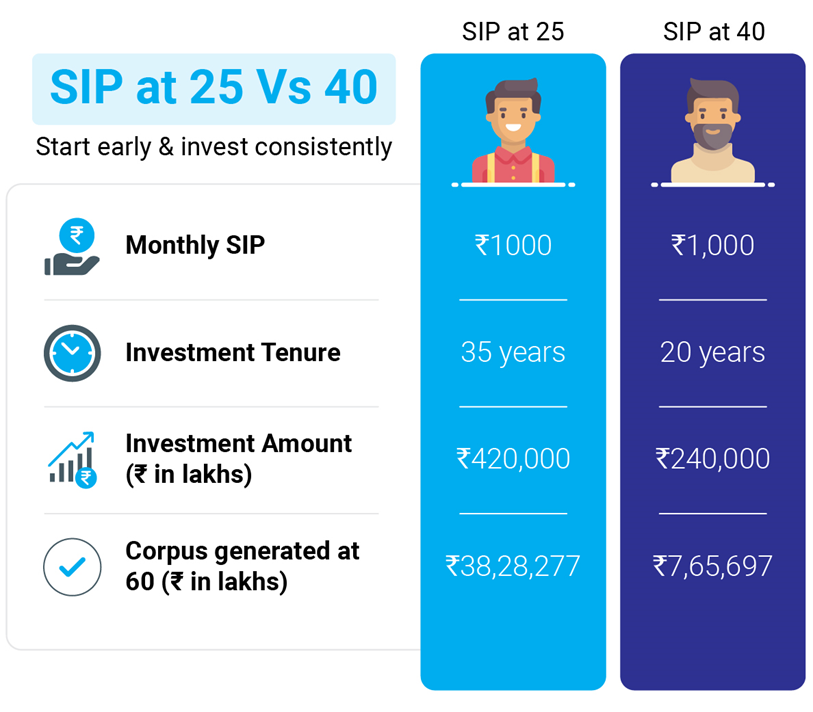

Mistake 2: NOT starting or starting late

Investors should realize the ill effects of procrastinating or, worse, not starting at all. Before investors begin their financial journey, they must rid ourselves of all biases such as inertia or fear of losses, or uncertainty about how much they need to save.

No matter however small the investment size is, it’s important to begin investing. Every day that an investor defers investing, they end up missing out on the opportunity to grow their investment. Let’s see an illustration of how two investors who have started monthly SIP of just Rs 1000/month with a 15-year difference resulted in a gap of over Rs 30 lakh @ assumed rate of return of 10% CAGR. Therefore, it is important to start even though it is a small step.

The above infographic is for illustration purposes only. Investments through SIP are subject to market risk and do not assure a profit or returns or protection against a loss in a downturn market.

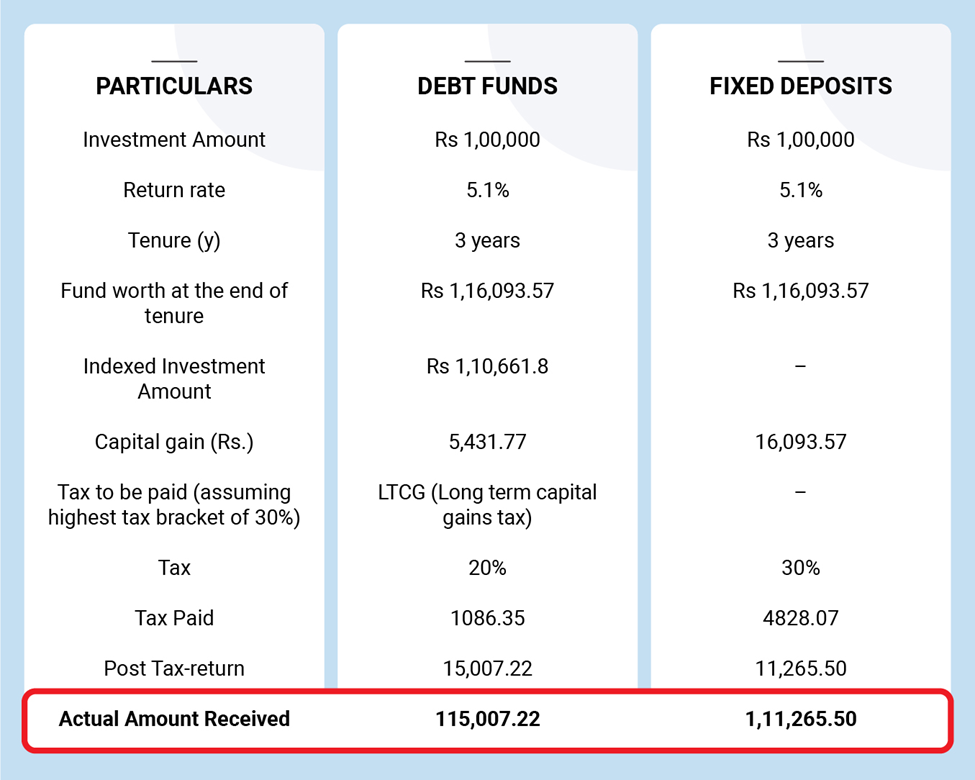

Mistake 3: Parking one’s money in conventional investments

When it comes to building a reserve for one’s future, one needs to look for options beyond fixed income instruments and invest in equities with long-term duration. Over the long term of three years or longer, debt funds are tax efficient due to the indexation benefit.

Let’s understand indexation benefit with an Illustration. Suppose an investor invested Rs.1,00,000 in Jan 2018 and redeemed his investment 3 years later in Jan 2021. For the sake of comparison, the rate of return on debt mutual fund has been assumed at the same rate of an FD at 5.1%

The above table is for illustration purposes to explain the benefit of indexation.

As we see in the table above, the indexation benefit accommodates for the inflation costs to calculate the taxable amount on your returns.

Investors who have a conservative approach can start small and can opt for a systematic investment plan (SIP), that allows them to invest fixed amounts monthly and helps them average their cost of investment over the long term.

Mistake 4: Untimely redemptions

In the investing game, it pays to be consistent. One does not get rich by chasing short-term profits. Unless one is nearing their financial goals, it is suggested that investors should not redeem from their investments. Moreover, as investors, one needs to be mindful of the exit load, taxation, etc.

Sometimes, it may be an unforeseen emergency such as unexpected travel expenses or medical expenses that is forcing one to redeem their investments. At such times, instead of completely redeeming from one’s investment corpus and stopping their wealth goals, an investor can switch or transfer the money needed from his equity mutual fund to his Liquid Fund and reinvest back to equities as needed. In any event, it does make sense to maintain an emergency corpus equivalent to 12 months of expenses in a Liquid Fund or Bank Account. Some mutual funds allow insta-redemption facility on their liquid fund up to Rs. 50,000 making these an ideal option to park emergency funds.

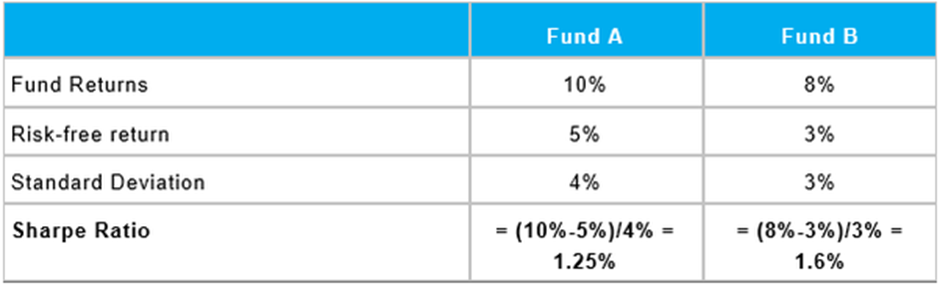

Mistake 5: Comparing mutual funds based on historical returns

When going about comparing two mutual funds, there are certain parameters that one should take into consideration. Evaluating mutual funds based on historical returns could be the starting point for the analysis. However, it cannot be the sole method of evaluating or comparing mutual funds. Therefore, one should look for consistency and not necessarily the rankings or returns alone.

If investors want to compare two funds offering similar returns, then different risk measures such as Sharpe ratio can be a deciding factor.

For instance, a higher Sharpe ratio might mean the fund has the potential to protect investors from market downsides.

Let’s understand this by comparing two funds.

Fund A generates a return of 10%, while fund B delivers an 8% return.

On an absolute basis, fund A has performed better than fund B. But the Sharpe ratio of fund B is better, delivering better risk-adjusted return.

In this example, Standard deviation measures how much a fund’s returns can fluctuate from its historical average. For instance, a standard deviation of 4% in the above example indicates Fund A returns can fluctuate between 6-14%, while Fund B returns can fluctuate between 5-11%.

Investors can also look at other quantitative parameters like underlying portfolio composition, portfolio turnover ratio and qualitative parameters like quality of fund house.

Good investment outcomes come from combining statistics with insights.

Thus, periodic review of one’s existing investment portfolio can provide insight into how to balance one’s portfolio to avoid costly mistakes that can reduce the return on mutual fund investment.

*Note: The comparison with Fixed Deposits has been given for the purpose of the general information only and not a recommendation to invest. Investments in mutual funds should not be construed as a promise, guarantee on or a forecast of any minimum returns. Unlike fixed deposit with Banks there is no capital protection guarantee or assurance of any return in mutual funds investment. Investment in Mutual Funds as compared to Fixed Deposits carry moderately high risk, different tax treatment and subject to market risk and any investment decision needs to be taken only after consulting the Tax Consultant or Financial Advisor

Disclaimer: The views expressed here in this Article / Video are for general information and reading purpose only and do not constitute any guidelines and recommendations on any course of action to be followed by the reader. Quantum AMC / Quantum Mutual Fund is not guaranteeing / offering / communicating any indicative yield on investments made in the scheme(s). The views are not meant to serve as a professional guide / investment advice / intended to be an offer or solicitation for the purchase or sale of any financial product or instrument or mutual fund units for the reader. The Article / Video has been prepared on the basis of publicly available information, internally developed data and other sources believed to be reliable. Whilst no action has been solicited based upon the information provided herein, due care has been taken to ensure that the facts are accurate and views given are fair and reasonable as on date. Readers of the Article / Video should rely on information/data arising out of their own investigations and advised to seek independent professional advice and arrive at an informed decision before making any investments. None of the Quantum Advisors, Quantum AMC, Quantum Trustee or Quantum Mutual Fund, their Affiliates or Representative shall be liable for any direct, indirect, special, incidental, consequential, punitive or exemplary losses or damages including lost profits arising in any way on account of any action taken basis the data / information / views provided in the Article / video.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.