In US, I do not think any of the banks offer any meaningful rates for CASA balance. They got access for such huge deposits because of the failure of few small banks. This had contagion effect on people who have funds in small banks which are still ok, started moving out to the big banks.

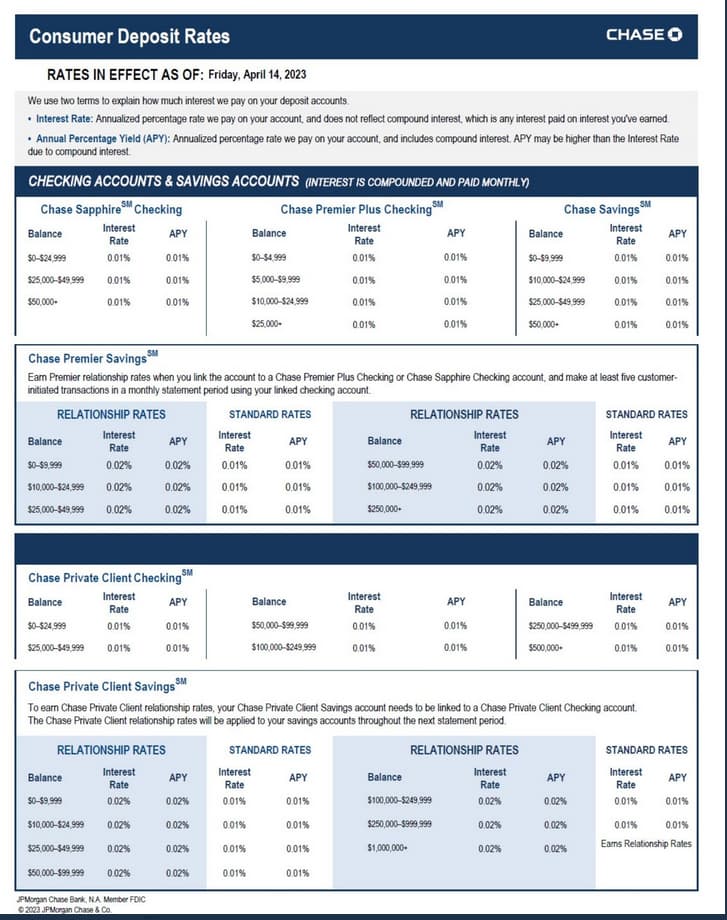

One of my relative asked me if it is was ok to keep money in Chase. She is a research scientist and have limited knowlege of banks. Her collegues have been talking about this and wanted my views. Her surplus funds is kept in FCNR deposit in Indian Banks which is getting 5.5% for 3 years as even chase does not give any interest on CASA or very nominal thing. What they do is if you keep some high balance then the locker facility is free and things like this.

Disclaimer - The above is from my conversation with my relatives about nil interest on casa balance in US banks

Why can’t all Americans put money in Indian banks and get 7-8% pa. Apart from that, Indian banks are also much more safe than these Global American banks

After conversion it will still be same. With rupee depreciating, the net effect will be the same.

Read about interest rate parity theory to understand this better.

in GDP 80% is corruption , if bank get more money from america these bank give loans to big another mallaya - nirav modi and they will give high loan to himself or bank manager relative , then the new scam india need to see-or another 5 SVB bank india need to see . so only americans doesit want to deposit here sir

I find @Jason_Castelino argument more logical. Assuming an American deposits USD 100 in an Indian Bank at 7 % pa on April 1 2022. At that time Dollar was around 76 Indian Rupees. So it works out to be ₹ 7600. After one year he earns ₹ 532 interest (7 % of 7600) so 7600+532=8132. Now he decides to take his money back home on April 1 2023. So 8132/82=99.17 (Dollar was around 82 on April 1 2023). Add to that currency conversion costs for first converting USD to INR and then vice versa. Net net its a loss.

To the best of my knowledge only NRI and Person of Indian Origin (PIO) holding Amercian citizen can open an account/FCNR deposit in India. A person who is not of indian origin cannot open FCNR deposit.

Few years back, the FCNR rates were below 2% (approx) so it did not make any sense for an PIO to place the deposits. It was only during the last 8 months or so when the INR started depreciating that FCNR rates were increased. Yes now it is a great time to place the deposit for NRI and PIO holders.

They should be placing the deposit on FCNR basis so that there is no currency risk. They still get 5.5% which is quite attractive. Only gulf NRI who know that they have to come back to their home country one day or the other will place the money in NRE deposits and get the 6 to 8%. Indian origin Amercan citizen will never come back to India and hence it is pointless for them to place the deposit in NRE and get 6 to 8%. However, as mentioned before, because the rates on USD deposits are higher now, few are moving the money to India in FCNR deposits. Also I am told they are taxed on global income basis.

Another major pain point is the movement of money. For the uninitiated, it is a process to ask the bank in India to remit the money back to their account in US. Not saying it is difficult but time consuming if the banker in India goes into IGNORE MODE…

As an example, I got an email from a bank in India that for two of my deposits to add nomination. This scared me, I wrote to them asking that to the best of my knowledge, I always add nomination when opening of FD. The reply I got was even more damning, it says, if I think, I have given the nomination, it is fine there is nothing to worry. Now this episode has created a doubt… I wrote to the branch asking to check their records if the nomination is given or not. Not a reply, it is pure silence, reminders go and I do not get a single reply from the branch…This is called ignore mode. This generally will scare a US citizen who do not have any contact in India (assuming) who wants his money back.

Reminds me of the last scene in Titanic, Rose keeps shouting jack, Jack… from the boat… in my case, I am shouting CSB, CSB… but absolutely no reply…Jack is dead…I only hope CSB is not dead…

Doesn’t your bank show nomination through net banking. After reading your post, I logged in to my internet banking to check if I’ve nominees in my FDs and it’s showing nominee name in netbanking. (Bank name - Central Bank of India & Bank of India)