How costly are regular mutual funds compared to direct plans?

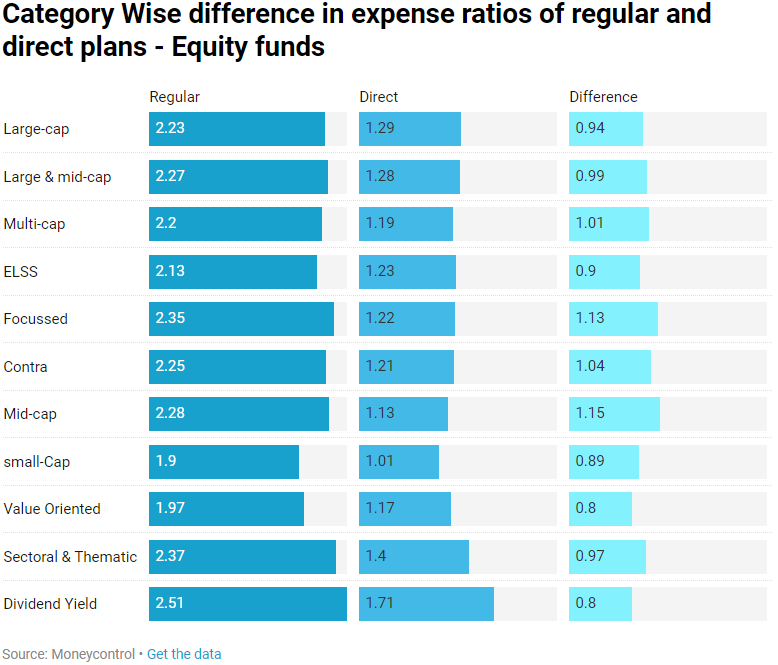

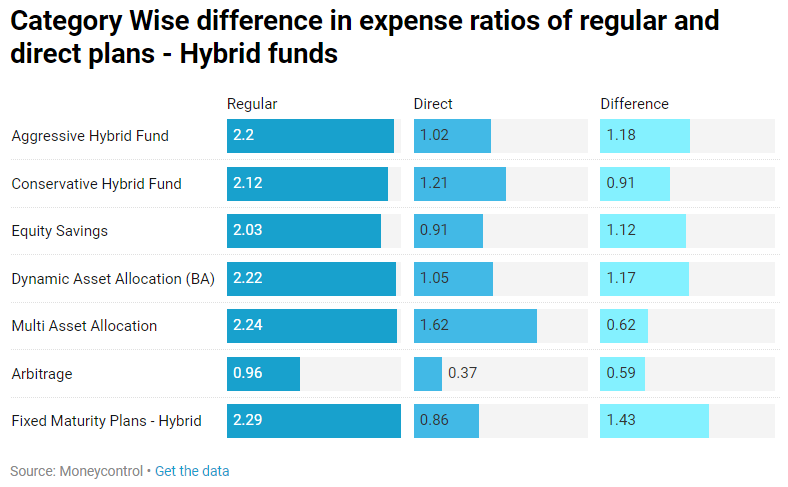

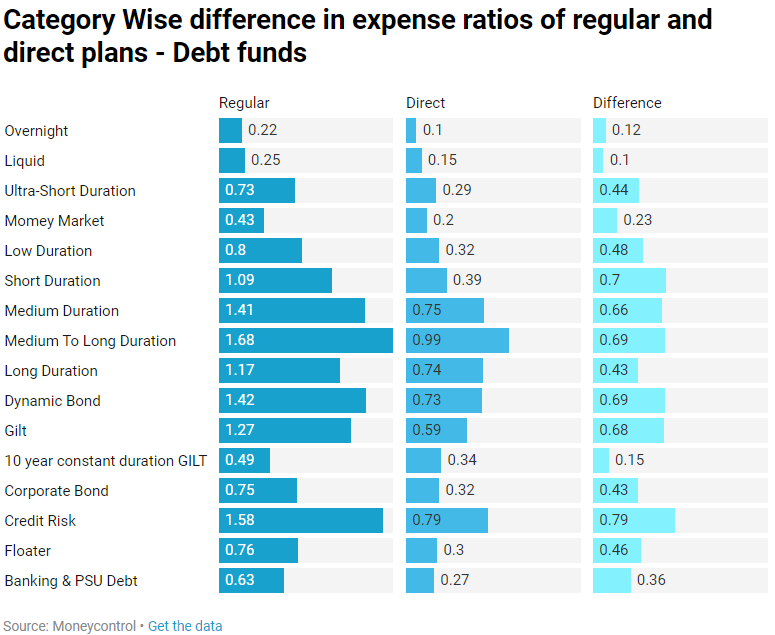

Here’s the category wise difference in expense ratios of direct plans and regular plans. Even after the revision in expense ratio slabs by SEBI there are big differences in expense ratios across categories.

When it comes to investing, there are very few things that are in your control. The two big factors you can control that affect your investment outcomes are costs and behaviour. Unfortunately, a vast majority of investors don’t realize the importance of costs. You might think that a difference of 0.94% in the case if large-cap funds seem trivial. But the thing about expense ratios is that they compound over time and the longer your investment period, higher their impact.

One should not let the miracle of long-term compounding of returns be overwhelmed by the tyranny of long-term compounding of costs - Jack Bogle

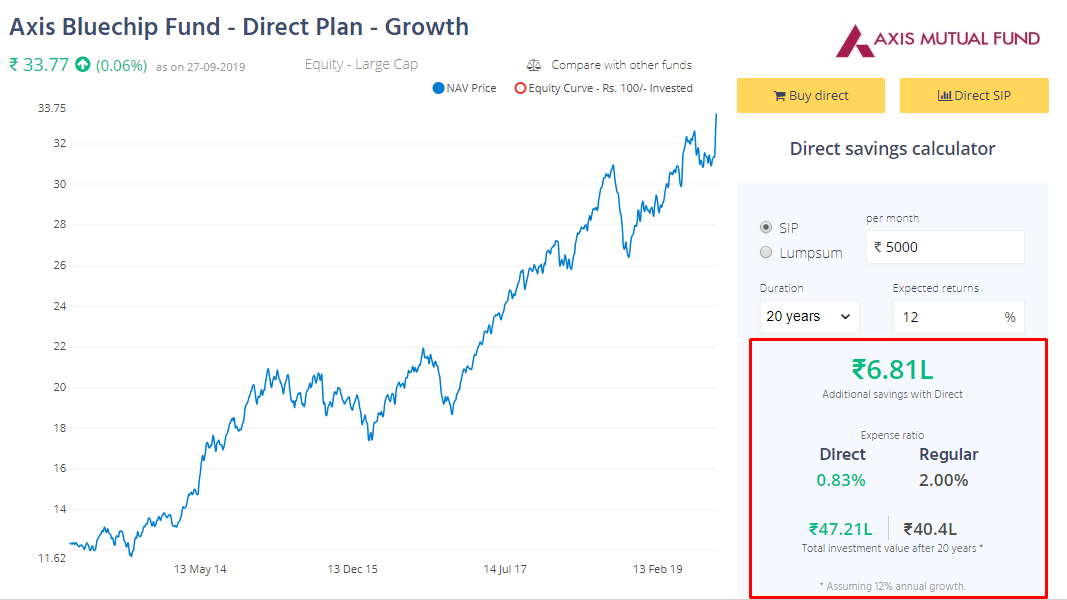

To give you an example, if you were to invest Rs 5000 a month in this fund for 20 years and if we assume a CAGR of 12%. Your corpus in a direct plan would’ve grown to Rs 47.2 lakhs, while the same investment in a regular plan would be Rs 40.4 lakh. A difference of Rs 6.8 lakhs, that is how much you would have lost in commissions.

Remember, you will keep paying commissions for as long as you are invested. so that seemingly tiny difference of 1.1% can have a massive impact on your final investment corpus. By keeping your costs low, you investment outcomes improve dramatically in the long run.

So, here are the average expense ratios across each category of mutual funds.

All numbers in %

Equity funds

Hybrid funds

Debt funds

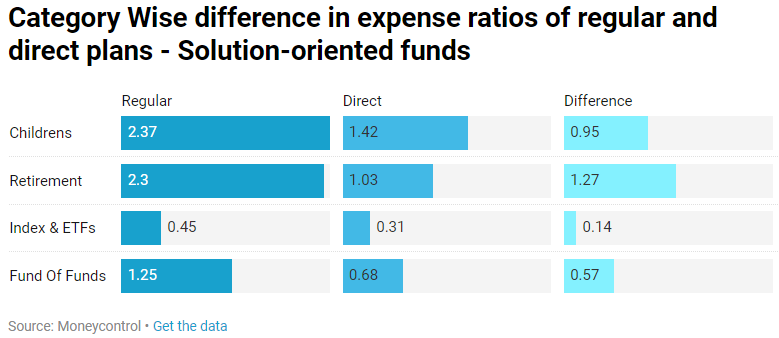

##Solution-oriented schemes

A few notes:

- The average expense ratio of index funds might seem a little misleading because the category includes gold ETFs as well. Today, you can invest in an index fund for as low as 0.10%.

- Don’t invest in Children’s plans and Retirement funds, they are poorly managed and are launched just gather AUM.

- Invest in direct plans and consult a fee-only RIA to save costs at the same time getting proper investment advice.

7 Likes

commission in regular plan is silent profit killer on long term , understand zerodha

commission in regular plan is silent profit killer on long term , understand zerodha

3 Likes

when it is deducted means at time of investing in mutual fund or??

Expense Ratio is deducted on daily basis as tiny fractions of annual value. So everyday when AMC declares NAV, Expense Ratio is already deducted.

6 Likes

So, now how much it costs for 0.83% expense ratio for 30 odd years?

Thanks

The regular mutual funds plan to decrease the corpus by a good 20% to 30%. The difference is compounding nature as is the return.

1 Like

Expense Ratio is deducted on daily basis as fractions of annual value. So everyday when AMC declares NAV, Expense Ratio is already deducted.

1 Like

Expense Ratio will not be deducted when you exit your mutual fund investment. However at the time of exit, there might be Exit Load applicable, this varies from fund to fund and depends on your holding period. You can learn more on this here.

2 Likes

When I buy a mutual fund from Zerodha, am I buying Regular or Direct plan?

1 Like

All mutual funds on Coin are Direct Plans.

5 Likes

So, why do we have even regular plan?

Mutual funds was sell previously(still ) through Agents . The Difference in Expense ratio of Regular-Direct was paid the Agents. Agents used to do lot of paper work, collecting checks , provide research etc.

1 Like

@Bhuvan what are the taxes & other expenses for mutual funds AMCs ?

I still dont understand how does the AMC does an index rebalancing, sell the outgoing stock & buy the incoming stock and still maintain expense ratio below 0.2%

I can not understand how is it possible?

As if Direct Plan NAV is 1, then Regular Plan NAV is always 0.98 or something.

If my buying cost is also low, how can there be a gap in returns, as NAV is already discounted.

Please someone explain,