With a list of tax-saving investment options, choosing the suitable investment can be a cumbersome task. The aim of any tax-saving investment is to help investors save tax and achieve goals for the future. In other words, a good tax-saving investment must be an investment first and a tax saver second. Let’s see how ELSS compares to traditional Section 80C approved investments – like PPF and NPS.

What is ELSS?

An Equity Linked Saving Scheme (ELSS) is an open-ended equity mutual fund that invests at least 80% of the scheme’s assets in equities and equity-related products. Equity Linked Savings Scheme (ELSS) is a tax saving investment to achieve investor’s long-term goals such as child’s education or retirement. It complements their equity allocation to profit from the long-term economic growth in India. ELSS has an AUM of Rs.152,610 crores as per AMFI data as of Oct 31, 2021. This constitutes approximately 11.6% of the total Equity mutual funds.

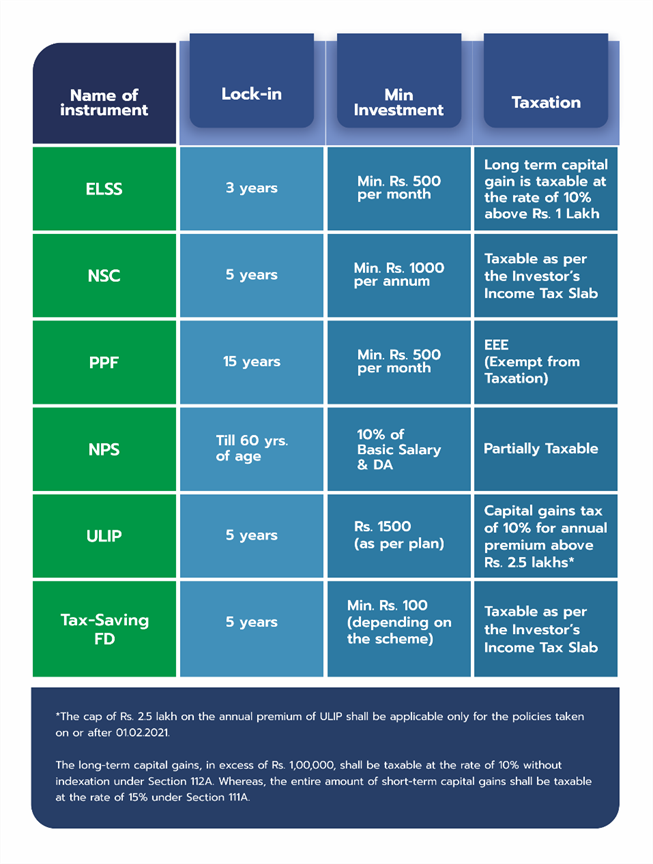

How does ELSS compare with other tax saving instruments u/s 80C?

The following table offers an overview of the taxation and lock-in requirements of the different tax saving instruments.

Why has ELSS been the preferred option?

ELSS funds have been the preferred option in recent years for the following reasons:

a. ELSS funds offer a tax deduction of up to Rs 150,000 under Section 80C of the Income Tax Act. This means upto Rs.46,800 tax benefit can be availed by the investors falling under highest tax bracket.

b. ELSS tax saving funds offer dual benefit: tax exemption, wealth accumulation.

c. ELSS invests primarily in the diversified equity allocation, giving investors the opportunity to earn long term risk -adjusted returns.

d. Lowest lock-in among other tax-saving options giving investors the flexibility to redeem once the lock-in tenure is completed.

Since ELSS mutual funds are equity-oriented funds, they carry similar risks that any other equity mutual fund carry. However, investors can reduce the impact of market volatility with the following ways.

1. Staying invested for five years or longer: Since ELSS is an equity-oriented scheme, investors need to stay invested for the long term to take advantage of the market cycles and ride out the market uncertainty. Also, the mandatory lock-in period of three years helps significantly in reducing the portfolio churn and thereby keep a check on the expense ratio.

2. Start an SIP: Investors can get ahead of their tax planning exercise and start an SIP now instead of waiting till the end of the tax season to invest in a lumpsum later. An SIP brings with it the benefit of rupee cost averaging. This means buying low during bullish markets and more when markets are falling. This essentially averages out the cost of purchase.

But investors should note that every SIP invested will be considered as a fresh investment and will get locked in for three years. If you are investing in lumpsum, investors have the flexibility of redeeming all investments at one go after the lock-in ends.

Irrespective of whether investors choose an SIP or lumpsum, it may be a good time to get ahead of one’s tax-saving and wealth creation goals with an ELSS mutual fund.

Disclaimer: The views expressed here in this Article / Video are for general information and reading purpose only and do not constitute any guidelines and recommendations on any course of action to be followed by the reader. Quantum AMC / Quantum Mutual Fund is not guaranteeing / offering / communicating any indicative yield on investments made in the scheme(s). The views are not meant to serve as a professional guide / investment advice / intended to be an offer or solicitation for the purchase or sale of any financial product or instrument or mutual fund units for the reader. The Article / Video has been prepared on the basis of publicly available information, internally developed data and other sources believed to be reliable. Whilst no action has been solicited based upon the information provided herein, due care has been taken to ensure that the facts are accurate and views given are fair and reasonable as on date. Readers of the Article / Video should rely on information/data arising out of their own investigations and advised to seek independent professional advice and arrive at an informed decision before making any investments. None of the Quantum Advisors, Quantum AMC, Quantum Trustee or Quantum Mutual Fund, their Affiliates or Representative shall be liable for any direct, indirect, special, incidental, consequential, punitive or exemplary losses or damages including lost profits arising in any way on account of any action taken basis the data / information / views provided in the Article / video.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.