Hey @Rishika_Garg,

Excuse me if I go overboard answering your questions. I was planning to write around this topic, especially with many articles over the last few months claiming that equity investing is dropping off a cliff and derivative trading is surging. Comparing the two is like comparing apples to oranges; these headlines also tend to mislead most people who don’t understand the nuances of the capital markets.

Why we shouldn’t compare trading turnovers to determine activity.

Let me give an analogy. If you want to figure consumption of wheat, would you look at all the wheat merchants (traders) who buy & sell wheat for a living to individual households (investors) who consume wheat and come to a conclusion that, wheat merchants are consuming more wheat? It makes no sense, right? Similarly it makes no sense to compare trading activity of active traders to equity investors and come to a conclusion on trends in the markets.

In the capital markets there are few classes of participants.

- Retail investors (buy a stock and hold for few days or more before selling)

- Retail intraday stock trader ( trades stocks for intraday or between 9.15 am to 3.20 pm)

- Retail F&O trader (trades futures & options, either intraday or takes positions for a few days)

- Institutional investors (Institutions that buy and hold)

- Institutional traders (Institutions that participate in active trading stocks and F&O)

When determining retail activity in the markets, I think the right way to determine trends is by seeing the participation in terms of the number of people trading across these classes of participants and not just trading turnovers. This is because, like in the case of the wheat merchants, a few active traders can generate a lot more turnover than many investors. Active traders tend to continue participating when the markets turn volatile or when there are market drops, investor activity typically drops when the overall markets are in a drawdown period.

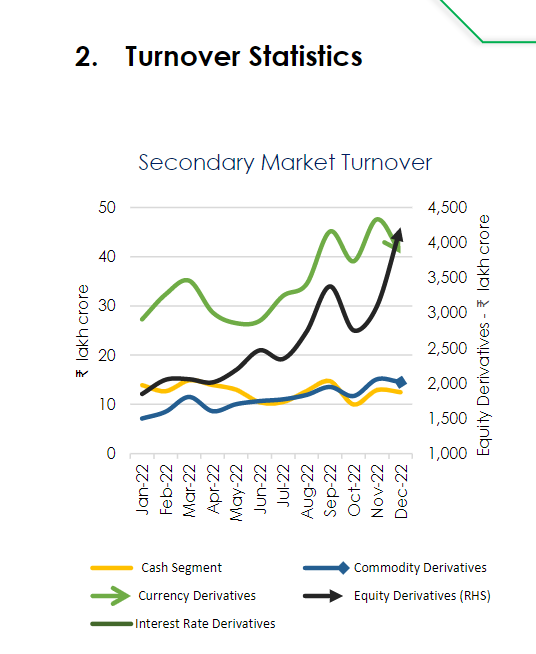

Most data released by the exchanges and regulators are turnover related and not in terms of participation. NSE publishes Market Pulse (page 123 onwards), and SEBI has a monthly dashboard are probably the best ways today to track trading turnover trends.

The above graph regarding trading turnover indicates that turnover in equity derivatives has grown significantly in the last 12 months while the cash segment has remained at same levels. While this is true regarding trading turnover, it isn’t in terms of participation. 90% of trading turnover is contributed by 10% of very active traders (wheat merchants), and the trading activity tends to go up when markets are volatile, which markets have been over the last three years. Trading activity in stocks reduces when markets are not performing well, like in the last one year, and hence cash trading turnover has remained muted.

Cash or equity segment has two types of participants - investors and intraday traders. While the volatility over the last year should have meant higher equity intraday trading volumes matching that of F&O, there have been regualtory changes in the last couple of years that has gotten active traders to prefer derivative segment over cash.

Traders preferring F&O to Cash.

Starting Dec 2020, SEBI capped the maximum intraday leverages a brokerage firm could offer their customers. Until then, a broker could potentially give unlimited leverage. By this, I mean if you had, say, Rs 1000 in your account, a broker could allow you to take positions worth, say, Rs 1lk (100 times leverage) for intraday. As you can imagine, the more leverage, higher the turnovers on the market. Traders love leverage; the higher the leverage higher the potential returns and, of course the losses as well.

While most online larger brokers had some cap, the smaller to mid sized brokers allowed leverage based on relationships. Brokers used leverage to make up for a not competitive product and attract active traders, who tend to be the highest revenue generating customers. The maximum leverage a broker could offer was capped at 20 times in Dec 2020 and slowly reduced to 5 times from Sep 2021.

As an intraday trader in cash segment, you have restrictions like having to square off positions by 3.20 pm and inability to carry short positions overnight. With the leverage offered for intraday stock now reduced to the same levels as the F&O segment, trading on F&O is a much better product.

- For those who trade larger quantities of intraday stock, futures or short option positions are better. Leverage is the same; trades dont’ get auto squared off at 3.20 pm, short positions can be hold overnight.

- For those who trade smaller quantities of intraday stock and can’t afford to post the full margin required for trading the minimum one lot of futures or short option position, buying options would seem like a better product. Buying options also gives much higher leverage, paying a small premium, which can get a large contract value exposure.

So, apart from markets being flat, the reason why derivative turnover is outperforming cash market turnover is also because active intraday traders in equity segment now preferring F&O.

Activity trends by participation.

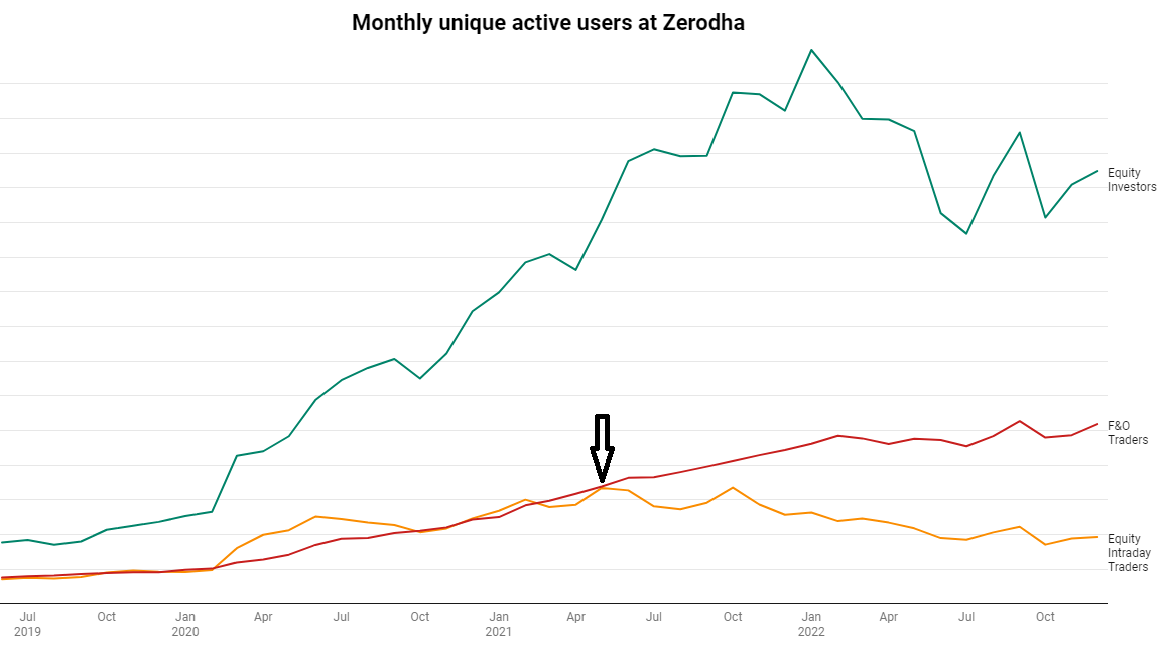

If we have to go down the path of figuring out the retail market participation trends, I think the right way to do this is by looking at the number of participants and not just the trading turnover. Exchanges and regulators don’t publish this data; here is what has happened at Zerodha. Since we are ~20% of the overall retail participation in India, this is quite a large sample size to help come to conclusions.

Monthly unique customers who have traded on the platform

If you were to look at the above graph, equity investor participation has grown significantly more than F&O trading in terms of participation in the last three years. The bump up we see from 2021 in F&O participation is also because of the drop in equity intraday trading participation. This, as I mentioned earlier, is most likely due to leverage restrictions on equity intraday trades, which makes trading on F&O a better product than trading in equity for anyone looking to trading with leverage.

Higher contribution from retail to derivatives segment.

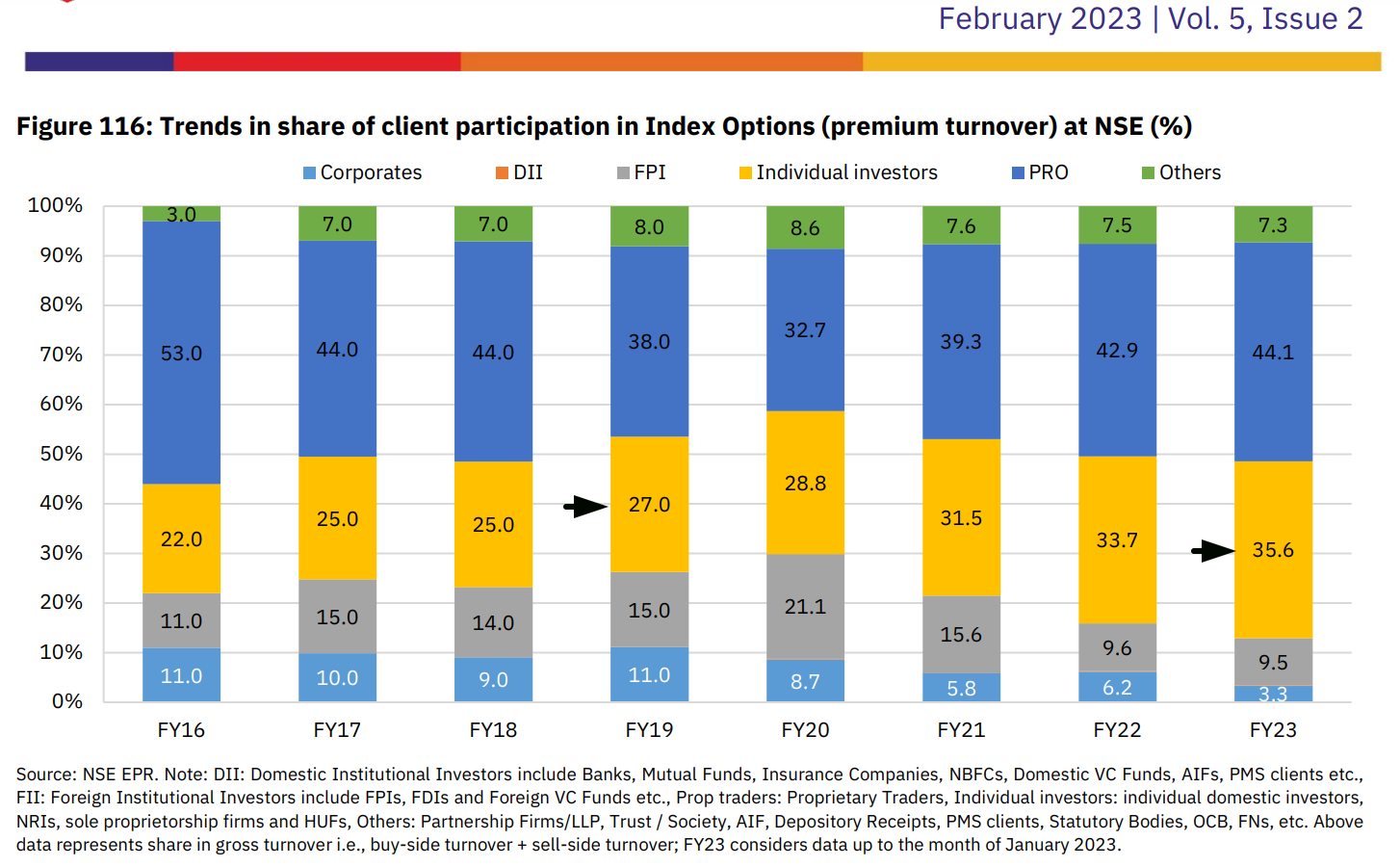

One of the other points that also gets highlighted is how retail trading contribution in derivatives segment and especially the option trading segment, has increased significantly in the last three years (since COVID). Check this image from NSE market pulse, which shows a jump from 27% to 36%.

I think this jump is again due to regulatory reasons. In March 2020 when Covid unleashed volatility in the capital market, SEBI, as a measure to contain risk, introduced open interest (OI) restrictions at entity level. The maximum OI at any entity level is Rs 500 crores worth of positions or, say, around 6000 lots of Nifty. While no retail investors would ever hit this limit, many institutions and prop shops were capped in terms of position limit, so their trading activity has been capped. This maximum OI limit is why I think retail percentage contribution has gone up. This will see a drop whenever the Rs 500 crore OI limit at entity level are increased or removed.

Money at play - equity vs derivatives.

Another way to compare participation trend is to compare the actual money at play. Which is, what is the total money being used at any point of time for taking F&O positions, and how does it compare to the total money used for equity positions.

At Zerodha, if you compare the total money utilised for F&O at any time and compare it total value of stock holdings, it is now ~3%. This percentage has reduced for us over the last few years and significantly.

So…

Yes, trading in F&O has picked up, but not disproportionately, as it is made out in mainstream media. Yes, F&O participation has increased, but equity has increased much more.

Trading in F&O is mostly from active traders who trade irrespective of if the markets are in bull or bear markets. Comparing this turnover to cash market turnover, where the market’s direction significantly determines turnover, isn’t a right comparison. A lot of trading has also moved from trading intraday stocks in cash segment to index F&O segment, which necessarily isn’t bad for the trader since indexes are a much safer product to trade as compared to stocks. This move has mainly been because of regulatory restrictions regarding maximum leverage on intraday trading. The increasing retail contribution in overall derivative segment again is due to restriction in maximum open interest affecting institutions and prop shops and not retail traders.

But yeah, let me add a disclaimer, F&O trading, especially option buying, is extremely risky. We had shared a bunch of things to keep in mind when buying options.