@nithin Increasing F&O trading in India is making headlines quite frequently. Can you tell me why and also some other questions.

For equity options - what % value is traded by retail investors vs institutions?

As we understand, retailers churn significantly, what is the trend for institutions?

Are there enough option sellers in the market? What regulatory overhang on margin requirements exist today?

Given ~90% of option traders make sizable losses - how do we expect their behavior to change? Do people who churn come back on the platform after a certain period?

Why does the mix towards options in India wrt total tx look skewed in India as compared to other geos? How do you expect this share to look like in future?

Excuse me if I go overboard answering your questions. I was planning to write around this topic, especially with many articles over the last few months claiming that equity investing is dropping off a cliff and derivative trading is surging. Comparing the two is like comparing apples to oranges; these headlines also tend to mislead most people who don’t understand the nuances of the capital markets.

Why we shouldn’t compare trading turnovers to determine activity.

Let me give an analogy. If you want to figure consumption of wheat, would you look at all the wheat merchants (traders) who buy & sell wheat for a living to individual households (investors) who consume wheat and come to a conclusion that, wheat merchants are consuming more wheat? It makes no sense, right? Similarly it makes no sense to compare trading activity of active traders to equity investors and come to a conclusion on trends in the markets.

In the capital markets there are few classes of participants.

Retail investors (buy a stock and hold for few days or more before selling)

Retail intraday stock trader ( trades stocks for intraday or between 9.15 am to 3.20 pm)

Retail F&O trader (trades futures & options, either intraday or takes positions for a few days)

Institutional investors (Institutions that buy and hold)

Institutional traders (Institutions that participate in active trading stocks and F&O)

When determining retail activity in the markets, I think the right way to determine trends is by seeing the participation in terms of the number of people trading across these classes of participants and not just trading turnovers. This is because, like in the case of the wheat merchants, a few active traders can generate a lot more turnover than many investors. Active traders tend to continue participating when the markets turn volatile or when there are market drops, investor activity typically drops when the overall markets are in a drawdown period.

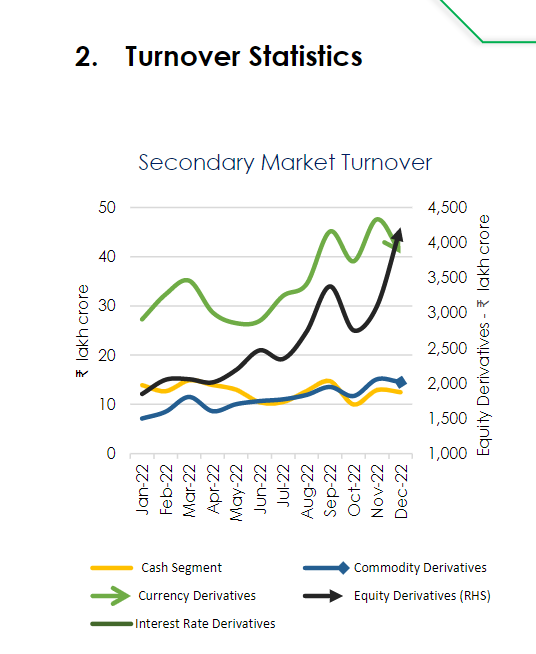

Most data released by the exchanges and regulators are turnover related and not in terms of participation. NSE publishes Market Pulse (page 123 onwards), and SEBI has a monthly dashboard are probably the best ways today to track trading turnover trends.

The above graph regarding trading turnover indicates that turnover in equity derivatives has grown significantly in the last 12 months while the cash segment has remained at same levels. While this is true regarding trading turnover, it isn’t in terms of participation. 90% of trading turnover is contributed by 10% of very active traders (wheat merchants), and the trading activity tends to go up when markets are volatile, which markets have been over the last three years. Trading activity in stocks reduces when markets are not performing well, like in the last one year, and hence cash trading turnover has remained muted.

Cash or equity segment has two types of participants - investors and intraday traders. While the volatility over the last year should have meant higher equity intraday trading volumes matching that of F&O, there have been regualtory changes in the last couple of years that has gotten active traders to prefer derivative segment over cash.

Traders preferring F&O to Cash.

Starting Dec 2020, SEBI capped the maximum intraday leverages a brokerage firm could offer their customers. Until then, a broker could potentially give unlimited leverage. By this, I mean if you had, say, Rs 1000 in your account, a broker could allow you to take positions worth, say, Rs 1lk (100 times leverage) for intraday. As you can imagine, the more leverage, higher the turnovers on the market. Traders love leverage; the higher the leverage higher the potential returns and, of course the losses as well.

While most online larger brokers had some cap, the smaller to mid sized brokers allowed leverage based on relationships. Brokers used leverage to make up for a not competitive product and attract active traders, who tend to be the highest revenue generating customers. The maximum leverage a broker could offer was capped at 20 times in Dec 2020 and slowly reduced to 5 times from Sep 2021.

As an intraday trader in cash segment, you have restrictions like having to square off positions by 3.20 pm and inability to carry short positions overnight. With the leverage offered for intraday stock now reduced to the same levels as the F&O segment, trading on F&O is a much better product.

For those who trade larger quantities of intraday stock, futures or short option positions are better. Leverage is the same; trades dont’ get auto squared off at 3.20 pm, short positions can be hold overnight.

For those who trade smaller quantities of intraday stock and can’t afford to post the full margin required for trading the minimum one lot of futures or short option position, buying options would seem like a better product. Buying options also gives much higher leverage, paying a small premium, which can get a large contract value exposure.

So, apart from markets being flat, the reason why derivative turnover is outperforming cash market turnover is also because active intraday traders in equity segment now preferring F&O.

Activity trends by participation.

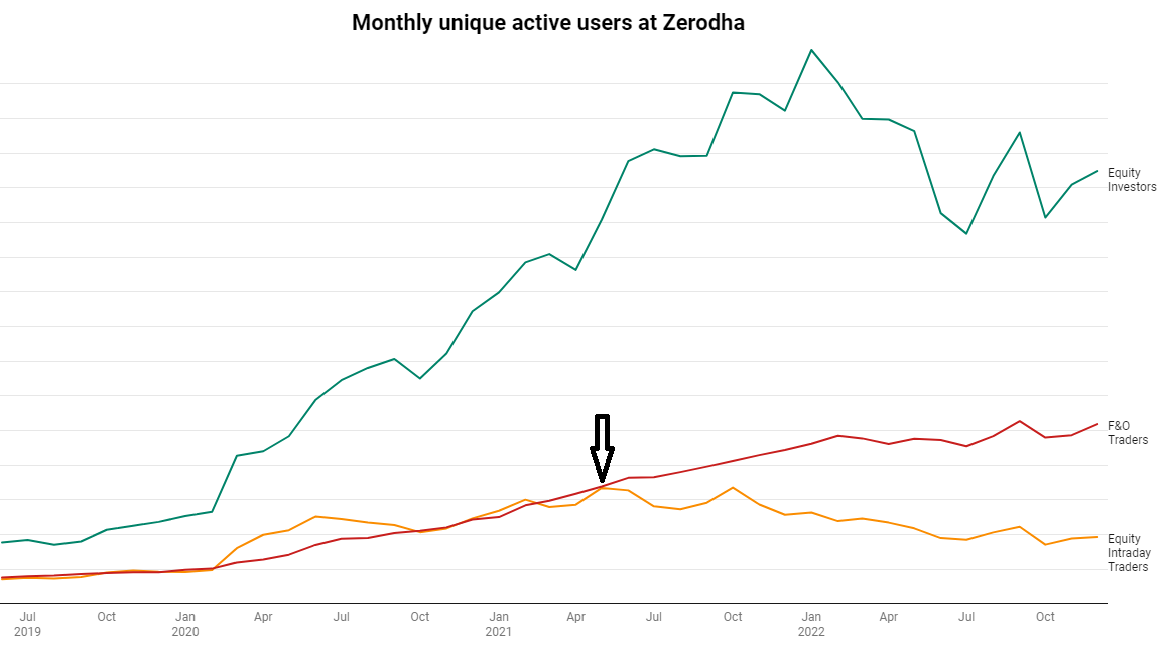

If we have to go down the path of figuring out the retail market participation trends, I think the right way to do this is by looking at the number of participants and not just the trading turnover. Exchanges and regulators don’t publish this data; here is what has happened at Zerodha. Since we are ~20% of the overall retail participation in India, this is quite a large sample size to help come to conclusions.

Monthly unique customers who have traded on the platform

If you were to look at the above graph, equity investor participation has grown significantly more than F&O trading in terms of participation in the last three years. The bump up we see from 2021 in F&O participation is also because of the drop in equity intraday trading participation. This, as I mentioned earlier, is most likely due to leverage restrictions on equity intraday trades, which makes trading on F&O a better product than trading in equity for anyone looking to trading with leverage.

Higher contribution from retail to derivatives segment.

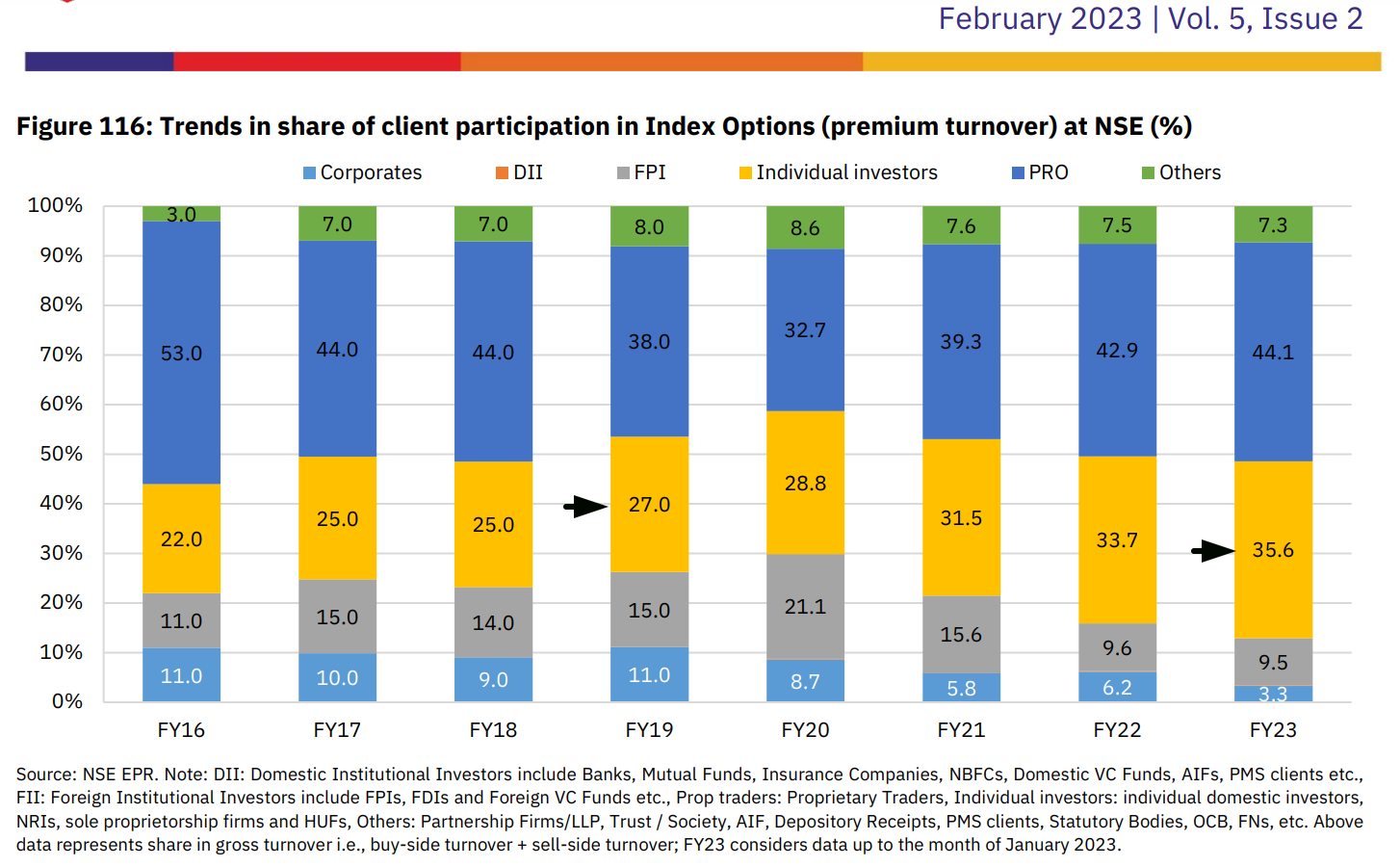

One of the other points that also gets highlighted is how retail trading contribution in derivatives segment and especially the option trading segment, has increased significantly in the last three years (since COVID). Check this image from NSE market pulse, which shows a jump from 27% to 36%.

I think this jump is again due to regulatory reasons. In March 2020 when Covid unleashed volatility in the capital market, SEBI, as a measure to contain risk, introduced open interest (OI) restrictions at entity level. The maximum OI at any entity level is Rs 500 crores worth of positions or, say, around 6000 lots of Nifty. While no retail investors would ever hit this limit, many institutions and prop shops were capped in terms of position limit, so their trading activity has been capped. This maximum OI limit is why I think retail percentage contribution has gone up. This will see a drop whenever the Rs 500 crore OI limit at entity level are increased or removed.

Money at play - equity vs derivatives.

Another way to compare participation trend is to compare the actual money at play. Which is, what is the total money being used at any point of time for taking F&O positions, and how does it compare to the total money used for equity positions.

At Zerodha, if you compare the total money utilised for F&O at any time and compare it total value of stock holdings, it is now ~3%. This percentage has reduced for us over the last few years and significantly.

So…

Yes, trading in F&O has picked up, but not disproportionately, as it is made out in mainstream media. Yes, F&O participation has increased, but equity has increased much more.

Trading in F&O is mostly from active traders who trade irrespective of if the markets are in bull or bear markets. Comparing this turnover to cash market turnover, where the market’s direction significantly determines turnover, isn’t a right comparison. A lot of trading has also moved from trading intraday stocks in cash segment to index F&O segment, which necessarily isn’t bad for the trader since indexes are a much safer product to trade as compared to stocks. This move has mainly been because of regulatory restrictions regarding maximum leverage on intraday trading. The increasing retail contribution in overall derivative segment again is due to restriction in maximum open interest affecting institutions and prop shops and not retail traders.

But yeah, let me add a disclaimer, F&O trading, especially option buying, is extremely risky. We had shared a bunch of things to keep in mind when buying options.

I guess the answer above should help you figure this. You can also check the NSE market pulse that I have linked above. But yeah, be mindful of not getting misled just by caring about trading turnover.

The deeper the pockets, lesser the churn. Also institutions aren’t like retail, mostly taking directional bets. Institutions are also hedging and arbitrageuing, lesser risk and hence higher longevity. But the Rs 500 crore restriction means institutions can only do so much in the markets today.

Yeah, enough option sellers. India has many prop shops doing arbitrage, so anytime demand picks up option buying, and if the price moves far away from theoretical price, there is an arbitrageur who will ensure it doesn’t go off whack.

All the regulations that had to change around this have already changed. Unlikely that anything new will affect, apart from any product suitability framework that makes it hard for most retail traders to participate. The derivative markets will collapse without the retail traders who provide constant liquidity. We can see this in many single stock derivative contracts with no retail participation and hence no liquidity.

As a broker we have been trying to educate and nudge customers to follow money management rules when trading options. We are trying to incorporate some of these within the platform. Things like blocking the account at a specific loss defined by customer, not allowing ovetrading or exposure beyond a specific value set by the customer, etc. Following basic money management rules is the best way to increase the odds of making profits while trading derivatives.

Only a tiny percentage of folks return if they have stopped F&O trading completely. The big problem is when people lose; many start throwing good money at bad money and stop only when they run out of resources or if the losses are too significant. Not everyone should be trading F&O or even the markets actively. I think the biggest stoploss every trader needs to have is on trading itself. We plan to actively dissuade people coming back to trading F&O if they haven’t been successful. Nudge them to get into lower risk investing type of products.

In India the stock lending and borrowing market isn’t very active. So the only way for traders to take short positions is through the derivative market. This is the reason why trading in F&O seems much larger as compared to other markets. This can potentially change when activity in SLB picks up.

Naked option buying works !!! Only if one buys and holds it till expiry it looses all the time value in price. But that is not what profitable option buyers do.

Those who trade intraday breakouts and momentum get in and out quickly. The time value loss is negligible or non existent.

Those who are trend followers like me turn time value loss in to an advantage. Trend follower accuracy is less than 50%. Everytime we lost, we lost less because of the time value cushion in the option premium. As we lose more than we win, theta decay incurred in a winning trade gets counter balanced by lesser losses in the losing trades. Also if one is a positional trader option buying caps max loss when market gaps against the position held.

Besides in general anytime, anything can happen in the market. Long options inherently limits the max risk.

Trading is a simple game of chance, associated risk-reward and capital adequacy. When trading (option buyer or seller) one has to keep adequate capital for the system (Capital is not the amount deployed for one trade. Its that amount that will allow one to trade the system over a fair amount of time and which can absorb system drawdowns comfortably for a certain position size.)

Traders are still paying option premium, which has increased 2.5+ times since FY21. Is the premium turnover too concentrated with these 10% very active traders? I am guessing that it will be more distributed.

What is the profile of these very active traders majorly [not sure what you can share here]? But is there a significant overlap in this 10% with the 10% of F&O traders in India who are not making losses?

In the chart with # of unique clients - the blue line is intriguing, will the churn of equity delivery customers seen in the last 6 months continue? What do you think?

Unlike in equity, where volumes come from investors (large numbers but small volume) and active traders (small numbers but large volumes), those who trade options are mostly active traders in the markets. So yeah, you are right; the turnover is more distributed within options.

But the business is very concentrated on the institutional and prop shop side. 10 of them could be as much as 30% of the market. These are HFT (High frequency trading) firms and arbitrage shops leverating technology to trade.

This is a tough one. The very active traders come across different backgrounds—those who trade full time for a living to those doing parttime like CXO’s, Doctors, software professionals, and many more. In many cases, trading also happens in the name of wife, parents, etc., for tax planning purposes, so you can never truly say what the profile is.

Equity delivery customers don’t stop trading like F&O customers when in a loss. Many return to try averaging the existing holdings if they are losing or buying some other stock. Also, as an equity delivery customer, time is in your favor; if you hold for enough time, even a lousy trade could potentially turn profitable. Also, psychologically, a loss isn’t a loss unless it is realized. In F&O and intraday stock trading, your loss is realized immediately, but you can delay it in equity.

But everything said, what matters is what is happening to equity as an asset class. Over the last many years, equities have outperformed fixed income and real estate, so there has been so much interest in the markets. But as the markets have started underperforming fixed income (FD’s inching up to almost 8%), many will question if they should invest in the markets vs fixed deposits. So the chances of those who have stopped equity delivery to return will be primarily based on whether equity outpeform fixed income going forward or not.

She works at Accel and had emailed me these queries. Coincidentally I wanted to write on this topic with all the noise around how derivative trading is growing and equity dropping. So I requested her to post the query here so that the discussion is helpful for the community.

Yup , I second that @viswaram .I have checked ATM straddle price, its actually significantly dropped around 20% ( compared with % of Spot and correlated with VIX). I feel either less people are buying or Options writers have increased( feels like the increase in option sellers). Might be she meant Increase in Option turnover?

@nithin do you think that option volumes in index will continue to rise in future from the current level given the reduced leverage across other derivative segments?

One final question from my side - do you think a significant portion of new F&O traders would have churned out already in the last two years ? And if I consider unique demat account holders as a ceiling then it is unlikely that we see disruption in number of consistent F&O traders in the country going forward. Activity can however continue to depend on multiple aspects.

Tough to say if option volumes will go up or not, since it is dependent on what happens with market direction and volatility. Which is impossible to call.

But one thing is for sure, given everything remains the way it is, option trading volumes will continue to be as high or higher as compared to equity intraday trading volumes. While most people getting started trading will still start as equity intraday traders, they will most likely shift to F&O given all the advantages.

Equity delivery volumes is a factor of market direction, again tough to call.

Typically a person starting trading in the markets does by first investing or equity delivery. A few of them discover intraday trading stocks and the ability to make money being short. And given enough time, most intraday stock traders discover and start trading F&O.

Since in 2020, the influx of people getting started investing was so high, it led to many attempting F&O. So unless we have another period where there is a sudden rush of investors to the market, unlikely that F&O trading activity in terms of participation is going to pick up in the future. As a business we are bracing ourselves for a period where we think F&O trading activity will reduce. The logic is the same, if new investors aren’t adding at same speed and existing F&O traders are stopping, the F&O business slowly and steadily will reduce.

There is a problem here. In my opinion, a large sample size is not necessarily a good sample size for this example.

Because F&O traders might be attracted to competitive brokerage charges, especially new entrants. Most of these new participants in the F&O segment are possibly with other brokerage houses that provide cheaper brokerage fees.

So if we take a sample of data from another broker with cheaper brokerage fees compared to Zerodha, the proportions of segment participation might vary significantly in their sample, and hence the conclusions put forward here might be subjective.