There are some parameters that affect the pricing of Options. Some of them are changes in spot and strike price. While others are velocity and time of expiration. But how does Interest rate effect options pricing.

1 Like

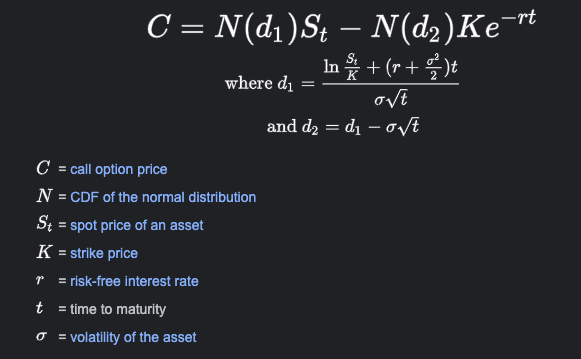

r in this case is the interest rate.

2 Likes

Can you please explain it little further, because as far as I can have heard risk free rate are those rate at which government securtites are traded. But how does that impact in pricing of the options?

This explains pretty much every aspect of option pricing formula.

For all practical purposes (as retail) this can be ignored as the options have already been priced based on the prevelant rate. This is explained in some detail here as well: Option Maths and Markets

Given the above, I am guessing you have some different use-case in mind which I could not infer from the question.

1 Like

Hi,

For the sake of convenience, let us take the example of a person who wishes to execute an arbitrage strategy by transacting in the spot and derivative segments. Say, he does this by buying the underlying security in the spot market and buying a deep ITM put option, the delta of which, is assumed to be virtually close to -1 throughout the duration of the contract.

Now, since the risk involved in the arbitrage strategy (based on the given assumptions) is more or less equivalent to the risk involved in a risk-free bond, theoretically speaking both the strategy and the investment in the bond should yield the same returns.

In other words, the put option would be priced such that the person in question would be indifferent to the arbitrage strategy and investing in the bond.

This is of course, a hypothetical scenario and a very crude way to explain the impact of risk-free interest rate in the pricing of options. I have basically tried to keep it as simple as possible, by ignoring all the other variables affecting the price of an option and various other factors, but hope you get the gist.

[This was how I had understood the concept of risk-free interest rate in the context of option pricing and I may very well be wrong.]

And yeah, goes without saying, it pays to go through the material referenced in this thread as well as Zerodha’s Varsity.

1 Like

Thank you Joyesh.

You have explained it perfectly. Thank you Pratist.