To trade derivatives exchanges ask for margin = SPAN + Exposure

Until now exchanges would charge a short margin penalty only if the margin in clients trading account went below the SPAN margin required to trade derivatives. The penalty could go up to 5%.

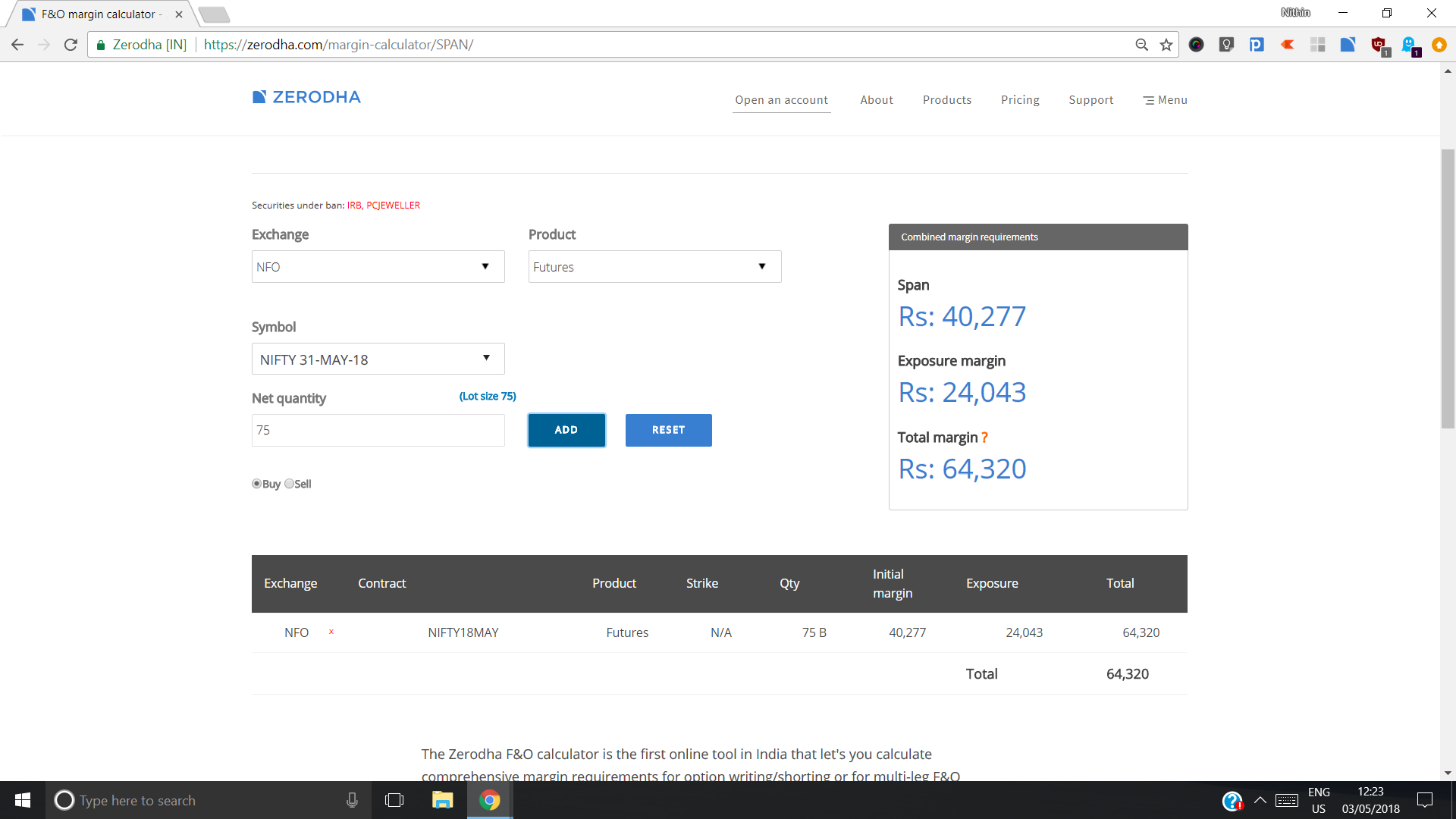

For example, below is the margin for Nifty futures. Exchange penalty would have been applicable only if funds in client account went below the SPAN margin of Rs 40k. Going forward from June 1st, a client is required to have the total margin of Rs 64k to continue holding a derivative position overnight without having to pay the short margin penalty.

More margin collected would mean lesser risks in the system overall - both for brokerages and exchanges. This is especially important when incidents like PC Jeweller, Satyam, etc happen - when stocks suddenly can move up and down significantly. If the broker hasn’t taken sufficient margin, he can become a systemic risk.

Some brokers used to ask for SPAN +Expo (us included) to take new positions, some weren’t. This new regulation will now mean that everyone will have to follow the same rule. Which is good for the industry. Leverage generally isn’t good for anyone’s health.

Con’s

Short margin penalties are bound to go up significantly until everyone is used to this new regulation. Not all traders are capitalized enough to continue holding onto positions overnight with SPAN+Exposure currently. The industry will take to adjust. In the interim, a world where we are already paying STT, GST, etc., this will just add to the costs of a trader.

Most mid to small sized brokerage firms used to allow trading just using SPAN margin. Since now even the exposure is required, volumes might drop in derivatives, especially single stock F&O. Especially more considering this is coming after SEBI had already increased the lot size last year.

How does it affect traders?

Until now you would be charged a short margin penalty if the money in your trading account was lesser than the SPAN margin amount. From June 1st, this penalty will be applicable if the margin in your trading account is lesser than SPAN + Exposure. So make sure to square off your positions.

How does it affect traders using Zerodha?

We have anyways been collecting both SPAN + Exposure margin. So this wouldn’t really affect any of you. But until now our RMS team might have allowed you to carry forward position to the next day if you were short SPAN+Exposure by a small amount, but going forward they will have to be stricter and square off positions before the close of the day if there isn’t the complete margin in the account.

Thanks so much @nithin.

As Zerosha already charges us SPAN and EXPOSURE for CF positions, even before the circular, this means that the circular will not affect Zerodha customers to have more margin, as we already keep this margin for CF. Please confirm.

Also, not sure about the circular limited trading based on income. If we maintain SPAN+EXPOSURE, are we fine to trade and CF as many FNO as we want without bothering about the income shown in ITR statements?

SEBI actions impact Future traders & Option writers , If stock options made American style , will hurt, Option writers the most. At the same time because of high margin , probably some of the "Long on " Future traders turn to buying option premium , i assume option buyers will have some advantage and also i suspect SEBI is targeting option writers.

Thanks for your detailed clarification. I have a few further questions here.

Lets say I need a total margin of Rs. 50000 (SPAN + exposure) to write one lot of nifty option and I have Rs. 55000 in cash, and then I take the position (NRML).

Now because of some reason (possibly increased volatility), the total margin requirement shoots upto Rs. 60000 at some point (after I took the NRML position), now will the RMS square off the position immediately, or will I have time till the end of the day to arrange for the shortfall of Rs. 5000?

In the above case, in case I manage to arrange for the additional margin on the SAME DAY, will I still end up paying penalty for margin shortfall?

Let us say NIFTY spot is at Rs. 11000, and I wrote an option of 10500 PE an bought option of 10300 PE. Suppose nifty spot suddenly crashes to 10200, and my short put position is deeply ITM, will the RMS square off the position? Now that the exchanges have mandated the broker to maintain exposure margin, how will I be affected in this scenario?

Since this position is a credit spread, I would want to square off both trades at the same time, but then if RMS squares off only the short PUT and leaves the other position open, then I could be at big risk if the market reverses direction instantly.

It would be good if you can throw some light on this, as your insight will be helpful for other traders as well.

Till 3 PM one will have time to bring in additional margin.

No.

Ideally RMS may not close as marking to market of profits/losses is not there for options but can’t guarantee if there are multiple hedge positions and margins are increased on shorting side. Also it would be difficult to analyse each and every position at the time of closing. One may also get some additional margin benefit if the positions are fully hedged from exchange. But it is recommended to have full margin at all times when trading especially in spread positions as if one position is closed we may end up with open directional trade. RMS will close future if one leg is long future and other leg is long put option and making loss in future even if put is making money as futures are settled daily but options are not.

Ok. So the circular is about “Additional Risk management measures for derivatives segment” where they have made all kinds of margin collection compulsory but haven’t mentioned any changes to the source of the margin which can be free cash or collateral margin. So I am hoping the rules for it remain the same, i.e. shortfall (less than 50% free cash) for overnight FnO attracting 0.05% per day interest … But that is it. After all it allows you to go almost 2X from risk mgmt. perspective.

Those rules remain the same but clarification is needed from exchange if losses can be reported using collateral or only from cash for collateral clients.

Suppose if I purchase option stock for 15,000 INR and if i keep it for 3 days or more, do I need to have additional 15,000 INR in my account ? Please clarify on it.

Received this message-

Starting tomorrow, you have to maintain full margin, i.e., SPAN + Exposure, to carry forward F&O positions. Not maintaining adequate funds could result in a system square off or an exchange margin penalty. Read more here.

or is there a broad category in that circular which includes it to calculate risk appropriately?

or is there a broad category in that circular which includes it to calculate risk appropriately?