Update 31st May: SEBI postpones applicability of this circular by a month to July 2nd from June 1st.

To trade derivatives exchanges ask for margin = SPAN + Exposure

Until now exchanges would charge a short margin penalty only if the margin in clients trading account went below the SPAN margin required to trade derivatives. The penalty could go up to 5%.

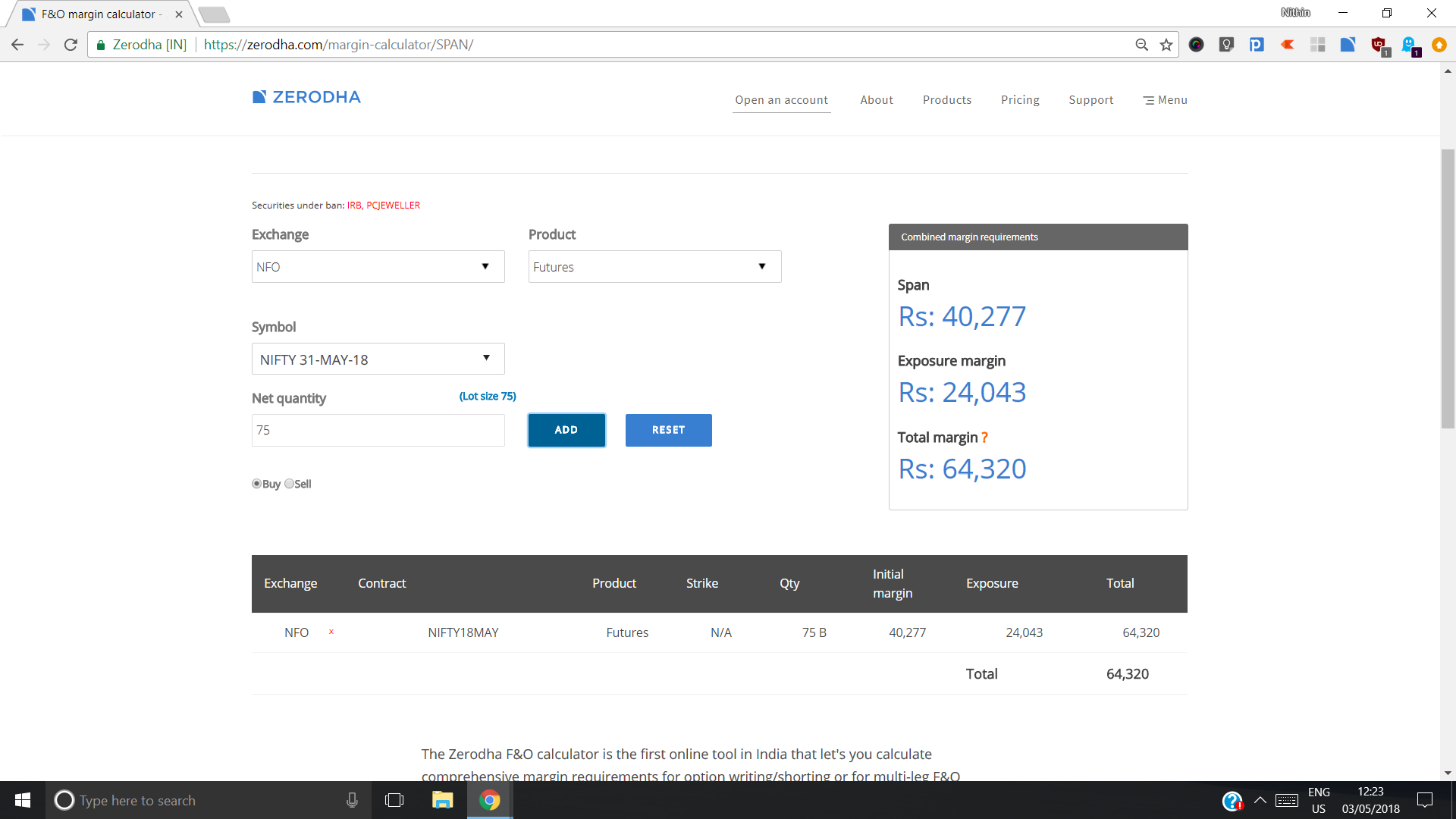

For example, below is the margin for Nifty futures. Exchange penalty would have been applicable only if funds in client account went below the SPAN margin of Rs 40k. Going forward from June 1st, a client is required to have the total margin of Rs 64k to continue holding a derivative position overnight without having to pay the short margin penalty.

Pro’s

-

More margin collected would mean lesser risks in the system overall - both for brokerages and exchanges. This is especially important when incidents like PC Jeweller, Satyam, etc happen - when stocks suddenly can move up and down significantly. If the broker hasn’t taken sufficient margin, he can become a systemic risk.

-

Some brokers used to ask for SPAN +Expo (us included) to take new positions, some weren’t. This new regulation will now mean that everyone will have to follow the same rule. Which is good for the industry. Leverage generally isn’t good for anyone’s health.

Con’s

-

Short margin penalties are bound to go up significantly until everyone is used to this new regulation. Not all traders are capitalized enough to continue holding onto positions overnight with SPAN+Exposure currently. The industry will take to adjust. In the interim, a world where we are already paying STT, GST, etc., this will just add to the costs of a trader.

-

Most mid to small sized brokerage firms used to allow trading just using SPAN margin. Since now even the exposure is required, volumes might drop in derivatives, especially single stock F&O. Especially more considering this is coming after SEBI had already increased the lot size last year.

How does it affect traders?

Until now you would be charged a short margin penalty if the money in your trading account was lesser than the SPAN margin amount. From June 1st, this penalty will be applicable if the margin in your trading account is lesser than SPAN + Exposure. So make sure to square off your positions.

How does it affect traders using Zerodha?

We have anyways been collecting both SPAN + Exposure margin. So this wouldn’t really affect any of you. But until now our RMS team might have allowed you to carry forward position to the next day if you were short SPAN+Exposure by a small amount, but going forward they will have to be stricter and square off positions before the close of the day if there isn’t the complete margin in the account.