Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the videos on YouTube.

In today’s edition of The Daily Brief:

- Indigo smashes past $10 billion revenue mark

- Where electric vehicles are in 2025: And where India sits

Indigo smashes past $10 billion revenue mark

At the moment, India’s listed aviation space might as well be synonymous with a single behemoth: Indigo Airlines. The company controls nearly 65% of all Indian aviation — nearly 25 times that of its only listed rival, Spicejet.

This is why, to us, understanding how Indigo works is central to understanding India’s aviation industry.

Airlines are a famously tricky business to run. Aircraft fleets are staggeringly expensive to maintain. A lot of those costs stick around, whether or not a company has passengers to cater to. You can’t really cut corners with aircraft maintenance; risking a plane crash is simply not an option.

Meanwhile, no airline is guaranteed passengers. No matter what an airline does, unless people have an extraneous reason to travel, they just won’t buy a ticket. And so, to a great extent, an airline’s sales are not driven by its own policies, but by the broader economic climate around them.

Their business is also constantly hit by all sorts of factors that lie outside its control — from oil prices, to pandemics, to the outbreak of war. Regulators, too, monitor the sector closely and intervene often, because no government wants to risk a single aircraft failure. Once again, these create risks that a airline company has no control over.

In essence, if you’re running an airline, you’ve to put gigantic sums of money on the line, and whether you’ll recoup those sums is outside your control. That’s why so many airlines across the world go bankrupt so often. In this business, there’s really just one option you have: put your head down, run your operations as smoothly as possible, and hope for the best.

That’s the game that Indigo’s playing. And to us, at least, it looks like it’s playing the game rather well.

How Indigo’s quarter went

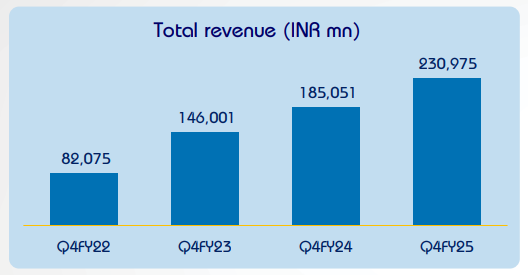

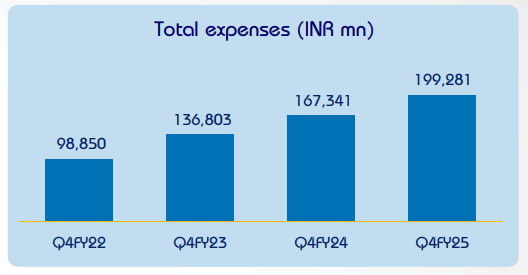

The quarter gone by was an exceptional one for Indigo’s business.

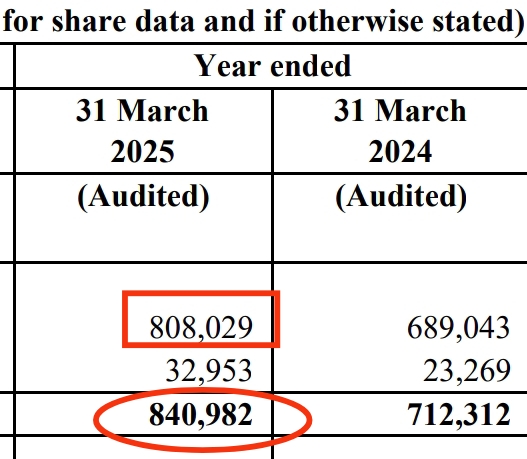

The company’s revenues for the quarter went up by nearly 25% over the same quarter last year.

Its expenses, meanwhile, rose much slower: by 19.1% year-on-year.

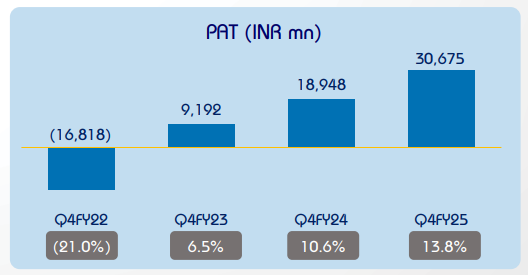

In other words, the company posted much better margins this quarter. Its EBITDA margin went up to 27.5% in Q4, compared to 22.4% last year. This was quite a leap, and that showed up in the company’s earnings. Indigo’s EBITDA went up by a giant 59% year-on-year. And with that, the company’s net profit shot up by nearly two-thirds within the space of a year — from ₹1,895 crore to ₹3,068 crore.

This capped off a great year; for the first time ever, the company’s total revenue over the year broke past the $10 billion mark.

What’s behind this performance?

For one, the company’s just growing its business.

Indigo added more aircraft to its fleet (434, against 367 last year), and it ran longer routes. Airlines usually count both together in something called “Available Seat Kilometers” — or ASK: the number of seats, multiplied by the number of kilometers they’ve flown. Indigo improved its ASK to 42.1 billion in Q4 FY 2025, compared to 34.8 billion last year.

It also managed to fill most of these new seats. Indigo boasted a ‘Passenger Load Factor’ of 87.4% over the quarter — an improvement from last year’s 86.2%. Roughly speaking, that means 87.4% of its seats were occupied over the quarter.

In short, the company’s margins, to a great extent, are just a result of it running a tight (air)ship. But, with that, it also caught some lucky breaks.

For one, oil prices fell over most of the year, and Indigo pocketed most of the gains. It was paying ₹1.60 per-seat per-kilometer in fuel, compared to ₹1.76 a year ago. Sounds like a minor shift, we know, but those savings can add up.

Two, this quarter featured a once-in-a-decade gathering — the Mahakumbh — with its 66 crore attendees. It also saw the upside of a longer wedding season.

Zooming out, there’s also a longer-term trend that has helped the airline soar: fewer grounded aircraft . This is a problem that has haunted the airline for the better part of a decade. Back in 2016, Indigo inducted a series of A320 Neo plans, which featured Pratt and Whitney engines. Those engines, however, weren’t up to the mark: and started seeing serious failures. Airlines all over the world — Indigo included — were forced to ground their fleets as they scrambled for answers. Finding new airplane engines, however, wasn’t easy — and became much more difficult as all operations stalled during the pandemic. To get by, Indigo had to lease aircraft, which sent up its costs.

The problem peaked early in 2024, when it was forced to confine more than 70 planes to the ground. But slowly, things have been improving. Nearly half of its grounded aircraft are now back in action, and with it, the company’s able to shed its leasing costs.

Is Indigo premiumising?

Indigo is famously a low-cost carrier . That is how it first made its mark in an industry that featured ‘full-service’ carriers like Jet Airways and Air India.

Only, it looks like the company’s slowly moving to slightly premium offerings. Over the last year, it launched a loyalty program, “BlueChip”. It also began something resembling a business class — ‘Stretch’ — with complementary meals, better baggage allowance, and nicer seats. It has started running wide-body flights over an ever-increasing list of international routes: moving away from its staple fare of no-frills narrow body aircraft.

In other words, after surviving a market that saw a steady parade of full-service carriers crashing out, Indigo is slowly starting to look like those that it replaced. So what gives? Is Indigo pivoting to a new strategy?

For now, the company insists that’s not the case. The company stands for lean operations, not sub-standard products, and that continues, as its management clarified:

“I think you should make a difference between ‘low cost’, and ‘low cost operations’ or a ‘low cost basis’ if you wish. And I think IndiGo prides itself — and we remain committed to that — to be an operator with a very low cost basis. That has not meant domestically that we’re having a product which is not high quality. ”

Perhaps. It’s interesting, nevertheless. The company is experimenting with a new sort of game, and we’re curious to see how it goes.

The geopolitical question mark

If you’re following the airlines sector, though, you’re probably as interested in what happened after the quarter as you are in Indigo’s quarterly results themselves.

After all, once Pahalgam was hit by terror attacks, the India-Pakistan tensions that followed threw up serious challenges for the airlines industry. Tourism took a sharp hit as tensions began to boil. Pakistan, meanwhile, shuttered its airspace. And then, once May rolled around, the two countries started exchanging blows. Within the space of a single month, a large chunk of the sub-continent turned into a big no-fly zone.

How does an airline company see this sort of a situation?

Right from April 22, when the attack took place, Indigo saw a wave of cancellations. Soon afterwards, Pakistan’s airspace closed up. The company had to suspend flights to two cities — Tashkent and Almaty — while for 34 routes, it had to go all the way around Pakistan. That added 20-30 minutes to flight times, and drank up more fuel. As tensions increased, in May, it had to suspend operations from 11 airports in North-western India. 170 flights were cancelled. In the meanwhile, its staff had to placate customers that were distressed by this entire situation.

In essence, briefly, the conflict threw the company’s operations in jeopardy.

But that’s where diversification comes in. Indigo flies thousands of flights a day, in regions all across India and abroad. Some of that business was affected by the situation. But the lion’s share of its operations went on as usual. And a month on, things have already started getting back to normal.

There are some minor tremors, still. Indigo’s long-standing partnership with Turkish Airlines, for instance, has suddenly come under question, after Turkey clearly took sides in the recent flare-up. The bottomline, though, is that things are quickly coming back to normal.

Soaring amidst turbulence

For all the chaos baked into the airline business — from unpredictable demand to black-swan geopolitical shocks — Indigo apears to have found some sort of rhythm. It’s running tight operations, flying more passengers farther than ever before, and making more money while doing it.

It isn’t immune to trouble, of course — the recent flare-up in the subcontinent is proof enough of that — but it does suggest something deeper: Indigo’s business seems robust enough to take a hit, adapt, and keep flying.

Where electric vehicles are in 2025: And where India sits

Yeah, we know, we’ve been going on and on about the green transition. But bear with us, because there are just too many rabbit holes to dive into.

See, the International Energy Agency’s Global EV Outlook 2025 just dropped, and there’s a lot to unpack here. Electric vehicles are turning mainstream across the globe, though at dramatically different rates, depending on where you look. We’re at the very beginning of an exploding market, and a country-wide infrastructure build-out. But that will only materialise if we fix a range of issues; and if we don’t, there’s a very real risk of falling behind in a new technological revolution.

There’s a lot happening, so let’s dive right into it.

The global EV landscape

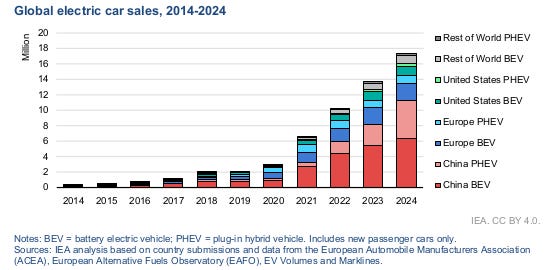

Electric car sales shattered records in 2024, exceeding 17 million vehicles globally. Think about this: in 2024, 3.5 million more EVs were sold across the world than in 2023. That difference, aline, is more than the total number of electric cars sold worldwide in 2020. That’s what exponential growth looks like in action.

China continues to tear through this space. Out of nowhere, its electric cars have come to account for almost half of all cars sold there in 2024. Get this – the over 11 million electric cars sold in China alone last year are more than global sales just two years earlier. They’re well on their way to electrifying their entire fleet — one in ten cars on Chinese roads is already electric.

Europe’s growth, on the other hand, has stalled. Its subsidy programs are waning, though the market share of electric cars is holding steady at around 20%. Meanwhile, in the U.S., electric car sales grew by a healthy-but-not-revolutionary 10% year-on-year. More than one in ten cars sold (but not in total) in the United States in an electric vehicle.

Where does India stand in this global picture?

Our electric car sales approached 100,000 in 2024, representing about 2% of our domestic car market. While that might seem modest compared to China or Europe, it’s important to remember that our EV journey is still in its early stages, and the growth rate is accelerating. In fact, in just the first quarter of 2025, India’s electric car sales grew 45% year-on-year , reaching nearly 35,000 units.

Across the world, the electric vehicle market seems bound to continue this boom.

In 2025, global electric car sales are expected to exceed 20 million — more than one-quarter of all cars sold worldwide. China is projected to reach an electric car sales share of around 60% this year, with Europe second at 25%. In India, too, we could see our electric car sales share reach nearly 15% by 2030. That’s a major increase from today’s levels, though still less than what’s projected for other major markets.

Does an EV fit your budget?

So why are we seeing such different adoption rates around the world?

A lot of it comes down to affordability .

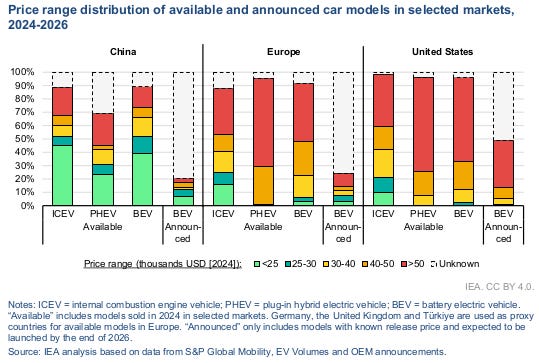

That’s why China is so fascinating . In 2024, about two-thirds of all electric cars sold in China were priced lower than their conventional equivalents — and that’s without counting purchase incentives. Chinese manufacturers have driven down costs through intense competition, and this has turbocharged adoption — even as government incentives have decreased.

Europe’s different. In Germany, for example, the average battery electric car price remained 20% higher than that of conventional cars. This price gap, combined with the phase-out of subsidies, has dampened sales.

The United States faces even steeper challenges. Battery electric cars are still 30% more expensive than conventional vehicles. This persistent price gap is hurting prospects for future growth.

India, too, has a similar gap — though it’s coming down. In 2024, the average price premium of battery electric cars in our market fell below 15% for small cars and 25% for SUVs. This is a significant improvement. Just a couple of years ago, they were priced at more than double their conventional counterparts. We’re taking our time with this transition. Instead of relying heavily on Chinese imports like Brazil or Thailand, we’re trying to take a more self-sufficient approach. We have high tariffs in place for EVs. We’re trying to nudge more such domestic capacity through PLIs on cars, auto components, and batteries.

Is that working? Maybe. At the very least, India has managed to come up with a range of battery electric car models priced under USD 20,000. That’s an accessible entry point for middle-class Indian consumers. The share of Chinese imports in India’s EV sales, as a result, have remained below 15%.

You can’t talk about affordability without talking about the total cost of ownership, of course: purchase price isn’t the only thing that matters; maintenance, fuel, and other operating costs matter too. This is particularly important for commercial vehicles like trucks and buses — where people are more likely to look at costs over the entire lifecycle. This is particularly relevant for India, where fuel costs can be exceptionally high. By 2030, electric buses in India are expected to reach a 25% market share, supported by government initiatives like the PM e-Bus Sewa scheme, which aims to deploy 38,000 electric buses across the country.

Heavy-duty electric vehicles

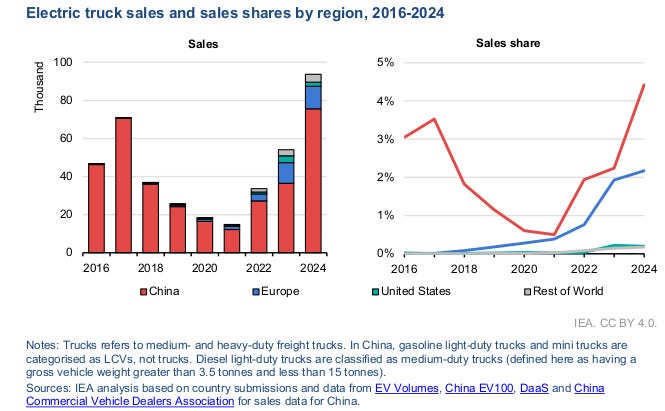

With that, let’s look deeper at what’s happening in the heavy-duty segment. Globally, electric truck sales grew by nearly 80% in 2024, and now makes up close to 2% of total truck sales.

No prizes for guessing who’s leading this charge. It’s China, of course . Their electric truck sales doubled to 75,000 vehicles last year, representing over 80% of global sales.

Not everyone’s doing that well. In Europe and the United States, electric truck sales remained relatively flat in 2024. However, in these regions, the number of available models is rising – we’ve gone from fewer than 70 battery electric truck models in 2020 to more than 400 today, which can meet a far wider range of applications.

In India, the PM E-DRIVE scheme, which replaced the earlier FAME-II initiative, allocated INR 5 billion (USD 58 million) specifically for purchase incentives for electric trucks. This was perhaps necessary: electric truck sales actually declined in 2024. Hopefully, this new support will to revitalize the segment. Whether it actually does, only time will tell.

But where India is making progress is in the electric bus sector. Our electric bus stock has increased dramatically — from less than 3,000 in 2020 to more than 11,500 by the end of 2024. We’ve talked about this before.

But there’s one thing that’s hard to deny: these numbers are nowhere nearly as great as those for cars. The economics of electric heavy-duty vehicles, it turns out, are very different from light-duty ones. They’re much more expensive upfront, for one — a battery electric heavy-duty truck costs two to three times more than an equivalent diesel truck in major markets. If you’re operating a business with thin margins, that’s a no-go.

Over a long time, though, greater efficiency and lower energy costs make battery electric vehicles more attractive the more they’re used. By 2030, battery electric trucks in Europe and the United States are expected to reach parity on total cost of ownership with diesel trucks for long-haul operations. They’re already there in China.

So it’s a mixed picture: if you have the cash to take an upfront hit, you’ll break even over time.

Chinese manufacturing goes global

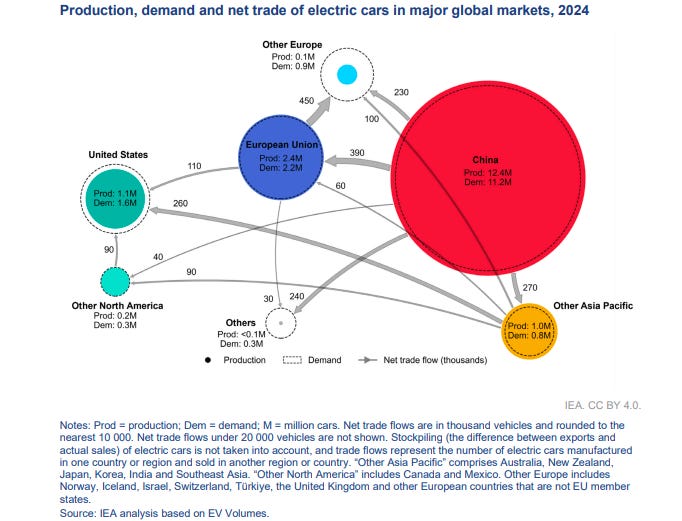

One of the most significant developments in the EV market, off late, is how Chinese manufacturers are responding to mounting trade restrictions, by expanding their manufacturing footprint overseas.

See, in 2024, multiple regions introduced new tariffs on Chinese electric car imports. The European Union imposed countervailing duties on Chinese battery electric car imports. The United States and Canada implemented tariffs exceeding 100%, with further increases slated for 2025. Markets that were recently receptive to Chinese imports, like Mexico and Brazil, have also approved tariff hikes.

So what did Chinese automakers do? They started building factories abroad, to give them a new foothold to export from. By 2026, Chinese overseas manufacturing capacity is expected to almost double, to reach over 4.3 million vehicles per year.

Europe and Southeast Asia are the primary locations for these new assembly plants. By 2026, almost half of the total Chinese overseas manufacturing capacity will be located in Europe.

We’ve spoken already about how we, in India, are attempting self-reliance instead. But EV manufacturers that commit to invest in India can import electric cars with much lower duties — reduced from 70% to 15%. That’s pulled in some Chinese manufacturers, getting them to team up with Indian industry.

In 2024, for instance, the JSW Group signed a joint venture with China’s SAIC Motor to work together on car production under the ‘MG Motor’ brand. About half of the electric cars sold by MG in India are now produced domestically. The other half are imported from China. By the end of 2024, JSW announced the launch of its own EV brand, and it’s discussing technology transfer from partners like BYD and Geely.

Will this help us develop an entire supply chain domestically? Or will this simply draw us closer into China’s orbit? Only time will tell.

Two and three-wheelers

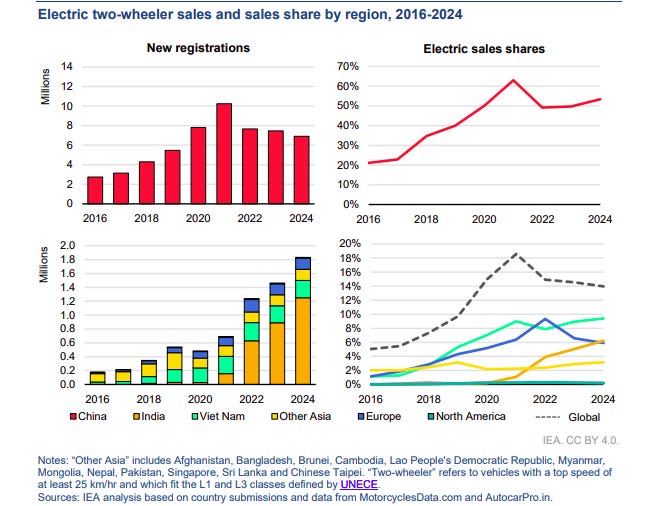

A very small part of India actually drives cars . Two-wheelers are our primary mode of transportation, accounting for over 80% of vehicle sales. This is where India’s EV transition is truly shining.

That’s also true elsewhere in the world. Two and three-wheelers remain the most electrified road transport segment globally in 2024, with more than 9% of the global fleet now electric. A steady 15% of all new two-and-three wheelers are electric, with total sales reaching 10 million units. This move is led by China, India, and Southeast Asia — the world’s largest markets for these vehicles, accounting for around 80% of 2024’s global sales. These markets treasure the affordability and accessibility of two-and-three wheelers. After all, they’re often the easiest entry point into electric mobility for those in developing economies.

In India, electric two-wheeler sales reached 1.3 million in 2024 — 6% of our overall two-wheeler market. We have a dynamic ecosystem with 220 different manufacturers in 2024 — up from 180 in 2023 — though the top four companies account for about 80% of sales. Many of our electric two-wheelers are surprisingly affordable. The Ola S1X entry model, for example, comes with a 2 kWh battery and 6 kW peak power. It’s price tag of about INR 70,000 (around USD 850) is actually lower than the average price of the five best-selling conventional two-wheelers in India.

How did we manage this? Government support bridged much of the affordability gap. The PM E-DRIVE policy provides purchase incentives of up to INR 5,000/kWh for two-wheelers fitted with lithium-ion batteries, and it’ll continue to do so at least until March 2026.

Hopefully, this nascent ecosystem will be self-sustaining by then. We’re quickly getting there. The 80 largest electric two-wheeler makers in India had a combined production capacity of 10 million units in 2024 — almost 8 times the domestic sales that year. This capacity is expected to increase even further, to 17 million in the near term if all announced expansions come through. This may well position India as an export hub.

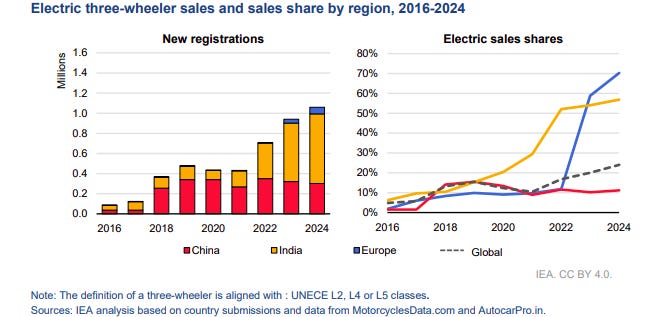

India has also seen lots of success with electric three-wheelers. In 2023, India overtook China to become the world’s largest market for electric three-wheelers. By 2024, a record 57% of India’s three-wheelers were electric. There’s a lot of nuance to this story, though, that we’ve talked about in detail before.

Battery demand and innovation

Before you can have an electric vehicle revolution, you need a battery revolution .

In 2024, global battery demand went past 1 terawatt-hours for the first time. That’s a staggering amount of energy storage. The battery demand in any average week in 2024 exceeded the total battery demand for an entire year , just one decade earlier. EVs were the primary driver of this surge, accounting for over 950 gigawatt-hours of battery demand — 25% more than in 2023. And this will only grow. EV battery demand is projected to reach more than 3 terawatt-hours by 2030, a threefold increase from today.

The supply is working over-time to match this demand.

Battery prices fell by about 20% in 2024 – the largest drop since 2017 – driven by low critical mineral prices and intensifying competition. But this decline wasn’t uniform across regions. While prices in China fell by nearly 30%, Europe and the United States saw a more modest 10-15% drop. This widening gap is partly why Chinese EV and battery producers have such an advantage.

India isn’t really a player in this game yet, as we explored recently. To us, right now, batteries are both a challenge and an opportunity.

On the one hand, it is a new business we can get into. We’ve opened our first domestic battery plants in 2024, with more than 5 GWh of manufacturing capacity. Reliance, a domestic leader, plans to launch a lithium-ion battery cell factory this year, and TATA is building a battery plant in Tamil Nadu.

But the question is: what happens if we don’t crack this industry? After all, we still have a long way to go – China’s battery manufacturing capacity is currently more than 500 times larger than India’s. If batteries are the new oil, as we believe, should we anticipate an OPEC-like battery squeeze in the future? We’re not the only ones asking this question. This is a concern in Europe and North America as well. China was responsible for 80% of global battery cell production in 2024 and has established a near monopoly on battery components production, supplying almost 85% of cathode active materials and over 90% of anode active material production.

This, as we recently explored, is true no matter which of the many battery technologies one looks at.

Charging infrastructure

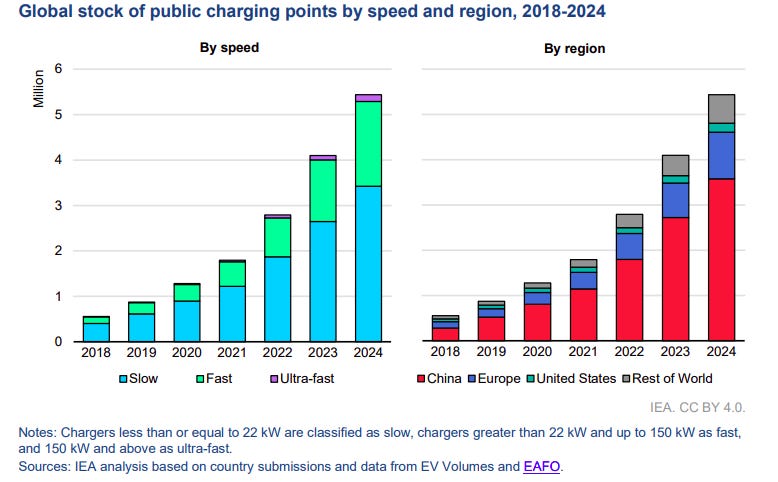

All these new electric vehicles need somewhere to charge. And the global charging infrastructure is expanding rapidly to meet demand.

Public charging stations have doubled in the past two years. More than 1.3 million public charging points came up in 2024 alone. That’s approximately equal to the total number of points available in 2020. About two-thirds of the growth in public chargers since 2020 has occurred in China, which now has about 65% of the charging infrastructure and 60% of the electric light-duty vehicle stock globally.

In Europe, the number of public charging points grew by more than 35% in 2024, to reach just over 1 million. The United States increased its charging stock by 20% in 2024 to just under 200,000 public charging points.

Beyond just the number of chargers, the world is also moving to better chargers. In 2024, the global stock of fast chargers reached 2 million, and ultra-fast chargers – capable of delivering 150 kW or above – grew by over 50%, now accounting for nearly 10% of all fast chargers. These ultra-fast chargers are critical for reducing charging times and making EVs more practical for a wider range of uses.

In India, too, our charging infrastructure is expanding rapidly. We’ve put up about 40,000 new public chargers in 2024 alone. This might accelerate further — in October 2024, INR 2,000 crore (USD 240 million) was allocated to charging infrastructure through the PM E-DRIVE scheme, mostly for our cities and heavily-used transport corridors. This push is particularly important for India. Most urban Indians live in multi-family buildings without dedicated parking. Public charging is essential for boosting EV adoption here.

But we aren’t pushing as strongly for fast charging. After all, 2 and 3-wheelers dominate our EV market, and their requirements are different. Most of these vehicles have small batteries that can be charged effectively with lower-power equipment. And that’s why our charging infrastructure could end up looking very different from what you see abroad.

We’re also trying out battery swapping because of our unique challenges. Instead of waiting for a vehicle to charge, riders can simply exchange their depleted battery for a fully charged one in a matter of minutes. Our battery swapping market has taken off in the past 5 years, with companies like Battery Smart and Sun Mobility leading the way. Battery Smart alone reached 1,000 stations in April 2024, while Sun Mobility has more than 630 swapping stations in 19 Indian cities.

But is this enough?

India’s charging infrastructure would need to grow nearly fivefold by 2030 to support our projected EV growth. That means adding around 50,000 charging points each year through 2030 — 30% more than the number of additions in 2024. This requires a significant investment

Can our grid even handle such a surge? Interestingly, yes. The impact of this on our electricity grid would actually be manageable. Even with our projected growth in EVs, they would account for only about 1.1% of India’s total electricity demand by 2030. In fact, EVs could become a valuable source of flexible demand for our growing but intermittent renewable energy capacity, helping to integrate more solar and wind power into our grid. Technologies like smart charging can ensure that EVs charge during times of high renewable energy availability, further reducing their environmental impact.

Tidbits

-

IndiGo to Bring Back 80 Grounded Aircraft Amid Operational Recovery

Source: Business Standard

IndiGo is set to restore 80 of its grounded aircraft back into service over the coming months, according to a report from Business Standard.This increase is about twice the airline’s typical annual addition of 40 planes.The planned restoration is expected to boost the airline’s fleet strength significantly and could help moderate airfares. IndiGo, India’s largest airline by market share, has faced capacity challenges due to the grounding but is now focused on stabilizing its operations. The move aligns with the airline’s broader strategy to scale operations and expand its route network. The return of these aircraft marks a key step in improving asset utilization and enhancing service reliability. -

ITC Reports Profit Growth Driven by Cigarette Business and Rural Demand

Source: Reuters

ITC Ltd. has reported a rise in quarterly profit, supported primarily by growth in its cigarettes segment and continued strength in rural markets. The company’s cigarette sales grew nearly 6%, benefiting from price hikes, improved volumes in competitive regions and premium offerings that are generally margin-boosting. This contributed significantly to the overall earnings performance. Other segments such as FMCG, agribusiness, and hotels remained stable.

- Govt Notifies Payments Regulatory Board with Equal Representation from RBI and Centre

Source: Business Standards

The Government of India has notified the Payments Regulatory Board Regulations, 2025, establishing a new Payments Regulatory Board (PRB) to replace the RBI’s existing Board for Regulation and Supervision of Payment and Settlement Systems (BPSS). The PRB will comprise six members—three nominated by the RBI and three by the central government—with the RBI Governor serving as Chairperson and holding the casting vote. Other members include the RBI Deputy Governor in charge of payment systems and an officer nominated by the RBI’s central board. The PRB will be supported by the Department of Payment and Settlement Systems (DPSS) within the RBI. Additionally, experts in payments, IT, and law may be invited to board meetings, with the RBI’s principal legal adviser as a permanent invitee.

- This edition of the newsletter was written by Pranav and Prerana.

Have you checked out The Chatter?

Have you checked out The Chatter?

Every week, we listen to the big Indian earnings calls—Reliance, HDFC Bank, even the smaller logistics firms—and copy the full transcripts. Then we bin the fluff and keep only the sentences that could move a share price: a surprise price hike, a cut-back on factory spending, a warning about weak monsoon sales, a hint from management on RBI liquidity. We add a quick, one-line explainer and a timestamp so you can trace the quote back to the call. The whole thing lands in your inbox as one sharp page of facts you can read in three minutes—no 40-page decks, no jargon, just the hard stuff that matters for your trades and your macro view.

Introducing “What the hell is happening?”

In an era where everything seems to be breaking simultaneously—geopolitics, economics, climate systems, social norms—this new tried to make sense of the present.

“What the hell is happening?” is deliberately messy, more permanent draft than polished product. Each edition examines the collision of mega-trends shaping our world: from the stupidity of trade wars and the weaponization of interdependence, to great power competition and planetary-scale challenges we’re barely equipped to comprehend.

What the hell is happening?

What the hell is happening?Subscribe to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets—both in India and globally.

Thank you for reading. Do share this with your friends and make them as smart as you are ![]()