Our goal with The Daily Brief is to simplify the biggest stories in the Indian markets and help you understand what they mean. We won’t just tell you what happened, but why and how too. We do this show in both formats: video and audio. This piece curates the stories that we talk about.

You can listen to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and videos on YouTube. You can also watch The Daily Brief in Hindi.

In today’s edition of The Daily Brief:

- Why Intel’s no longer a superpower

- Climate change and economic damage

- What Trump’s steel and aluminium tariffs mean for India

Why Intel’s no longer a superpower

Intel was once synonymous with the global semiconductor industry. It wasn’t just a chip company; it was THE chip company. Its dominance felt untouchable. Its processors powered most of the world’s computers. From its breakthrough x86 architecture to its iconic "Intel Inside " marketing campaign, the company sat at the heart of global chip-making. Most of the world’s bleeding-edge technology was possible because of Intel chips.

Fast forward to today, that same company has become an acquisition target . Competitors that once quivered before Intel’s might are now hoping to strip it for parts. That’s a profound fall from grace for one of the world’s most incredible companies.

The question is — where did it all go wrong for Intel?

Intel’s many missteps

Intel’s downfall didn’t come from a single bad decision. The company made a series of miscalculations and strategic missteps which compounded over time.

Intel came from the era of ‘Integrated Device Manufacturing’ or IDM. It designed chips and then ‘fabricated’ those chips itself (i.e. turned silicon wafers into chips), much like its early competitors like IBM or Texas Instruments. From the 1990s onwards, younger companies began moving to a ‘fabless’ model, designing chips and then sending those designs to companies like TSMC and Global Foundries for fabrication. But that was a forced decision — based on how they couldn’t afford their own fabrication facilities. Intel, meanwhile, prided itself on its ability to do everything in-house. In an era where making chips was relatively simple, this was a huge advantage as well. It would soon become a problem, however.

Sitting out the smartphone boom

Meanwhile, in 2007, Apple approached Intel to make chips for its first iPhone. Intel turned it down, citing low profit margins. This was Intel’s first great mistake. Because of that decision, Apple decided to license chip designs from the British chip maker, ARM, which were sent to Samsung for production. In a few short years, this turned into an entire industry segment. Soon, Qualcomm, Apple, and other companies built entire businesses around power-efficient processors. Intel, meanwhile, found it increasingly difficult to enter the space. Most mobile applications were made for ARM designs and ran poorly on Intel chips. The company struggled to gain any relevance in mobile computing and exited it altogether in 2016.

Intel’s fabrication woes

Around the same time, Intel’s own chip manufacturing unit—the very foundation of its strength—started running into problems. For years, Intel had set the pace for ‘Moore’s Law’, improving the quality of its manufacturing at such a rate that the transistor density in chips doubled every two years. But slowly, it started to fall behind. When it was time to transition to 10-nanometer chips, things went south. Manufacturing delays, technical roadblocks, and poor execution created room for rivals like AMD to push past Intel. After all, unlike Intel, AMD merely had to think of chip design — companies like TSMC had to think of how to get production into place.

This was the era where companies were setting up huge data centers — to capture a series of booms, from the explosion of the internet to cloud computing.

This is where AMD began capturing market share from Intel. While Intel struggled with 10 nm chips, AMD quickly graduated to 7 nm, and then 5 nm chips. Its EPYC servers began crushing Intel’s equivalents, allowing it to take up a big share of the data centre market. Meanwhile, it also began to eat into Intel’s dominance in PC chips, with its Ryzen series.

Losing out on artificial intelligence

And then came the biggest of all problems — Artificial intelligence.

The explosion of AI after 2020 completely reshaped the semiconductor landscape. When it came, it seemed like Intel didn’t grasp the magnitude of what was happening. It had built an empire on general-purpose CPUs, but AI demanded specialized chips—powerful GPUs and AI accelerators. It was now Nvidia’s turn to shine.

For a long time, Nvidia played second fiddle to Intel and AMD. While these companies made CPUs — the main chips that ran personal computers — Nvidia played second fiddle with its GPUs, which merely made video games run well. But these chips had other uses. They were really useful in mining crypto-currency, for instance, and in the crypto boom that began in 2017, it saw a steady increase in the demand for its products.

Then came AI, and the game changed entirely. With its CUDA software ecosystem and AI-focused GPUs, NVIDIA became the undisputed leader in AI hardware. The company doubled down, innovating at a frenetic rate, until it was the undisputed backbone of AI computing. The rest of the industry has been left playing catch-up — at least for now.

Intel, obviously, tried to respond. It made massive bets on AI hardware and even acquired companies like Habana Labs to build AI-focused processors. But these efforts were just too late—and they failed to gain significant traction.

Intel’s last-ditch attempts at recovery

After all these tumultuous years, the semiconductor industry today is very different from what it was during Intel’s golden era. Even the biggest players don’t do everything themselves. Both NVIDIA and AMD, for example, don’t manufacture their own chips, instead outsourcing production to TSMC. Intel, however, tried to do everything in-house—design, manufacturing, marketing, and sales. That strategy, once Intel’s strength, became its biggest liability. In a sense, it was simultaneously competing in two different industries—chip design and fabrication—each with extremely capable and innovative entities. It simply didn’t have the flexibility of its rivals.

When Intel realized it was losing ground, it tried to correct its course. Under former CEO Pat Gelsinger, Intel decided not just to make its own chips but also to manufacture chips for other companies. It effectively tried to transform itself into a foundry like TSMC, pouring billions into new factories in the US and Europe.

But timing was again a problem—while Intel was trying to revamp itself, the market was demanding immediate AI breakthroughs. Investors and customers grew impatient. Gelsinger’s vision was bold, but since Intel was already behind in the race, their execution was extremely slow. By late 2024, Intel’s struggles deepened, and the board decided it was time for a leadership change. Gelsinger was pushed out.

Intel, btw, didn’t just fail in manufacturing; it also struggled with strategic acquisitions. Over the years, it made several big-ticket purchases in an attempt to diversify its business. It acquired Altera for $16.7 billion in 2015 to gain a foothold in programmable chips. It then bought Mobileye for $15.3 billion in 2017 to expand into automotive technology. It even attempted to strengthen its AI play with Habana Labs.

But none of these bets ever turned into real competitive advantages. NVIDIA and AMD kept pulling ahead, and Intel’s acquisitions failed to deliver the impact it had hoped for.

The scavengers appear

Intel has weakened as an entity. It’s trying to shed deadweight and has just laid off over 15,000 employees. In fact, it briefly even stopped offering free tea and coffee to its employees. Several companies now see an opportunity to acquire pieces of it:

-

Broadcom has offered to acquire Intel’s design and marketing segment. Broadcom, for context, is a powerhouse in semiconductors and networking solutions. They want Intel’s intellectual property and branding strength, but they don’t seem to have any interest in capital-intensive chip manufacturing.

-

TSMC, the world’s leading contract chip manufacturer, is eyeing Intel’s factories. But instead of outright buying them, TSMC is considering forming an investor group to take control of Intel’s manufacturing operations, which would further solidify its dominance in semiconductor fabrication.

-

Qualcomm, which dominates mobile processors, had, back in September 2024, expressed interest in a full acquisition of Intel. If that deal is still on the table and it does happen, it could be one of the biggest semiconductor deals in history.

But there’s another option for Intel. Apollo Global Management, which is a private equity firm, has proposed investing in Intel for about a 5% stake. If Intel decides to take this path, it could buy some time to restructure and attempt a comeback rather than be absorbed by competitors.

What’s next?

So, then, the big question then is - what’s next for Intel? Does Intel really have the fight left to reinvent itself, or is it simply too late?

The semiconductor industry is evolving at a breakneck pace, and Intel has repeatedly struggled with timing. The AI boom, the shift in chip manufacturing, and the rise of fabless giants like NVIDIA have reshaped the landscape.

Intel’s legacy is undeniable. Over the years, it has built an extensive portfolio of patents covering everything - from processor architectures to advanced manufacturing techniques. Its intellectual property remains one of the strongest in the industry, with key innovations in areas like high-performance computing and semiconductor fabrication. In addition to that, Intel has also formed strategic partnerships with major tech players like Microsoft, Dell, and Lenovo to ensure that its chips power a wide range of their devices. But that said, despite this rich legacy, whether or not Intel has a future as an independent company remains very uncertain.

That’s not unusual for this industry, though. In the early 2000s, when Intel and AMD entered the graphics processing space, it seemed like Nvidia would find it hard to survive. In 2008, it seemed like AMD was bankrupt, and turning fabless was its desperate gambit for survival. Both these companies scripted dramatic turnarounds. Can Intel follow suit? Or are we witnessing the death of a giant?

Either way, this is a development worth tracking, because the future of one of the most iconic companies in tech hangs in the balance.

Climate change and economic damage

Here’s a critical story that’s been making waves in central banking circles - the growing economic toll of climate change. This isn’t your typical environmental story - we’re talking hard numbers, economic impacts, and why central bankers are increasingly losing sleep over rising temperatures.

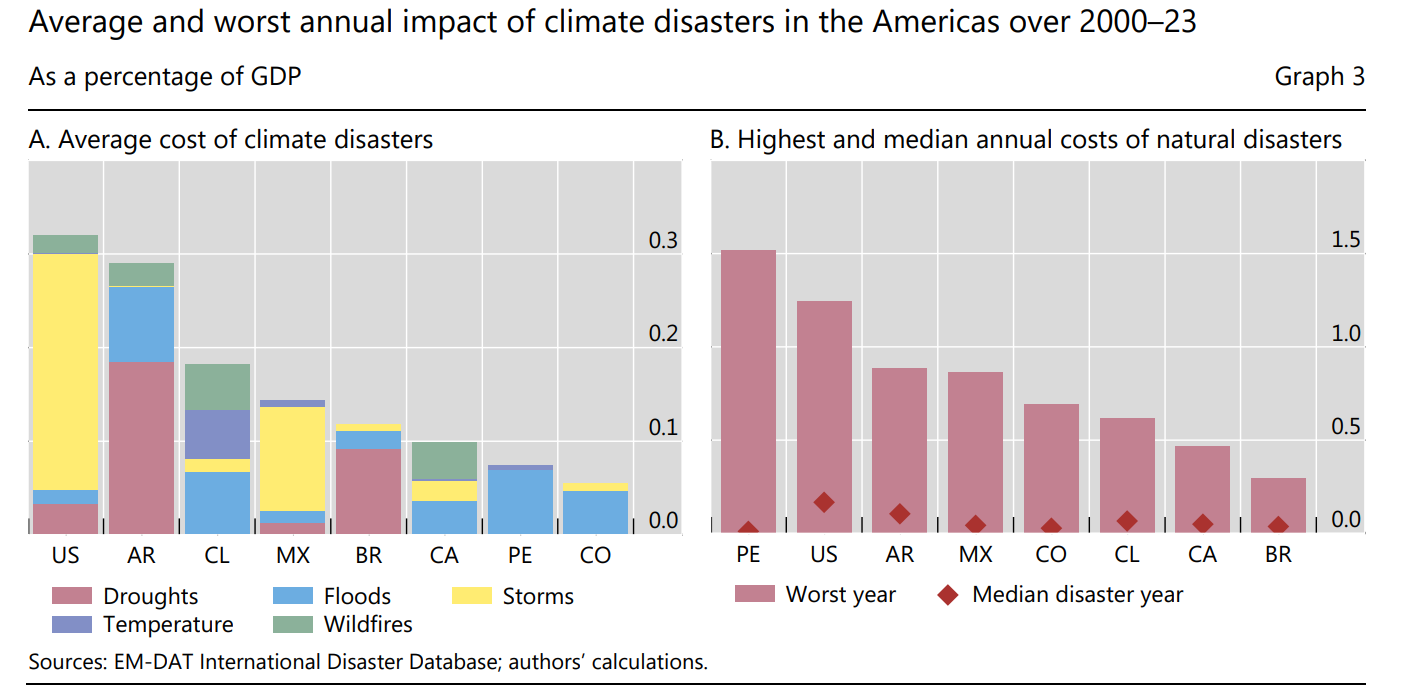

Let’s start with a major report just released by the Bank for International Settlements - that’s essentially the central bank of central banks. The BIS bulletin examined data from eight major economies in the Americas and found something fascinating - different types of extreme weather events impact the economy in distinct ways through various transmission channels. But here’s the kicker: droughts in particular seem to be the real economic killers. They found that droughts reduce economic output for up to two years after they occur, mainly by devastating agriculture, forestry, and electricity production.

Source: BIS

And these impacts aren’t just theoretical. The bulletin points out real examples - like when floods in Rio Grande do Sul in 2024 hit a region accounting for 12.7% of Brazil’s agriculture and 8.4% of manufacturing. Or when Hurricane Helene disrupted a major quartz producer in October 2024, sending shockwaves through global chip production. These events show how localized climate disasters can ripple through global supply chains.

The insurance angle is also fascinating. The BIS data shows insurance premiums represent between 0.7% and 3% of GDP across these economies. But here’s the concerning trend - as extreme weather events become more frequent, premiums are rising and some insurers are pulling out entirely, creating what experts call an ‘insurance gap.’ This gap between total losses and insured losses reached about 60% globally in recent years.

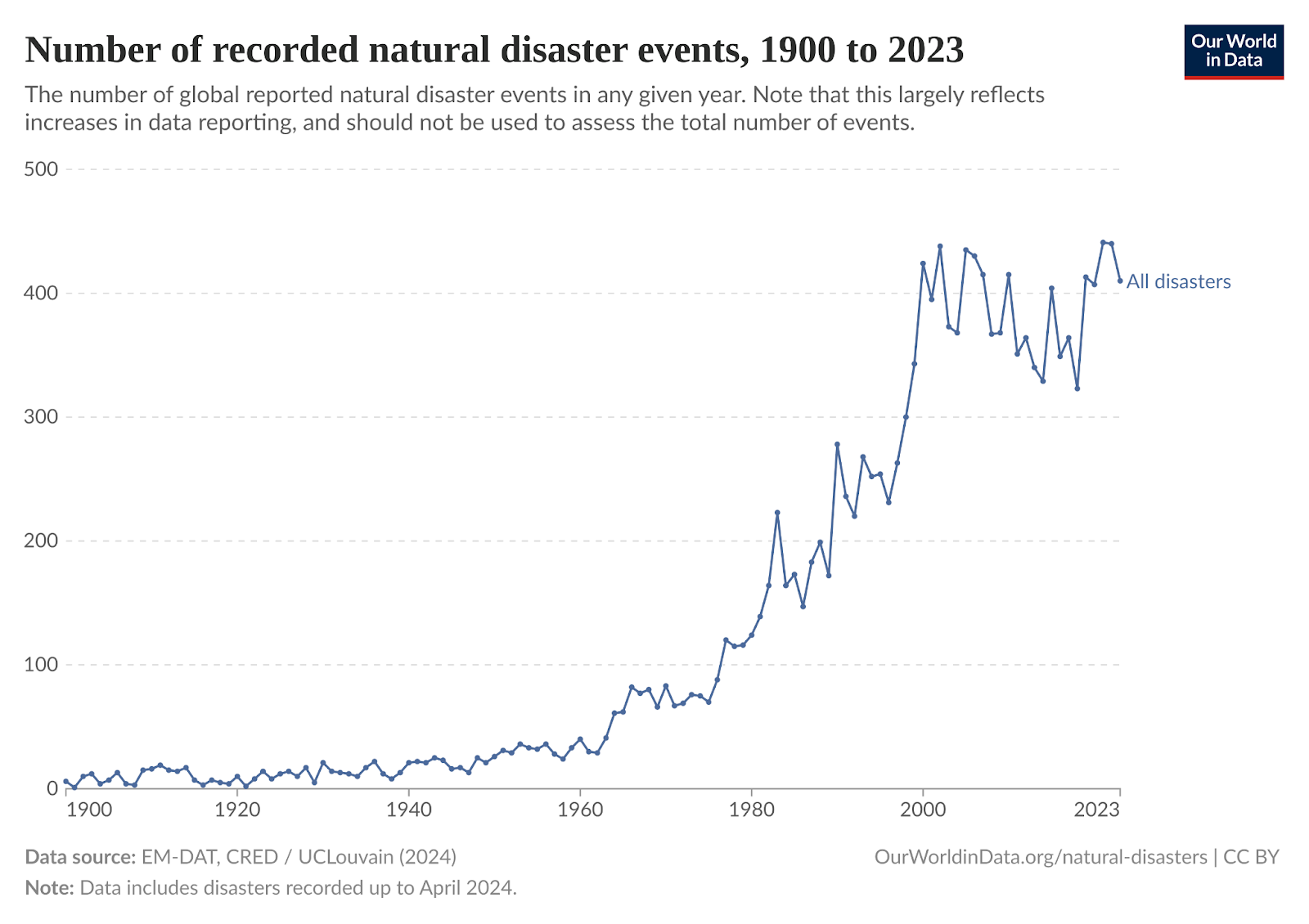

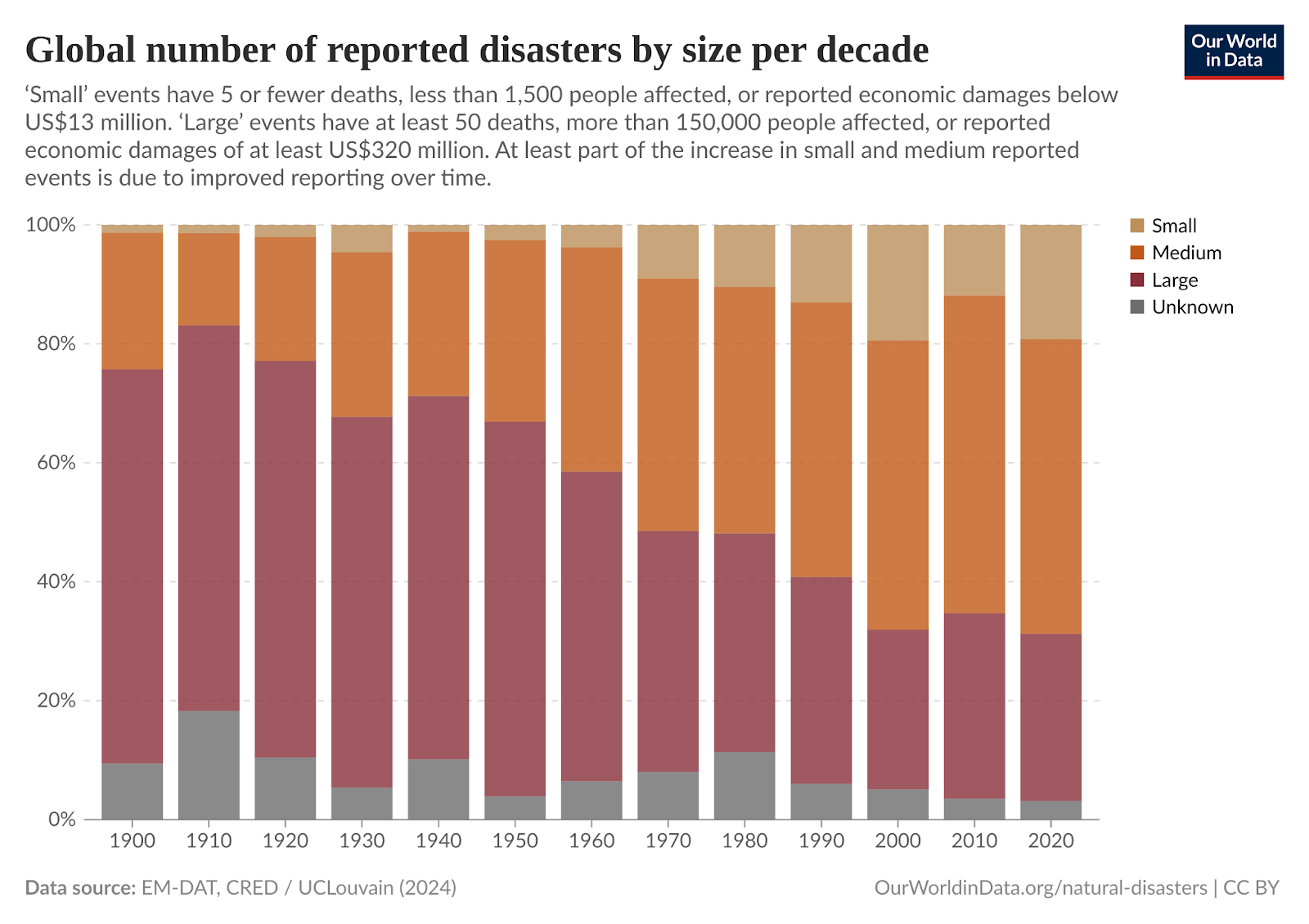

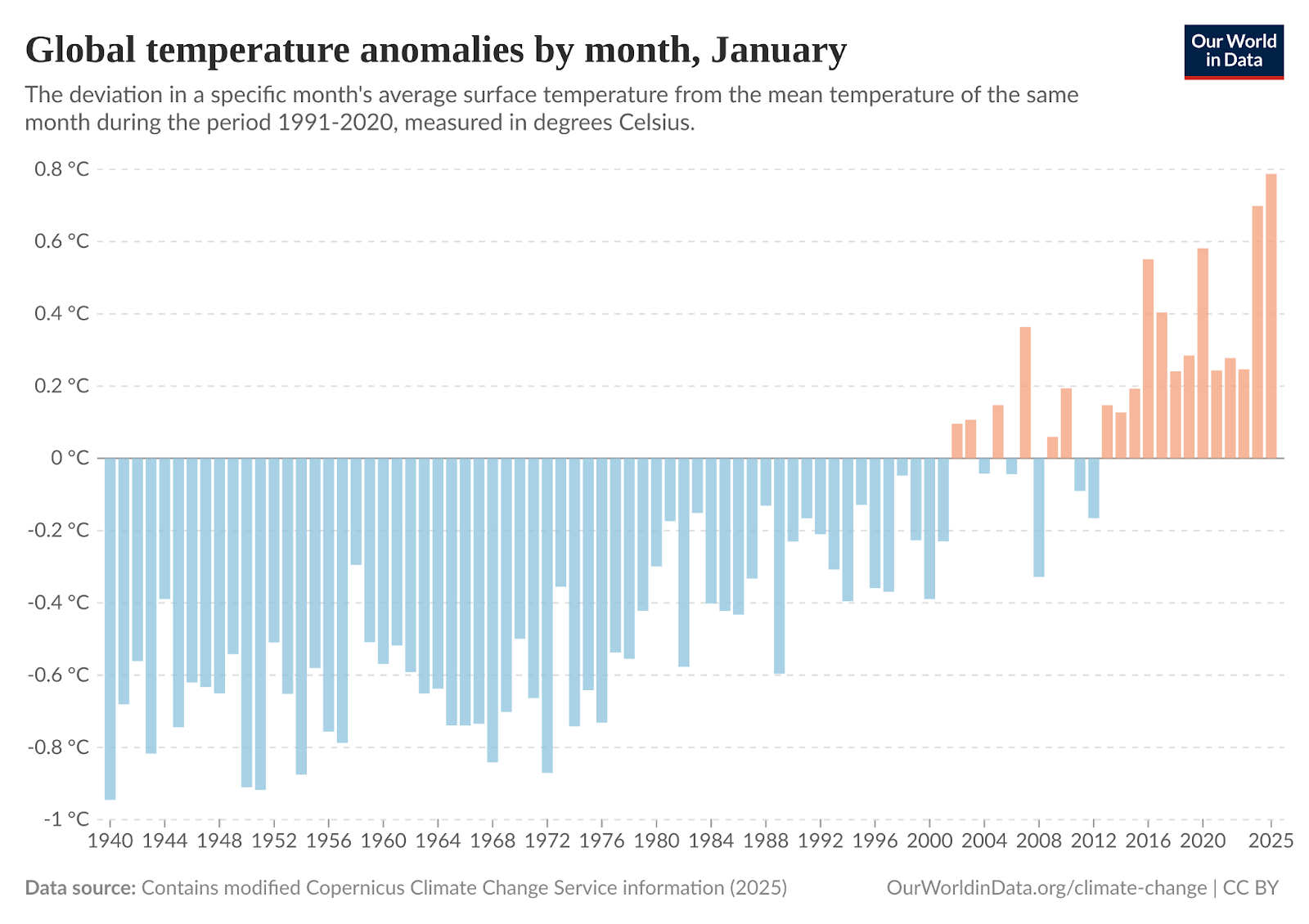

Now, let me add some important context here from Our World in Data. When you look at disaster databases like EM-DAT, they show a dramatic rise in natural disasters since the 1980s. The UN and World Meteorological Organization have cited this data to claim disasters have quadrupled since 1970. But here’s the crucial nuance - a lot of this apparent increase reflects better reporting and data collection, not necessarily more disasters. EM-DAT itself warns about this in its documentation. The database wasn’t even created until 1973, and systematic data collection really only began in the 1980s. During these decades, we also saw massive improvements in telecommunications, satellites, and reporting capabilities.

Source: Our World In Data

If you look at disasters with more than 1,000 deaths, the trend is much more stable over time. It’s the reporting of smaller events that’s driving much of the apparent increase. This doesn’t mean climate change isn’t increasing disaster frequency - it likely is. But it does mean we need to be very careful about how we interpret historical data and trends.

Source: Our World In Data

Projecting the economic impact of climate change is incredibly difficult. As the statistician George Box famously said, “All models are wrong, but some are useful.” The economic models we use to estimate climate damages vary widely in their predictions. Some studies suggest damages of just 1% of GDP from an additional 1°C of warming, while others project devastating losses of up to 25%. That’s a massive range of uncertainty.

Let’s talk about some specific channels through which climate change hits the economy. Extreme temperatures directly impact labor productivity - it’s simply harder for people to work effectively in extreme heat. There’s damage to physical capital from floods and storms. Agricultural yields decline. Energy costs spike during extreme weather. And all of this feeds into inflation through food and energy prices.

Source: Our World In Data

The timing of these impacts is also crucial. There’s significant debate about whether climate shocks create level effects or growth effects on the economy. If they’re just level effects, the economy takes a one-time hit but then returns to its previous growth rate. But if they’re growth effects, climate change could permanently lower an economy’s growth rate - that’s a far more devastating long-term impact.

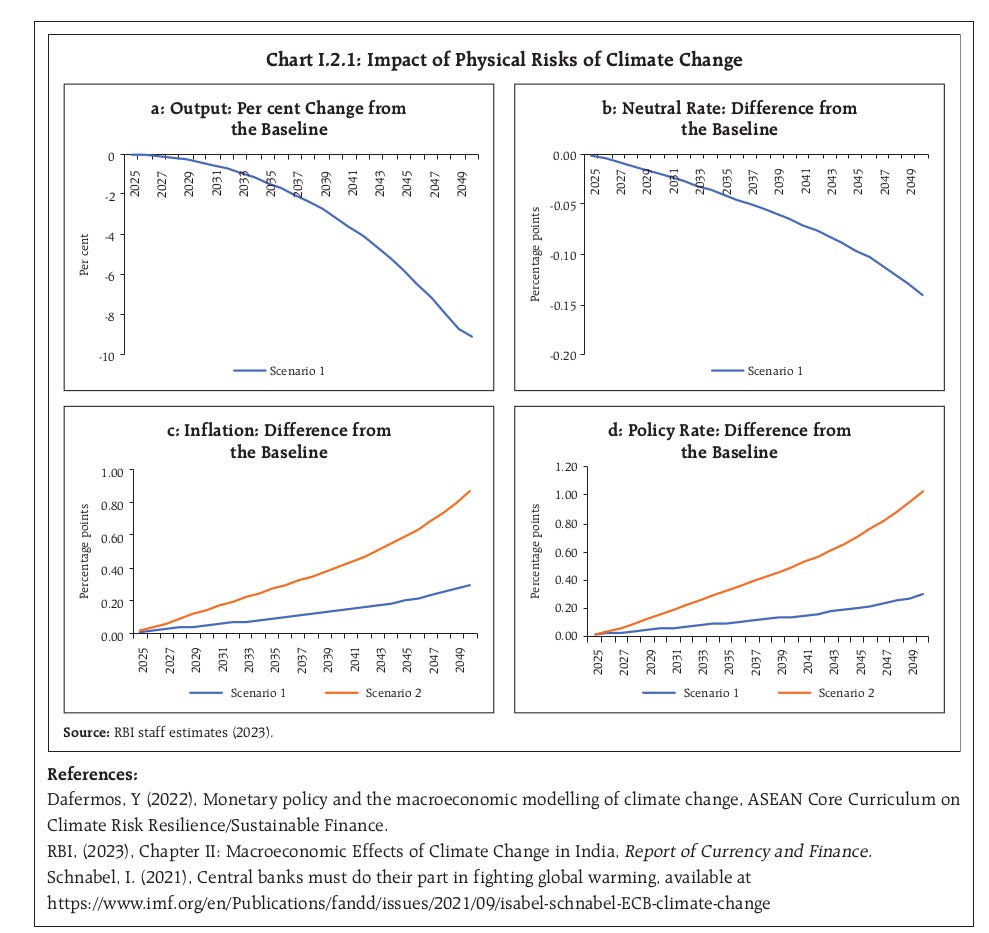

Now, let’s zoom in on India, which offers a fascinating case study. RBI research shows how climate change is wreaking havoc with food prices there. In 2023-24, El Niño conditions led to both a hotter summer and inadequate monsoon rains. This double whammy hit agricultural production hard, pushing up food inflation. And remember - in a country where millions still live in poverty, food inflation isn’t just an economic statistic, it’s a human crisis.

The RBI’s modeling is particularly sobering. Their analysis indicates that without any climate mitigation policies, India’s long-term output could be lower by around 9% by 2050 compared to a no-climate-change scenario.

What’s particularly concerning is that both inflation and its volatility are projected to increase over time. Lower productivity may lead to a fall in the natural rate of interest, but here’s the paradox - frequent shocks to inflation will force central banks to maintain tighter monetary policy even with a lower natural rate.

Last year, RBI Deputy Governor Rajeshwar Rao gave a remarkable speech highlighting how climate change transcends traditional risk categories. He made a crucial point - unlike typical financial risks that can be managed through traditional tools like insurance, climate risks hit entire regions and industries simultaneously. You can’t just diversify away from climate risk.

And there’s another crucial angle here - the distributional impacts. The RBI’s research suggests climate change could exacerbate inequality because poorer households and small businesses typically have fewer resources to adapt and recover from climate shocks. They’re also more likely to work in climate-sensitive sectors like agriculture and construction.

This creates a feedback loop - climate shocks increase poverty, which reduces the economy’s resilience to future shocks. The RBI’s stress testing suggests this could create what they call ‘climate poverty traps’ in certain regions.

Let me put this in perspective - we’re seeing a fundamental shift in how central banks think about climate change. It’s no longer viewed as just an environmental issue but as a core macroeconomic and financial stability concern. The data increasingly suggests that climate change could force central banks to maintain higher interest rates even as economies struggle, creating a persistent stagflationary bias.

This is a complex story that’s still unfolding. But one thing is clear - the economic impacts of climate change are becoming impossible for policymakers to ignore. The question isn’t whether climate change will impact the economy, but how severe those impacts will be and how we can best prepare for them.

What Trump’s steel and aluminium tariffs mean for India

Over the last few weeks, we’ve often talked about how America’s new tariffs threaten to tear up the delicate balance of foreign trade. Let’s see how that plays out with one specific tariff.

In an effort to protect America’s domestic steel and aluminium industries, last week, Donald Trump announced a 25% tariff on imported steel and aluminium products from anywhere in the world. This isn’t the first such tariff. Back in 2018, President Donald Trump announced a similar move — with tariffs of 25% on steel imports, and 10% on aluminium. This led to chaos across the world. Other countries retaliated with their own tariffs, while businesses restructured their supply chains.

President Biden, through his term, brought some of these tariffs down. In July 2023, for instance, the United States removed tariffs on Indian steel and aluminum exports after long negotiations.

Those tariffs are now back. For aluminium, in fact, those tariffs are now higher than ever.

So, what do these tariffs mean for India? That’s a complicated question. While India’s direct exports to the US are limited, such measures have ripple effects that could affect Indian businesses and consumers heavily. A new Care Ratings report sheds some light on these dynamics. Let’s dive in.

The impact on India’s steel industry

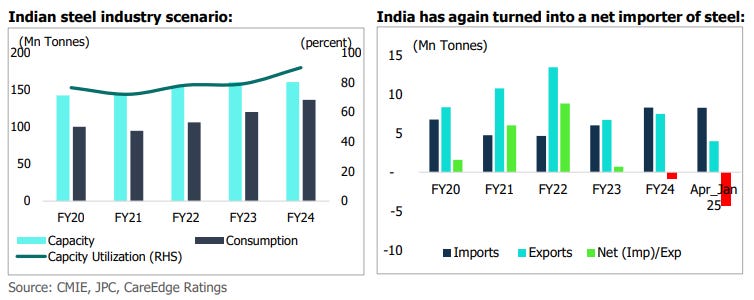

India is both the world’s second-largest producer and consumer of steel, second only to China. Over the last decade, India’s steel production capacity grew at a CAGR of 4.6%. But while India was ramping up how much steel it could make, the amount of steel it could use was growing much faster. Our domestic consumption of steel has risen at a CAGR of 6.3% over the last decade. This has been more dramatic in the last five years when India’s steel consumption has surged by a CAGR of 8%, even though we were increasing our capacity at a rather subdued rate of 3%.

The result? Over the last few years, India has become a net importer , rather than an exporter, of steel:

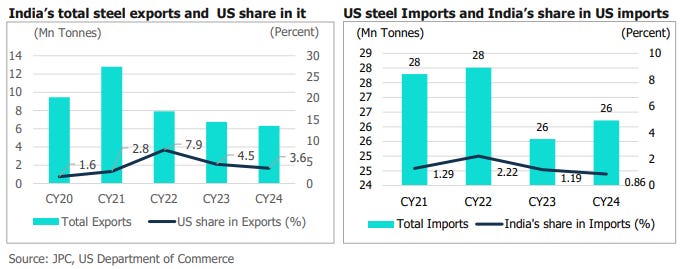

Meanwhile, the United States is hardly a major market for Indian steel exporters. India’s direct steel exports to the US made up just 4% of our total steel exports in 2024 — a total of 6.3 million tonnes. This share may well be hit by America’s few tariffs, but all in all, that’s hardly a lot.

In essence, exports aren’t a big part of India’s steel industry, and America isn’t a big part of India’s steel exports. So, do these tariffs amount to nothing? Well, there’s more to consider here.

Over the last few years, the global prices of steel have fallen drastically. The demand for steel has been declining in major consuming markets like the US, Japan, the European Union, and most importantly, China. China makes 50% of the world’s steel. Yet, its domestic steel demand is falling, even though it’s producing steel at peak capacity. This surplus is all exported out — often at rock-bottom rates. In 2024, Chinese steel exports reached 90-95 million tonnes, up substantially from 65 MnT in 2022.

Where does that steel go? Well, think about it: India’s been on a construction spree — with infrastructure projects and urbanisation proceeding everywhere at a furious pace. You need steel to construct things. And that became a massive opportunity for China. 43% of India’s steel imports, in fact, came directly from China — with more being routed through countries like Vietnam.

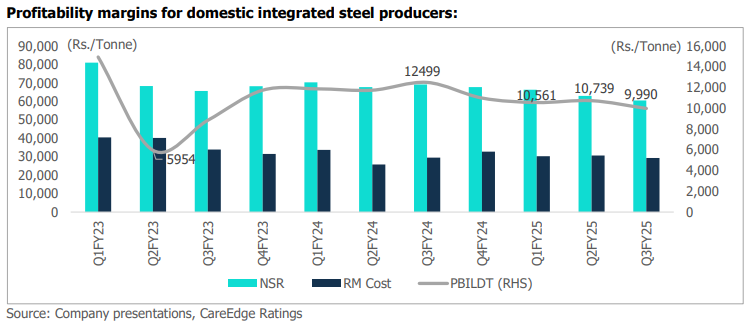

This has hit the profitability of Indian steel-makers hard. While our imports grew by 38% in FY 2024, and another 20% in the first ten months of the current Financial Year. Meanwhile, exports fell by 29% in the first ten months of the current Financial Year.

This is the real concern around US tariffs on steel. While the direct impact on our exporters will be limited, as the American market closes down, global steel demand will fall even further. Suppliers from all over the world will gun for the Indian market. This will put Indian producers under even more pressure.

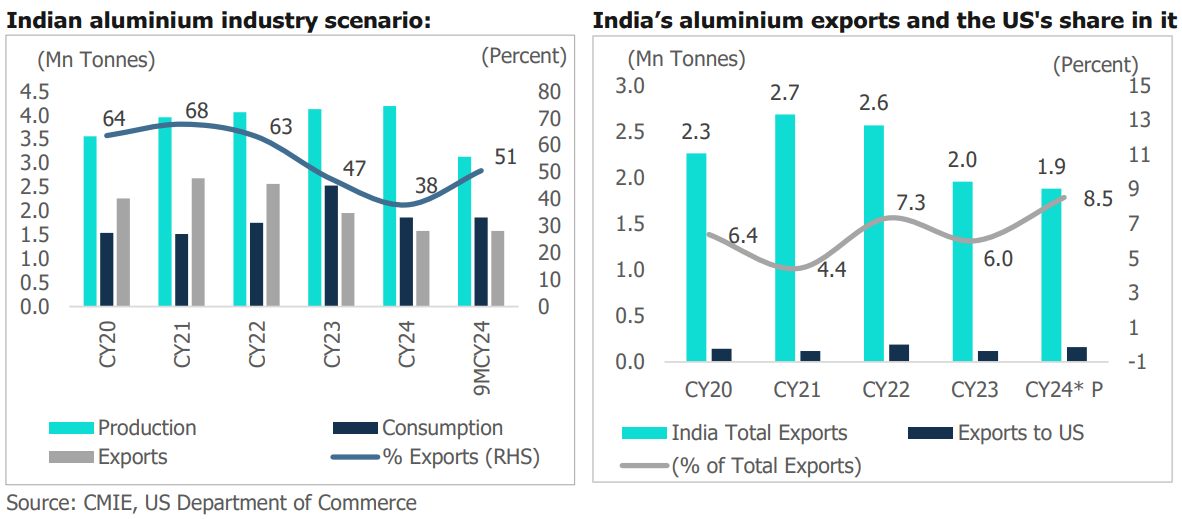

The Impact on Indian Aluminium

Unlike steel, India’s aluminium sector faces more direct exposure to US tariffs.

India is the world’s second-largest producer of aluminium. Don’t put too much weight on that statistic though; we’re far behind China, the global leader. India comprises 6% of global aluminium production, compared to China’s 60%. But crucially, unlike steel, exports are extremely important to Indian aluminium manufacturers. We export about 40% of our total aluminium production. The US market accounts for 6-8% of these exports. This sector, therefore, is relatively more vulnerable to US trade policies than steel.

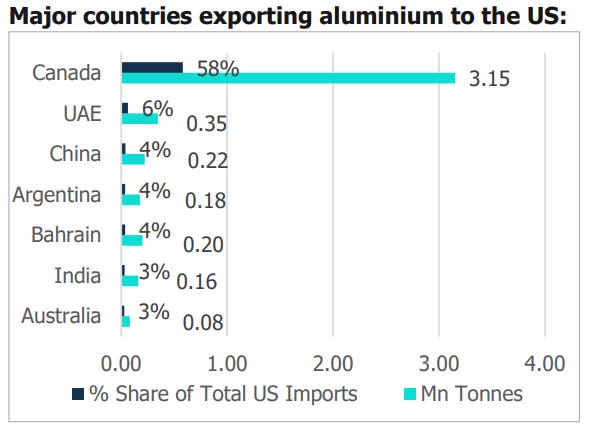

This vulnerability isn’t too high either, however. India’s total aluminium exports to the United States are at a relatively muted 0.16 million tonnes per annum.

India holds a crucial advantage in aluminium production — we have abundant high-quality bauxite reserves. This makes us one of the world’s lowest-cost producers of aluminium. This cost advantage could help cushion some of the impact we face from US tariffs.

What does it all mean?

In all, as the world’s second-largest producer of steel and aluminium, Trump’s new tariffs seem like they would be terrible for the country. But international trade is hardly that simple.

Steel and aluminium are heavy, after all, and shipping them across the world is hardly as lucrative as shipping higher-value products like iPhones or pharmaceuticals. This is why America is a relatively small market for our steel and aluminum producers. America derives the largest share of these products from its immediate neighborhood — from countries like Canada, Mexico, and Brazil.

But that doesn’t mean India is immune to these changes either. World trade, as we’ve often mentioned, is complex. There are all sorts of second-order effects that these tariffs can have. India’s steel sector has already been suffering in the face of foreign competition, and this new move might make things worse.

Tidbits

- Despite the RBI’s 25 bps repo rate cut, corporate bond yields continue to rise due to a ₹1.8 Lakh Cr. liquidity deficit in the banking system. In February, the yield spread between corporate and government bonds widened by 25 bps, driven by a surge in corporate debt issuance. The 5-year AAA-rated corporate bond yield stands at 7.46%, while the 10-year is at 7.30%, leading to an inverted yield curve.

- India’s oil imports from the U.S. jumped to 218,400 bpd in January from 70,600 bpd in December, making the U.S. its fifth-largest supplier. Meanwhile, Russian imports rose 4.3% to 1.58 million bpd, but future purchases could decline due to sanctions. Middle Eastern crude surged 6.5% to 2.7 million bpd, pushing its share in India’s oil imports to a 27-month high of 53%.

- India’s urban unemployment rate declined to 6.4% in Q3 FY25, down from 6.5% in Q3 FY24, as per the NSSO survey. The joblessness rate for women improved to 8.1% from 8.6%, while for men, it remained at 5.8%. The survey covered 45,074 households and 170,487 individuals under a rotational panel method.

- This edition of the newsletter was written by Anurag, Bhuvan and Pranav

Have you checked out One Thing We Learned?

Have you checked out One Thing We Learned?

It’s a new side-project by our writing team, and even if we say so ourselves, it’s fascinating in a weird but wonderful way. Every day, we chase a random fascination of ours and write about it. That’s all. It’s chaotic, it’s unpolished - but it’s honest.

So far, we’ve written about everything from India’s state capacity to bathroom singing to protein, to Russian Gulags, to whether AI will kill us all. Check it out if you’re looking for a fascinating new rabbit hole to go down!

Subscribe to Aftermarket Report, a newsletter where we do a quick daily wrap-up of what happened in the markets—both in India and globally.

Thank you for reading. Do share this with your friends and make them as smart as you are ![]()