Investors have this perception that returns on debt mutual funds are fixed and steady, just like in the case of bank deposits. However, the fact is that debt mutual fund returns are not steady or safe and depend on various factors, such as the credit quality of the portfolio, the current interest ratio scenario, and the scheme’s investment strategies, among other factors. So, your investment in a debt mutual fund scheme is subject to market risk.

One of the key factors that can affect the returns of debt mutual funds is changes in the interest rate scenario and the credit environment. That said, not all categories are equally sensitive to interest rate changes. Furthermore, schemes within each category may differ in performance based on their duration strategies.

Average Maturity, Macaulay Duration, and Modified Duration are the important parameters that investors can use to assess how sensitive a scheme will be to changes in interest rates. In this article, we will explain what is Average Maturity, Macaulay Duration and Modified Duration in debt mutual funds and how you can use them while selecting a debt mutual fund for your portfolio.

What is Average Maturity and why it is important?

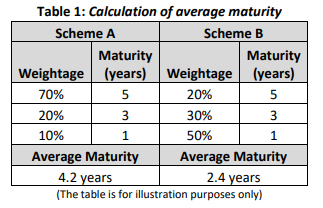

A bond’s maturity is the date on which the investors get their principal back along with interest. Since debt mutual funds invest in a range of debt securities, and each security may have a different maturity date and weightage in the portfolio, the average maturity of a scheme is taken as the weighted average of all the securities held in the portfolio. The Average maturity profile can be calculated in days, months, or years.

A higher maturity period shows that the fund has invested predominantly in securities that will mature over the long term, say 3-5 years or more. Likewise, lower average maturity highlights that a scheme has higher exposure to short-term securities.

A point to note is long-term debt papers are more sensitive to interest rate movements. When interest rates fall, the funds that hold long-term debt papers generally generates better returns as bond prices fall. However, they may not do well in a rising interest rate scenario. On the contrary, funds with shorter maturity profiles are less impacted by interest rate movements.

The average maturity of a debt scheme can help investors to choose a scheme that aligns with their investment horizon. It can also help investors to reduce interest risk by re-balancing their debt portfolio in line with the changing market scenario.

In the above example, Scheme A has a higher average maturity of 4.2 years compared to Scheme B, whose average maturity is 2.4 years. Therefore, Scheme B’s Net Asset Value (NAV) has less chance to get impacted due to changes in interest rates.

So, as an investor, if you have a low-risk appetite, you may be better off investing in schemes with low average maturity, such as Liquid Funds, Ultra Short Duration Funds, Short Duration Funds, etc.

On the other hand, if you have a long-term investment horizon and the ability to handle volatility in the debt market, you may consider Long term debt funds such as Gilt Funds that invest in long-term debt papers having higher maturity.

If you are unsure about the interest rate outlook and want to avoid the volatility accompanied to long term bonds, another option is a Dynamic Bond Fund that has the flexibility to actively modify the duration or maturity of the securities it invests in.

What is Macaulay Duration and why it is important?

Investors in bonds usually receive periodic payments in the form of coupons, while the principal amount is paid back on maturity. Macaulay Duration measures how long an investor has to hold on to a bond to get back invested money through periodic coupon payments and principal repayment.

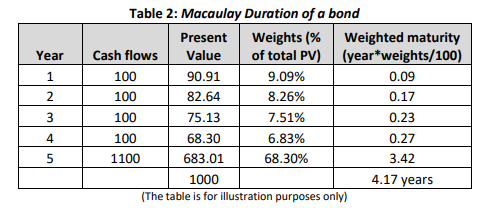

In the case of debt funds, the Macaulay Duration is the weighted average Macaulay Duration of each individual bond in a scheme’s portfolio. The weight of each cash flow is determined by dividing the present value of the cash flow by the price, discounted by the current yield to maturity. Macaulay Duration is expressed in years and is a better indicator of duration compared to maturity.

Macaulay Duration depends on the average maturity. The higher the maturity, the longer will be Macaulay Duration. Furthermore, since it considers periodic cash flows in the form of coupon payments, a fund’s Macaulay Duration will be lower than its average maturity, though the magnitude of difference may differ from one scheme to another. If a scheme holds securities that have higher coupon payout, then the cash flows will be higher and Macaulay Duration will be lower.

For example, assuming that the face value of a bond is Rs 1,000, coupon rate of 10%, YTM of 10%, and maturity of 5 years, the Macaulay Duration of a bond will be as follows:

A higher Macaulay Duration indicates a higher sensitivity to interest rates and vice versa. If you match your investment horizon to the Macaulay duration of a scheme, you could effectively eliminate the interest rate risk from your investment.

What is Modified Duration and why it is important?

Fund managers of debt mutual funds use a concept called Modified Duration to assess how much a debt portfolio is likely to fluctuate in response to changes in interest rates. For instance, if the Modified Duration of a debt scheme is 5 years, if the interest rate increases by 1%, then the value of the portfolio will fall by 5%.

Modified Duration is calculated as:

= (Macaulay Duration)/[1+YTM/Number of coupon period per year)]

In the above example, Macaulay’s Duration is 4.17 years, considering YTM of 10% and frequency of coupon payment as 1 per year, the Modified Duration will be 3.79 years.

A portfolio with a low modified duration implies that the returns are mainly from accrual income rather than capital gains. Whereas a portfolio with a high modified duration implies that returns are mainly generated from capital gains.

If a fund manager expects the interest rates to rise, he/she would reduce the modified duration of the portfolio to reduce the risk of volatility in the value of the portfolio. Alternatively, if the fund manager expects interest rates to fall, he/she will maintain a portfolio with a high modified duration to benefit from the rise in bond prices.

As an investor, you too can mitigate interest rate risk in your portfolio by shifting to a scheme with a low modified duration of up to 2-3 years when interest rates are rising. Similarly, you can consider gradually shifting to schemes with a high modified duration of 3-5 years or more when interest rates have peaked or are expected to fall.

Conclusion

The Average Maturity, Macaulay Duration, and Modified Duration can offer valuable insights on the duration strategies adopted by fund managers. It also helps you to determine the sensitivity of the scheme with respect to changes in interest rates.

A clear understanding of these concepts can help you to build a suitable debt portfolio to reduce the impact of interest rate risk. You can easily get this information from the scheme-related documents of the respective schemes.

Lastly, remember that even in the case of debt funds, higher returns are usually associated with higher risk, which makes it important to choose schemes carefully.

Disclaimer: The views expressed here in this Article / Video are for general information and reading purposes only and do not constitute any guidelines and recommendations on any course of action to be followed by the reader. Quantum AMC / Quantum Mutual Fund is not guaranteeing / offering / communicating any indicative yield on investments made in the scheme(s). The views are not meant to serve as a professional guide / investment advice / intended to be an offer or solicitation for the purchase or sale of any financial product or instrument or mutual fund units for the reader. The Article / Video has been prepared on the basis of publicly available information, internally developed data and other sources believed to be reliable. Whilst no action has been solicited based upon the information provided herein, due care has been taken to ensure that the facts are accurate and views given are fair and reasonable as on date. Readers of the Article / Video should rely on information/data arising out of their own investigations and advised to seek independent professional advice and arrive at an informed decision before making any investments. None of the Quantum Advisors, Quantum AMC, Quantum Trustee or Quantum Mutual Fund, their Affiliates or Representative shall be liable for any direct, indirect, special, incidental, consequential, punitive or exemplary losses or damages including lost profits arising in any way on account of any action taken basis the data / information / views provided in the Article / video.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.