As of May 2021, the markets might be looking attractive due to renewed optimism concerning falling Coronavirus cases and earnings upgrade from Indian companies. On the other hand, several rating agencies have downgraded India’s GDP forecast and outflows from Foreign portfolio investors amounted to $1.5 billion in April 2021. How do you respond during such market uncertainty? Do you try to book profits when the market is high or do you buy and hold? An ideal investing strategy is one where you can invest in a bear market and redeem when it is bullish. However, this is easier said than done. We evaluate the three reasons why market timing can best be avoided:

-

Requires minute attention to monitor investments:

If you follow the financial market on a daily or weekly basis, it can be quite difficult to manage along with your personal and professional commitments. -

Consistency of making a right guess is not easy:

It is difficult to predict the market. Most big market gains and losses could be concentrated in short periods, wherein an untimely exit could ruin your long-term returns. -

Could be detrimental to your long-term goals:

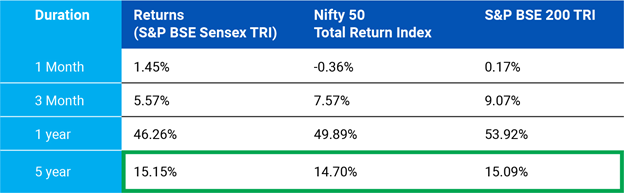

We all know that market movement are mostly unpredictable in the short run. The risk of downside could be offset in the long run. Check the table below to see how the returns tend to be more attractive with time.

Table 1: Market volatility in 1 month, 3-month, 1 year and 5 year period

Past performance may or may not be sustained in the future.

Data as on April 30, 2021.

Returns are net of total expense and are calculated on the basis of Compounded Annualized Growth Rate (CAGR).

Source: BSE Sensex, Nifty 50 Index and S&P BSE 200 TRI.

So what could be your approach to market uncertainty?

-

Assess your risk appetite: if you are risk-averse and unable to bear huge fluctuations in your equity portfolio, then consider allocating less proportion of your investable funds into equity mutual funds and a greater chunk of your portfolio in debt.

-

Determine your investment duration: Consider your investment duration. A time horizon of less than 3-5 years can be considered as a short-term goal, whereas anything above 5-7 years can be considered medium- to long-term goals. This clear demarcation of your investible corpus can keep you from redeeming from your long-term investments to meet short-term expenses.

-

Devise an asset allocation plan and rebalance periodically

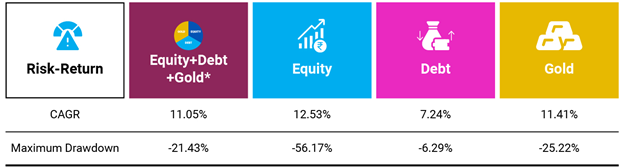

Since financial assets such as equity, debt and gold are cyclical, predicting the next best asset might be a futile exercise. If you see in the table as illustrated below, investing heavily in one asset class has potential downside risks (see maximum drawdown). In such a scenario, it makes sense to devise an asset allocation plan with due weightage given to all assets, thereby reducing your downside risk. You could then periodically reassess your asset allocation strategy and bring the assets to their original intended allocation. For a simple and easy approach to asset allocation, it is suggested to first set aside 6-24 months of monthly expenses as ‘safe money’ in a liquid fund to act as your emergency fund and the balance of your money in Equity and Gold in the 80:20 ratio.

The illustration below uses the 40-20-20 allocation to Equity, Debt & Gold.

Table 2: Asset allocation delivers a better risk-adjusted return

The Time frame is November 2004 to April 2021. The period is taken from 2004 since the asset allocation weights are calculated based on normalizing the historical monthly equity and debt indicators. Given the normalization time frame used in the strategy, data availability for certain parameters beyond the time frame analyzed was a constraint. Compiled by Quantum AMC. *Equity-Debt-Gold ratio is 40-40-20.

Source: Sensex TRI, Crisil Composite Bond fund index, and Domestic Gold Prices

Past performance may or may not be sustained in the future

- Start an SIP to take the rupee cost averaging benefit

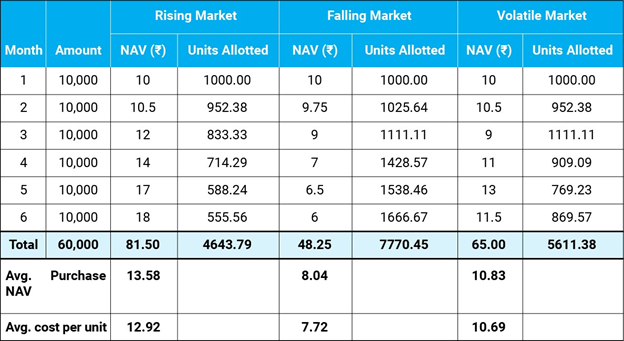

An SIP (Systematic Investment Plan) is one of the better routes to average your cost of mutual fund investments over the long term. As seen in the table below, SIPs allow you to buy more units when markets are low and lesser when markets are rising. This makes your investments more cost-efficient and negates the need to time the market.

Table 3: Rupee cost averaging benefit

The above table is for illustration purposes only. Investments through SIP is subject to market risk and do not assure a profit or returns or protection against a loss in downturn market.

The above table is for illustration purposes only. Investments through SIP is subject to market risk and do not assure a profit or returns or protection against a loss in downturn market.

Thus, in the end, it is not market timing, but a staggered investment approach coupled with a good asset allocation strategy in tandem with your risk profile and time duration at hand that can help achieve your financial goals.

Disclaimer: The views expressed here in this Article / Video are for general information and reading purpose only and do not constitute any guidelines and recommendations on any course of action to be followed by the reader. Quantum AMC / Quantum Mutual Fund is not guaranteeing / offering / communicating any indicative yield on investments made in the scheme(s). The views are not meant to serve as a professional guide / investment advice / intended to be an offer or solicitation for the purchase or sale of any financial product or instrument or mutual fund units for the reader. The Article / Video has been prepared on the basis of publicly available information, internally developed data and other sources believed to be reliable. Whilst no action has been solicited based upon the information provided herein, due care has been taken to ensure that the facts are accurate and views given are fair and reasonable as on date. Readers of the Article / Video should rely on information/data arising out of their own investigations and advised to seek independent professional advice and arrive at an informed decision before making any investments. None of the Quantum Advisors, Quantum AMC, Quantum Trustee or Quantum Mutual Fund, their Affiliates or Representative shall be liable for any direct, indirect, special, incidental, consequential, punitive or exemplary losses or damages including lost profits arising in any way on account of any action taken basis the data / information / views provided in the Article / video.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.