Investors spend a lot of time worrying about the equity part of the portfolio and don’t nearly pay enough attention to the debt portion. But you should be just as careful when building your debt portfolio.

A few things to keep in mind;

Don’t worry about chasing returns in your debt portfolio, that’s what you invest in equity for. When it comes to debt, the return of capital is more important than the return on capital.

Understand the two important risks in debt funds:

-

Interest rate risk

-

Credit risk or default risk

This thread explains what interest rate risk is. Just to reiterate, debt funds and interest rates have an inverse relationship. When interest rates rise, NAVs fall, and when interest rates fall, NAVs rise.

https://twitter.com/ZerodhaVarsity/status/1523665845029064705

How much will the NAVs rise and fall?

As explained in the thread, this is where the concept of modified duration comes in. You can check the modified duration of a fund in its fact sheet. The higher the duration of a fund, the more volatile it is and the higher its sensitivity to interest rate changes. Here’s an example of the volatility of short, medium and long duration funds.

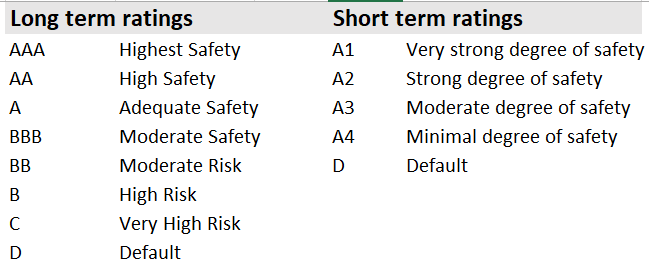

Credit risk or default risk is the risk of you losing your money. Debt funds hold individual long-term and short-term bonds. Every bond has varying levels of risk and this is denoted by a credit rating, here’s the rating scale of CRISIL.

Every debt fund discloses its portfolio fortnightly. You can check the underlying portfolio to get a sense of how risky the fund is. Periodically reviewing the portfolio of a debt fund is important. Lower the credit rating, the higher the “potential” return but higher the risk.

When you are building your debt portfolio, you should always take interest rate risk and credit risk into account. You can invest in longer-duration funds as long as you understand how interest rate cycles work and that they can be volatile. But if you don’t have the stomach for interest rate risk, then you can stick to short-term funds or funds with lower duration. The duration range for each category is clearly defined.

Chasing returns in debt funds is a bad idea. Investing in funds with higher credit risk without understanding that high returns come with a higher chance of loss of capital can lead to mishaps. We saw this during IL&FS and DHFL crises.

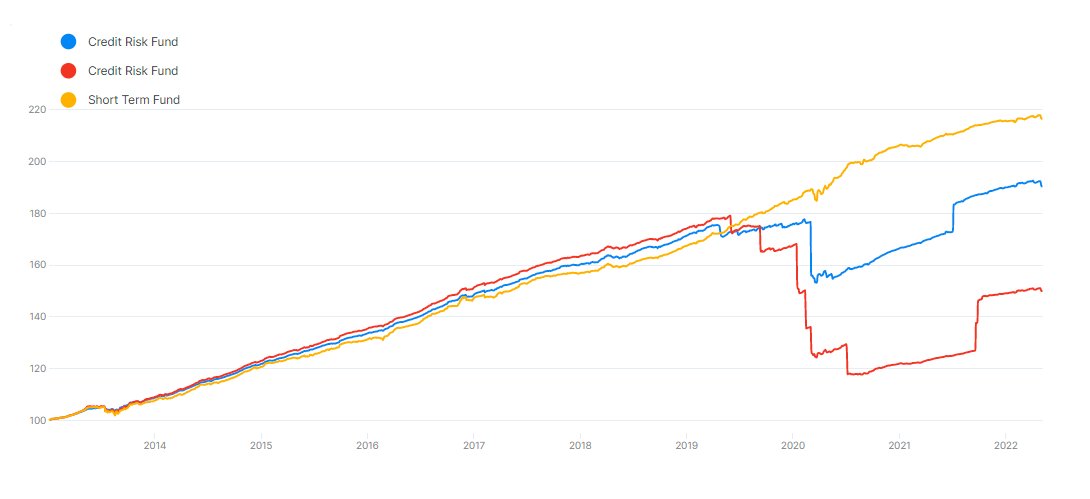

Most funds with higher credit risk, like credit risk funds, haven’t exactly delivered in India. Their returns on 5 to 10-year periods are on par or less than much safer funds. When things go bad, you’ll lose most of your investment. Here are two examples vs a short-term fund.

Retail investors are better off avoiding risky funds and funds with higher credit risk. The risk to reward rarely makes sense. Stick to funds with high exposure to G-Secs, State development Loans (SDLs), and AAA-rate papers.

Another recurring mistake investors make is assuming that gilt funds are totally safe. Gilt funds only hold government bonds and there’s no credit risk. But most gilt funds hold long maturity G-secs and have a very long duration, and they have a high-interest rate risk.

The reason why investors ignore debt funds is that there are 16 categories of debt mutual funds. But the best thing you can do is first understand the basic concepts like interest rate risk, duration and credit risk.

This will make things much, much simpler when choosing debt funds. We highly recommend you check out the Varsity chapters on debt funds;