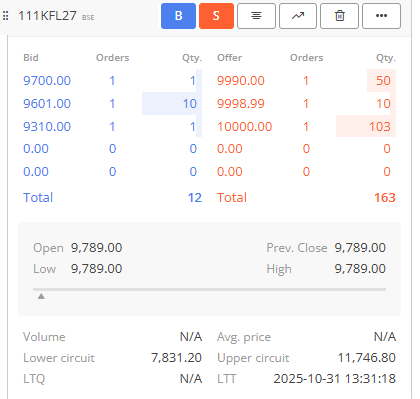

On Kite, the price will depend on demand and supply. On Coin, the amount blocked for G-secs is the estimated weighted average rate of all allotments to competitive bidders + accrued interest + markup value (difference between the lowest and highest bid).

Bonds and other approved liquid instruments are treated like cash, so you can use them to meet your entire margin requirement without paying any interest.

Equity, however, is considered non-cash collateral. Here, the 50:50 rule applies at least half of your margin must come from cash. If you don’t maintain that cash portion, interest will be charged on the shortfall.

Any idea what is the difference if I buy it directly from Zerodha instead of goldenpi or wintwealth? If I buy through say goldenpi, i know its maturity, interest payout timelines. How does the interest payout work (which dates) if i directly buy it via zerodha?

maturity or interest payment dates for bonds are fixed at the time of issue, and remains same throughout bonds tenure.

So for a particular bond, dates and all relevant details remains same regardless of where you buy it from.

A big difference though maybe liquidity (at least for buying). Most of these bonds are pretty illiquid and you might not get a seller available on exchange at required price.

These platforms like goldenpi / wintwealth used to do some kind of market making (matching buyer / seller or getting a big chunk from issuer and selling it to retailers at fix price)

So availability might be slightly better on some platforms.

One big caveat

Do not blindly trust yield numbers shown by these platforms. Calculate yourself and confirm what they are indicating.

In past I have a seen a case with paytmmoney, where they did a mistake in calculations, and arrived at YTM of 38% per year, and people happily bought it assuming they are going to get 38% interest a year.

In reality what they bought was not even going to cover the buying price they paid.