NOTE: Sharing first impressions based on limited info from the details in the original post and the shared LLM-chat . Please correct any incorrect assumptions and share additional details for further relevant discussions.

With 70K monthly-expenses from a monthly-income of 1.3L,

for a couple with an infant,

(i.e. presumably one hasn’t even hit one’s peak expense yet,

which is expected over the next 2 decades),

the 40L asset/cash appears to be extremely critical

and sufficient parts of it must be liquid at key points of time in future,

to avoid missing the key goals in future.

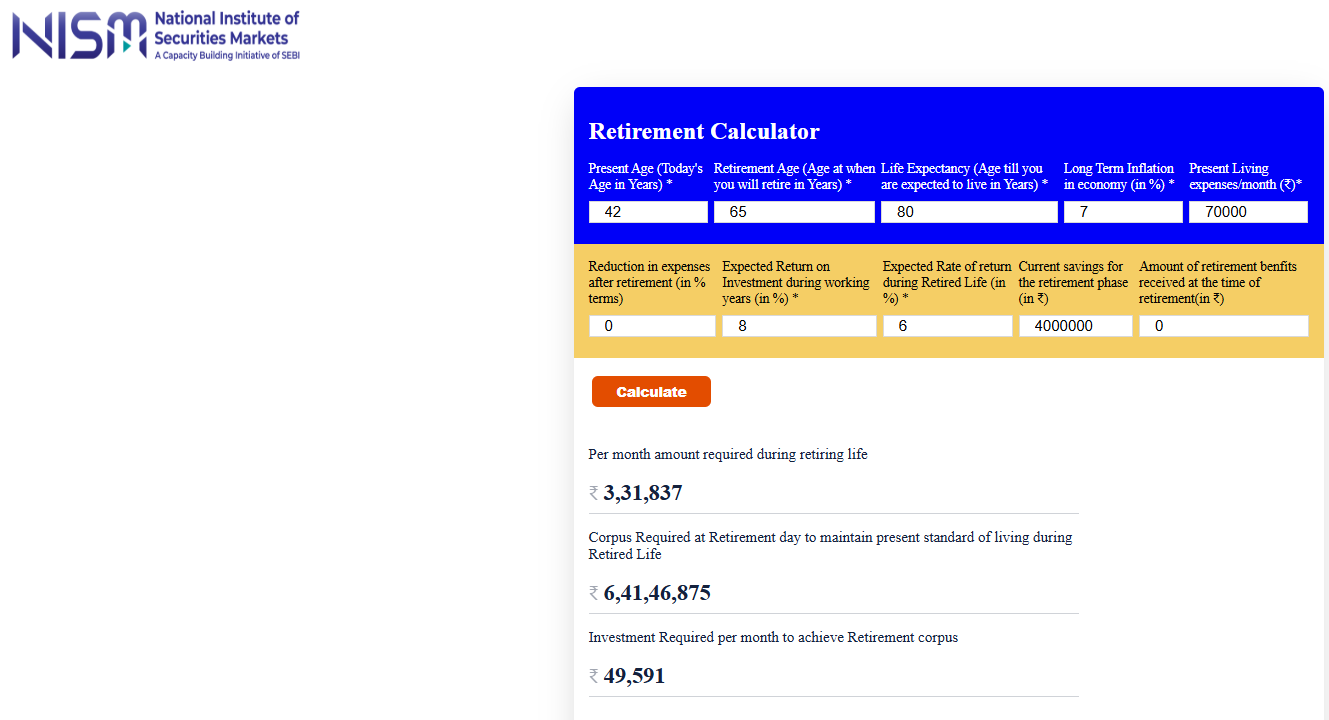

a. Are you aware of the various generic assumptions made by the retirement calculators you used?

b. Do they match your own planned lifestyle choices (now and in the future)?

c. When do you intend to retire? (in the LLM-chat it is mentioned 65)

d. Over the years, has physical / mental fitness been taken care of (and is still being taken care of) to be productive till you are 65 years of age?

e. Are you confident of being gainfully employed to completely cover your expenses and investments till you retire (till 2047?) ?

f. Are there any other reliable/guaranteed sources of income? (regular/sporadic? in-future?)

IMHO, while financial planning, folks are usually optimistic,

i.e. the worst-case assumptions are not worse enough.

Thus, there is less of a buffer against unforeseen situations.

For example, a bunch of typical expenses are not discussed in the LLM-chat shared.

Not sure if those expenses do not apply (due to specific lifestyle choices),

or if not accounting for them is an oversight.

A list of few potential sporadic expenses...

| Category |

Example Expenses Not Explicitly Covered in the LLM-chat |

| Children’s Education |

College, coaching, study abroad, extra-curriculars |

| Children’s Marriage |

Wedding, gifts, ceremonies |

| Home |

Purchase, major repairs, taxes, interiors |

| Vehicle |

New car, major repairs, insurance gaps |

| Health |

Dental, vision, long-term care, mental health |

| Family Support |

Parents’/siblings’ needs, emergencies |

| Legal/Compliance |

Legal fees, tax penalties |

| Lifestyle |

Gadgets, hobbies, festivals, gifts |

| Travel |

Domestic, emergency, other international trips |

| Inflation |

On any unplanned or under-budgeted item |

| Children’s Misc |

Special needs, gadgets, tuition, school trips |

| Insurance Gaps |

Exclusions, premium hikes, critical illness |

| Retirement Upgrades |

Relocation, hobbies, lifestyle changes |

| Miscellaneous |

Fraud, disaster, litigation, regulatory fines |

| Technology |

Subscriptions, online learning, device upgrades |

| Professional |

Certifications, conferences, career change |

| Business |

Side hustle losses, seed capital |

| Pets |

Vet care, food, emergencies |

| Social/Community |

Donations, community events, religious functions |

| Government/Regulatory |

Renewals, fines, compliance |

| Aging Parents |

Elder care, funeral costs |

| Children’s Opportunities |

Competitions, exchange programs |

| Relocation |

Job transfer, emigration, moving costs |

| Personal Emergencies |

Divorce, rehab, legal fees |

| Asset Replacement |

Appliances, electronics, home goods |

| Security/Safety |

Home security, cyber protection |

| Environmental |

Water/air solutions, disaster recovery |

| Legal/Inheritance |

Will, inheritance settlement |

| Miscellaneous |

Lost items, unplanned celebrations |

| Children’s Entrepreneurship |

Seed funding, creative projects |

| Uninsured Damages |

Rental/property damage, liability |

| Taxation Surprises |

Capital gains, gift tax |

are all of these already accounted for

- either in the “average monthly expense” ?

- or in the “emergency fund” ?

How many of these expenses need to occur

simultaneously / close enough to each other in time,

to end-up depleting the monthly-expense + emergency-fund,

and force one to dip into other investments,

at the risk of derailing the long-term “financial plan” that we have come-up with so far? -

2? 5? 10?

Also, thinking of this as a dichotomy (only 2 choices) will incorrectly force one to either

- Settle for less risky investment options with fairly predictable liquidity.

- and guarantee missing some(all?) of the goals.

or

- Settle for more risky investment options (higher volatility? less liquidity?)

- and face a higher likelihood of NOT being able to achieve one’s goals.

A third choice is to limit/avoid expenses, especially lifestyle inflation.

- Doing this earlier can be more rewarding, due to compounding of investments over time.

- Doing this enables one to tweak one’s investments (to achieve one’s future goals)

towards instruments with higher likehood of success.

Depending on the number of uncertainties involved,

that one is unable to rule-out,

IMHO, it sounds prudent to affect a change in the lifestyle now to reduce expenses,

and calculate a revised investment strategy

that achieves the same returns as what one already had in mind,

but with a better chance of success.

One of the major challenges with using LLMs is they are like Suppandi from Tinkle, often taking statements too literally and ignoring even basic assumptions (that humans usually make) if such assumptions are not explicitly specified in the instructions.

We can leverage LLMs themselves to highlight a few actual instances of this!

Try continuing the LLM-chat shared above with the following prompt -

"Prepare a comprehensive list of all potential scenarios

in which the above plan will fail to achieve

(or will only partially achieve)

one or more of the goals."

For example,

IIUC, one such potential issue is

not accounting for the 2nd child’s education.

The LLM appears to have interpreted the following prompt…

give me in charts ur financial structure and planning … for …

…

2. Child Schooling

3. 2nd Child.

…

…to mean - “Plan for educating the first child and the birth of a 2nd child.”

Thus, it looks like the proposed financial plan shared by the LLM,

ignores finances required for the 2nd child’s education.

Right?

Source: Section '5. Goal-Specific Risks' of a follow-up LLM-chat.

Few potential scenarios in which the proposed financial plan may fail to achieve (or only partially achieve) one or more of the stated goals.

1. Market-Related Risks

- Prolonged Bear Market or Low Returns:

If equity markets underperform for a decade or more (e.g., <7% CAGR), your ₹30L STP and SIPs may not compound enough to reach the ₹6–7 crore retirement target.

Partial achievement: Retirement corpus may fall short, requiring lifestyle adjustments or delayed retirement.

- Sharp Market Crash Early in STP:

If a major crash happens in the first 12–18 months of STP, a large portion of your ₹30L may be invested at high NAVs, reducing long-term returns.

- Debt Fund Defaults or Credit Events:

If the liquid/short-term debt funds used for STP or buffers face credit events, you could lose capital or face delays in accessing funds for short-term needs.

2. Inflation Risks

- Higher-than-Expected Inflation:

If education, healthcare, or travel costs rise faster than assumed (e.g., >8%/year), your earmarked buffers (₹5L for schooling, ₹12k/month SIP for Europe) may be insufficient.

- Lifestyle Inflation:

If your expenses rise faster than your income (e.g., due to lifestyle upgrades, private schooling, etc.), your surplus for SIPs may shrink, reducing long-term corpus.

3. Income & Employment Risks

- Job Loss or Salary Stagnation:

If you or your wife lose your job, or if salary increments are lower than expected, you may not be able to maintain the ₹30k/month SIP or replenish emergency funds after a drawdown.

- Forced Early Retirement or Health Issues:

If you are forced to retire early due to health or job market changes, the corpus may not be sufficient.

4. Expense Shocks & Life Events

- Major Health Emergency Exceeding Insurance:

If a health event costs more than your insurance + emergency fund (e.g., rare illness, long-term care), you may need to dip into retirement or education funds.

- Second Child Complications:

If delivery or neonatal care costs are much higher than planned, or if insurance does not cover certain expenses, you may need to use more of your buffer, impacting other goals.

- Multiple Large Expenses in Short Succession:

If schooling, health, and travel needs coincide (e.g., in the same year), your buffers may be depleted, forcing you to redeem long-term investments early (hurting compounding).

5. Goal-Specific Risks

- Child’s Schooling Costs Underestimated:

If you opt for a more expensive school, or if fees rise sharply, the ₹4L buffer and annual surplus may not be enough.

- Europe Trip Cost Overruns:

If the rupee depreciates, or travel costs spike, the ₹12k/month SIP may not be enough for a family of four.

- Second Child’s Education/Needs:

If you have a second child, future education and other costs will double, but the plan only earmarks for one child’s schooling and SSY.

6. Liquidity & Access Risks

- Lock-in or Redemption Delays:

If you need funds urgently (e.g., for health or schooling) but they are in funds with exit loads or redemption delays, you may face a cash crunch.

- Taxation Changes:

If tax laws change (e.g., higher tax on debt/equity funds), post-tax returns may be lower than planned.

7. Behavioral & Execution Risks

- Discipline Lapses:

If you skip SIPs, redeem funds early, or fail to top-up SIPs as income grows, corpus targets will not be met.

- Overconfidence or Panic:

If you panic during a market crash and stop STP/SIP or redeem equity, you lock in losses and miss the compounding benefit.

8. Other Unforeseen Events

- Regulatory or Policy Changes:

Changes in mutual fund regulations, PPF/SSY rules, or capital controls could impact liquidity or returns.

- Family Emergencies or Obligations:

Extended family support, legal issues, or other obligations could require large, unplanned outflows.

Summary Table

| Scenario Type |

Example Failure Mode |

Impacted Goal(s) |

| Market Risk |

Prolonged low returns, early crash |

Retirement, Europe trip, all |

| Inflation Risk |

School/travel/health costs rise faster than planned |

Schooling, Europe, health |

| Income/Job Risk |

Job loss, salary stagnation |

All (esp. SIPs, buffers) |

| Expense Shock |

Major health, 2nd child complications, multiple events |

Health, schooling, all |

| Goal-Specific |

Underestimated costs, 2nd child not planned for |

Schooling, travel, retirement |

| Liquidity/Access |

Redemption delays, tax changes |

All (esp. emergencies) |

| Behavioral/Execution |

Skipped SIPs, panic selling, lack of top-up |

Retirement, all |

| Unforeseen/Regulatory |

Policy changes, family obligations |

All |

Key Takeaway

The plan is robust for “expected” scenarios, but will only partially achieve or may fail for one or more goals if:

- There are multiple large, unplanned expenses,

- Market returns are much lower than expected,

- Income does not grow as planned,

- You are unable to maintain discipline or adapt the plan as life changes.

Regular review and flexibility are essential.

Another major issue with using LLMs is that they are sycophantic by design. For example, while financial planning in an LLM-chat, we need to constantly ensure that the false praise by the LLMs in the chat, (eg. equating basic follow-up Qs to “great catch”, “thinking like a family CFO” in the shared LLM-chat), does not limit us into thinking that we are anywhere close to a decent financial plan.