I have observed that average slippage for market orders is 0.3%. Also, while roll over of future contracts, every time there is 0.5% loss. There losses are huge if average winners last for more than 12 months. Is it possible to reduce this loss?

Have you checked Iceberg orders? You can use this when placing market orders to reduce slippage.

Rollover, there is no way around; the costs will eat up your returns over time. If you are taking long term view best to take position in the farthest most liquid contract.

Will using the clone feature in basket orders achieve the same reduction of impact cost like iceberg orders? Since I couldn’t find the iceberg option while placing orders in basket.

With clone using a basket, you are still firing multiple market orders simultaneously, which doesn’t help reduce impact cost. With Iceberg, a large order is fired in smaller parts, but most importantly, every subsequent part is fired only once the previous is executed. Thus reducing the impact cost.

2 Likes

Sir… if possible, can you provide SPREAD ORDER in KITE for ROLLOVER future contracts… SPREAD ORDERS help in reducing slippage…

1 Like

How will spread orders reduce slippage for rollover if you already have an existing open futures contract?

Sir… the sole purpose of SPREAD ORDER is to rollover index or stock futures contracts as SINGLE ORDER is required for an exit open position and initiate a fresh position in next month’s future contracts…for example, if I have an existing open October month long Nifty future contract then I have to first exit that long position and then place a fresh buy order for the November month Nifty future contract and this rollover process will take at least 4-5 seconds which can easily increase impact cost (not necessarily every time but it could)…But in SPREAD ORDER I have to just place a bid for the PREMIUM DIFFERENCE between both contracts and when it gets traded my position automatically gets rollover…last year also I tried to bring notice in front of you sir…I am also tagging you today in last year’s thread about my demand

@MohammedFaisal can you respond? I don’t think there is any marked improvement in terms of improving price since the spread we see is based on the combined market depth of Oct’s Best Bid and Nov’s Best Ask. This is essentially as good as exiting one and entering the other immediately?

+1.

You can ensure instant execution of both orders in a rollover using basket orders on Kite.

Concerning placing the order by entering the premium difference, you can set Limit orders by looking at the market depth when you are adding the contract to the basket.

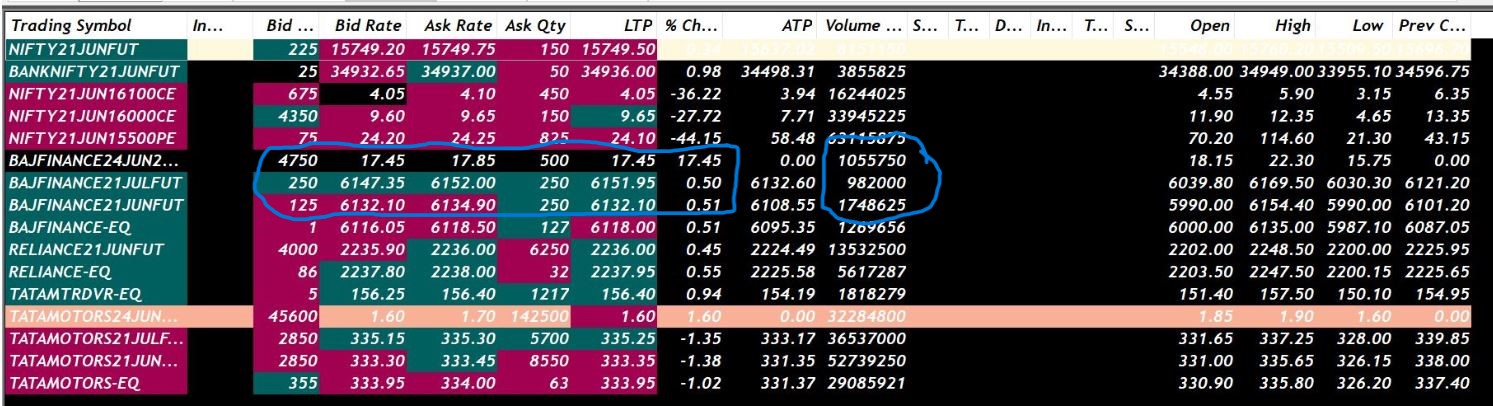

In INDEX FUTURES… there is no issue in using basket order features of kite for an instant order execution by placing not just limit orders but even market orders can be used without any significant slippage for rollover as there is enormous liquidity in nifty banknifty… but the problem lies in the rollover of STOCK FUTURES where market orders give high slippage (at least 300-400 rs. per lot) and limit order does not always guarantee execution as there is always a chance of getting one leg of basket order getting executed and other order can remains pending and that’s where SPREAD ORDER can be used… as they ensure simultaneous execution of both months contract with marginal improvement in terms of pricing… I am attaching last year June July month rollover spread order of BAJFINANCE screenshot where you can see marginal price improvement in Spread order bid and ask compare to actual future bid and ask

@nithin @MohammedFaisal

No plans as of now. 1 iceberg can potentially lead to many smaller orders, and allowing this through a basket could mean exponentially more load on our systems.

2 Likes