If possible, only if it not intrusive, could you at a broad level let us know your version.

Don’t use plan B. Invest in your kids like most Indian parents. ![]()

![]()

Probability wise looking at her conversation history she will be angry/upset for this statement.

Agree. Understand your viewpoint

That’s exactly original query … what can be plan B or C ?

I also do not have an answer for it. so Trying to find out what I can do, in order to ensure plan A does not fail.

Agree with the second part that complexity can be overkill and like most other things in life like simple strategy wins most of the time.

However, when I am at retirement, the first part needs to be relooked.

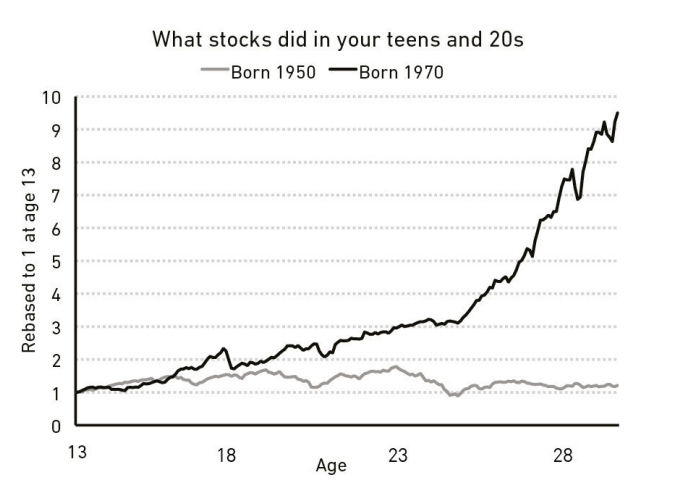

This is a graph from psychology of money which tells how “inflation adjusted” US stock market behaved in different time periods.

Experts may disagree but there is no assurance that it may not happen in India for an extended period of time. or how Japan stock market moved… There can be black swan effect.

What I am simply saying is that once I am retired the risk tolerance goes down .and that’s what the original question is.

Agree. Multi Asset portfolio and periodic rebalancing is not designed to beat the best performing asset in that year. It will never be.

It just ensures that drawdown is capped. and again it works best if complexity in decision making about asset allocation is removed.

It is supposed to reduce fluctuation

Ok… I do not have any patented secret! however now I think the thread should be moved to “personal finance” from “Versity” ![]()

![]()

Although its not rocket science, trying to give a bit of a detailed explanation so that I can get feedback on where I can improve…

it might test your attention span though !

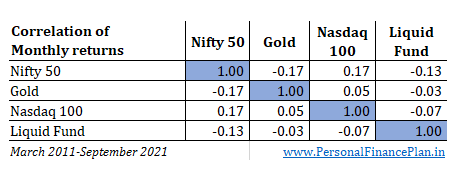

fundamentally I wanted to build retirement portfolio or part of it using asset classes which are uncorrelated (as far as possible) to minimize drawdowns and maximize returns

This table indicates (one way) to achieve a point of minimum variance.

Effectively start with an equal proportion of all four components

- Nifty

- US NASDAQ

- Gold

- Liquid

and re-balance every year once. (while withdrawing money from kitty)

However, I do believe in India’s growth story , and wanted to ensure NIFTY has more weightage to be on efficient frontier. Its possible to allocate more % to nifty but it (slightly) complicates rebalancing.

So my current retirement portfolio looks like equal weight of

- Nifty index

- Nifty Next 50 index

- 200 Momentum 30 index

- Low volatility index

- Gold index

- US Total market index

- Medium duration debt fund

- Liquid fund

And aim is to rebalance every year to have exactly the same amount in every class. Esp while withdrawing.

Selected momentum and volatility index as intuitively (haven’t calculated) they seem to have low co-relation with each other. no particular resoan to select Next 50. I could have selected two different nifty index to ensure equal distribution.

Is it the only way?

There are may ways to skin the cat, e.g. Probably alpha index would have been better fit than momentum index.

Does it work?

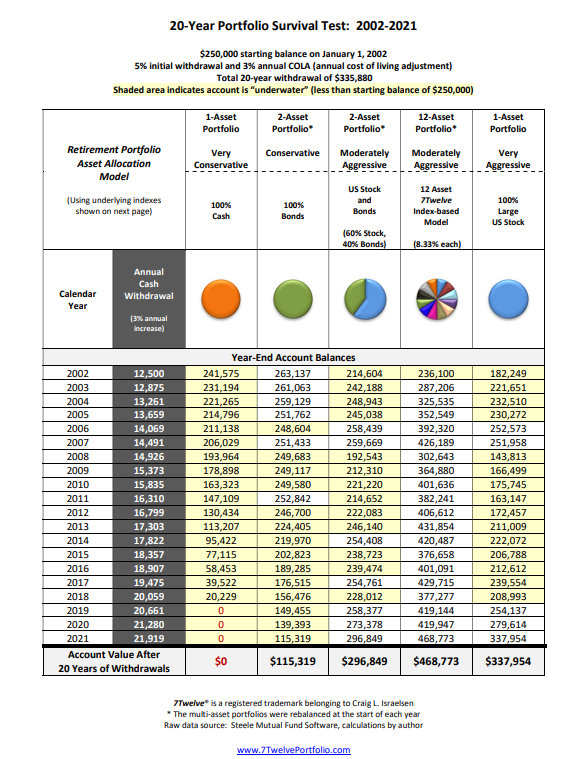

When we are withdrawing… less drawdowns seems to help in preserving capital.

The 7/12 study shows asset diversification “and” rebalancing helps in preserving capital .

100 % Nasdaq equity only portfolio gave 9.52 % returns during study period and 7/12 diversified portfolio gave 7.76% returns

However, something strange happens when you are withdrawing every year from kitty.

After 20 Years of Withdrawals balance Value is less for equity only portfolio than diversified portfolio.

What is magic here?

Its because lower drawdown combined with sell high strategy helps lower erosion of capital (with respect to single asset portfolio.)

Even after inflation adjusted 4% (any fixed number) withdrawal every year , my capital is increasing irrespective of economic cycle/phase. This will ensure that I don’t have to make decisions when I am in my 80s or 90s… Its like buying annuity plans but far greater returns.

I think this what my expectation from retirement fund,

Questions/Feedback/comments/suggestions welcome !![]()

Portfolio allocation + re balancing i think is the best one can do passively. There is no magic solution. Going further, You can try to test it out and see what works well. Long term gilt may have a place in portfolio too as they can sometimes have inverse correlation with equity. And probably don’t use them when rates are absurdly low.

After that either you need to be active, which is risky as most fail. Or perhaps use your skills from life so far and have some low effort way of making money that is also interesting to you and that can take care of managing expenses until you cant/don’t want to work. Also we can try to save more. If you need say 1 cr to retire but save 2 or 3 or x cr, it will be much easier.

For me answer is trading. For now its plan a b and c. Diversification is only within trading. Retirement for me probably will mean stopping intraday completely and shifting to low frequency low effort trading along with some diversification to other assets like you said.

That’s why you should have gold, not debt fund/FD. Bonds are rich peoples asset. The rich has 28% of portfolio as bonds. Majority of these HNI’S , VHNI’S have gsec bonds. See when things go to hell they know central bank goes to secondary market and starts buying those 10 year yeilds which increases bond price. So the rich can one earn interest income and secondly can easily exit when QE is in motion. Now you are probably wondering , why we can’t do? Well the standard lot in CCIL bond market is 5Cr, I certainly don’t think 28% of your holdings won’t come to minimum 5Cr.

I suggest to use gold as hedge. Always have minimum 10% of gold as portfolio. Goldbees ETF recommended!

FD’s are good cash flow, you can manage food expenses and to an extent clothes. As far others I can’t quantify whether it will pay for energy, because energy is the big elephant(petrol ,diesel, gas , electricity) .

Thirdly as finance with sharan says:-

Income generation comes from :-

-

60% - 70%. From salary

-

30% - 40%. From portfolio investments

So as soon as you retire I certainly don’t think any corpus can replace 1 with existing lifestyle expenses. Taking risk in equity makes no sense either. I guess sure you can sustain initial 5 years but certainly degrades over time. The key is being frugal here and really is needed because c’mon you are 60 just retired and can’t have desires like buying new car, costly Marriage for kids or cousins, helping xyz relatives, constructing new house , giving costly gifts!. Your goal is to sustain for rest of the life with the corpus you have.

Note :- only for salaried individuals that are only willing to work till retirement

Plan B:- sending your kids to aboard and living with 700$ per month sent by them.

Plan c:- start tea shop, taking chance in politics , food bussiness

Plan D:- make costly Marriage for kids screw your corpus retirement funds by being stupid and then die of heart attack or ailment!

Note:- these are what I see in my place or you can say what boomers are doing so far doing. Funny these ppl mostly choose plan B or plan D.

K got you ![]()

Thanks for the suggestion. I wasn’t very happy with my own selection of ““Medium duration debt fund” as asset. Would slowly change to long term gilt as asset.

Debt funds are always puzzle for me… but will do due research to zero down what I think can be treated as long term govt debt index.

These words should be inscribed in gold! Very important life advice.

Lifestyle inflation eats everything. If I am using car, I still need to change car after every 15 years. I will need driver even if I have self-driven for life. It’s important that mentally we accept to choose lower version of hatchback instead of premium sedan or SUV.

![]()

![]() secret wish of every Indian parent!

secret wish of every Indian parent!

I remember in my village, every young man used to go Mumbai to earn money. Idea of earning money is to work in cotton mill in three shifts so that in dipawali they can buy new cloths every family member!!

1 Like

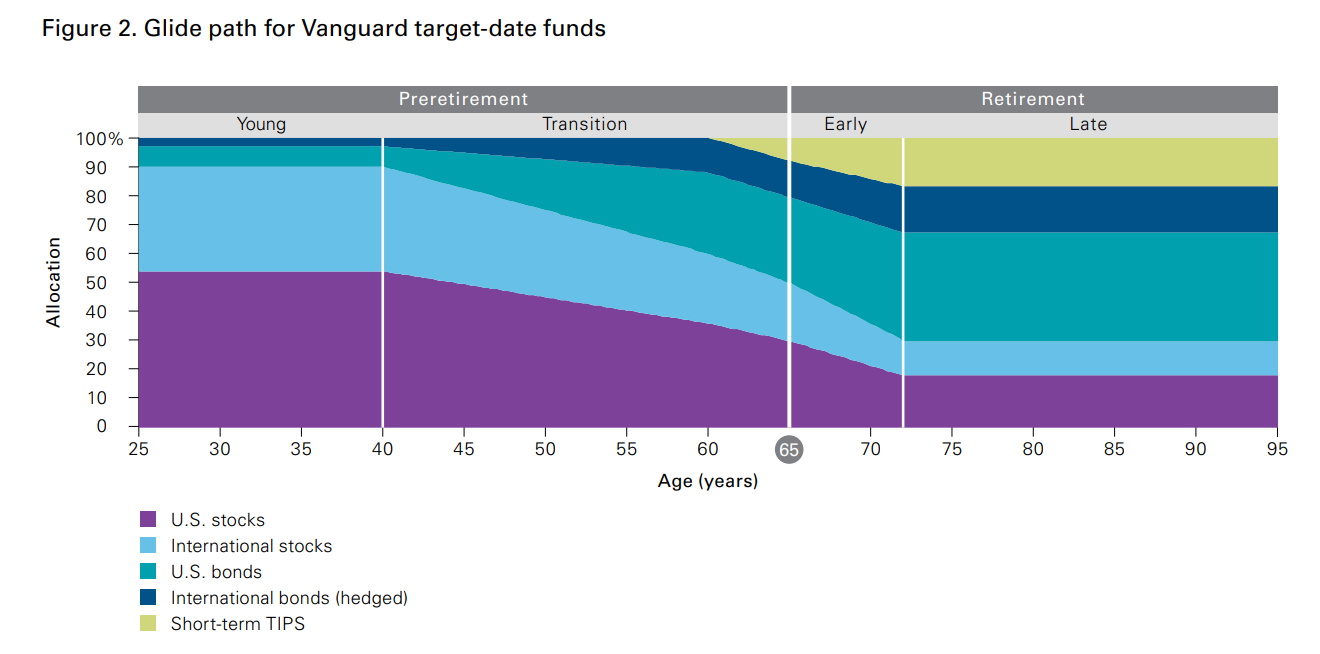

What you are talking about is called “sequence risk.” The scenario you mentioned will be a problem if you are 100% in equity, which isn’t a good idea when you are retired. It’s always better to gradually de-risk your portfolio as you age by decreasing equity exposure and increasing debt/fixed income exposure.

But this isn’t a solution to bad luck. Assuming that you aren’t sufficiently prepared for your retirement, the only solutions are:

- Spending less

- Working longer or generating some sort of side income

- Monetizing assets through reverse mortages etc

But in general, if you are still working, it better to expect less and save more. Being over prepared never hurts.

https://www.morningstar.com/articles/1111313/sequence-risk-during-retirement