Effect of reduction of intraday leverages in the near term

Trading volumes are bound to dip. Almost 50% of all trading on the exchanges are from retail traders and investors and the majority of that is intraday trade. Even in the non-retail bit, there would be some effect of this. Today March 15th was quite a volatile day but at Zerodha our trading volumes compared to a similar kind of day pre-March were at least 20% lesser.

When trading volumes dip, the impact cost goes up. Impact cost is how much you lose to the market when you place a market order due to the bid-ask spread. The problem with impact cost going up is that it can have a snowball effect. Impact cost increasing further reduces trading volume and hence making the impact cost even larger. Trading volumes or liquidity being lesser also means that markets tend to move in a jagged fashion - sharp moves up and down due to large orders being placed. I guess we are already starting to see this happen and will take some time for the markets to adjust. So yeah, near term pain for Exchanges, Brokers, and traders.

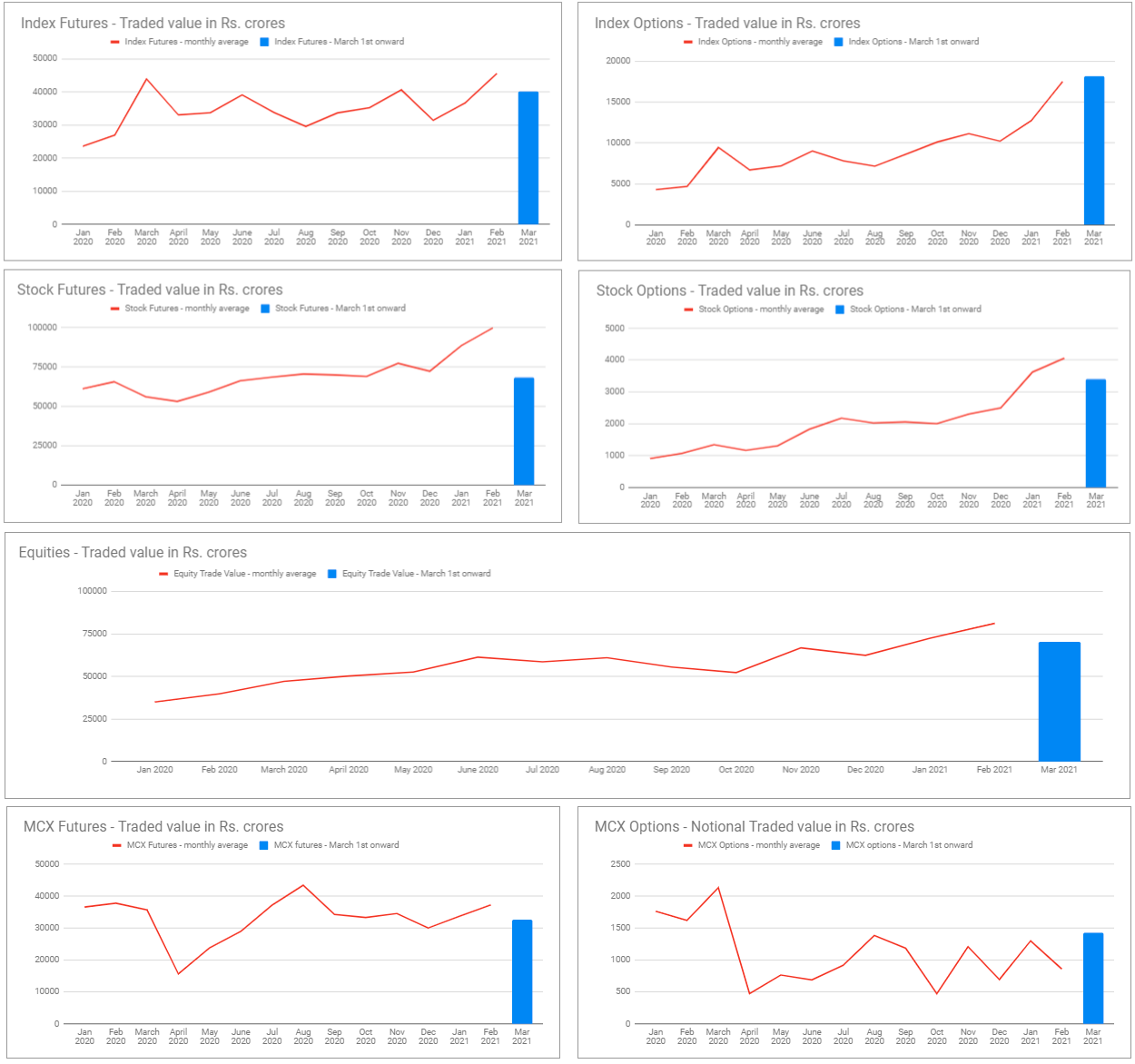

This is how trading volumes look pre-March to post-March as of 15th March.

As expected, futures are the most hit. The issue with customers moving from futures to options is that options (buying options) are much riskier.

Effect of reduction in intraday leverage in the long term

The best-case scenario is that with lesser leverage, the odds of a trader profiting/surviving go up significantly. Historically our industry has had the problem of very shallow retail participation in terms of the number of active traders. I’d fathom a guess of fewer than 10lk customers at any point, even when the industry might have added a lot more customers. The reason being for every 1 new customer getting added, maybe 1 stops trading (losses). So the net customers actively trading has remained the same. By actively trading I mean customers who trade frequently in stocks, intraday, & F&O, not equity investors.

So with lesser leverage, more traders survive, and hence the size of this industry by the number of participants will go up. While trading volume might reduce in the near term, the increase in the number of traders will hopefully make up for the drop in trading volumes with time. ![]()

My stance on if there should be additional intraday leverages or not?

Here is an FAQ from both the exchanges that explain what are margins, why they are collected, etc. Margins are calculated using the concepts of VAR+ELM for equity and SPAN+Exposure for F&O. Margins are collected to ensure there is as little counterparty risk of a trader defaulting in making good if there were losses (losing more money than what he/she has). It is important that this risk is low because a bunch of traders with a broker losing more money than what they have on a black swan day can potentially bring the broker and hence the entire settlement system down. A broker is required to pay up the margin/losses to the exchange the same day irrespective of client makes good of it or not.

Last year when Crude Oil closed in the negative, many customers who were long or had buy positions lost more money than what was in their account. This was even after collecting the entire SPAN+Exposure margin. Thankfully this was the time when due to lockdown restrictions MCX was closed by 5.30 pm. That day commodity brokers had over Rs 330 crores in losses (customer losses more than margin placed), it could have been Rs 3000 crores if MCX stayed open like normal till 11.30 pm. Rs 2000 crores would have been enough to bring the entire system down. So yeah, collecting margin and making sure that it keeps pace with change in volatility is super important.

Anyways, the main input to calculate margins is volatility, the higher the current volatility more the margin. In the case of SPAN+Exposure, along with volatility the time left to expiry also makes a small difference. The longer the time left for the expiry of contracts, the more the margin. One input that doesn’t get into this margin calculation is whether a position is intraday or overnight. As you would imagine the volatility within a trading day is usually much lesser than the volatility of trades held overnight. So technically if a trader is saying that the trade is not going to be held overnight (using intraday product types like MIS, CO, etc), then those are a lesser risk. In which case, there is an argument to be made that margin required for such intraday trades could be lesser than overnight trades.

How much lesser could the margins be for intraday?

We could use the same volatility calculations to determine VAR+ELM or SPAN+Exposure for intraday trades based on historical intraday volatility. My guess is that it will be at least 50% of overnight margins or around what the current intraday leverages are.

But yeah, all of this was put across as a request by the broker associations and exchanges to SEBI. I guess SEBI opted to look in for the longer-term benefits more than the shorter-term potential pain.