I guess everyone knows what happened to crude oil yesterday on the international markets, 20th April 2020. If you don’t, check this article:

I have been getting queries since yesterday night from people about how this incident has affected Zerodha and Indian commodity brokerage firms. So here is a summary.

Crude oil is one of the most actively traded commodities on MCX. It is a cash-settled derivative contract, which means on the expiry day all open contracts get settled as per the closing price of Crude on NYMEX (New York Mercantile Exchange). Most trading happens in futures contracts, very little in options. Crude oil on MCX is a 100 barrel contract, and Indian crude typically trades at International Crude * USDINR rate. Margin required to trade crude oil historically was around 10%, but with volatility, these margins go up. Currently, the margin required after yesterday is close to 70%.

For those who don’t understand futures (Check out Varsity to learn in detail), the way it works is you put up a portion of the contract as margin and you can either buy or short futures. If you buy and the market goes up, you make money, else you lose. But you can also short (sell first) and make money if it goes down, loose if it goes up. People trade futures mainly because of leverage (trade with only a portion of the contract value as margin) and also because you can short (make money when market falls). The margin a customer places with the broker is to ensure the counterparty risk is removed when the customer loses money and doesn’t pay up the loss. The only issue being, if the market goes against the customer by more than the margin placed, the customer can default, and the broker has to cover for the losses until it can be recovered from the customer. Most of the time, the margin requirement usually covers the risk, until the black swan shows up (like yesterday).

Coming back to what happened yesterday, crude has had huge amounts of volatility in the last few weeks. It started on 9th March, when crude oil lost over 30% at the market opening. The margin required for crude the previous Friday was 15%, this 30% gap down meant that customers who had bought futures would have lost twice the margin due to the gap down. If the customer didn’t have additional money, brokers get exposed to bad debts. I think on that day the industry as a whole was exposed to Rs 100 crores of bad debts, not really sure how much got recovered from the customers. But, post this fall the margin required to trade crude went up, which meant trading volumes dropped quite a bit. After the lockdown, exchanges reduced the trading timings (under pressure from a few brokerage firms who claimed that they couldn’t operate from home) from 11.30 pm in the night to 5 pm in the evening. This meant that customers, and in turn brokerage firms also were exposed to the risk of not being able to react when there were big moves happening in the international markets.

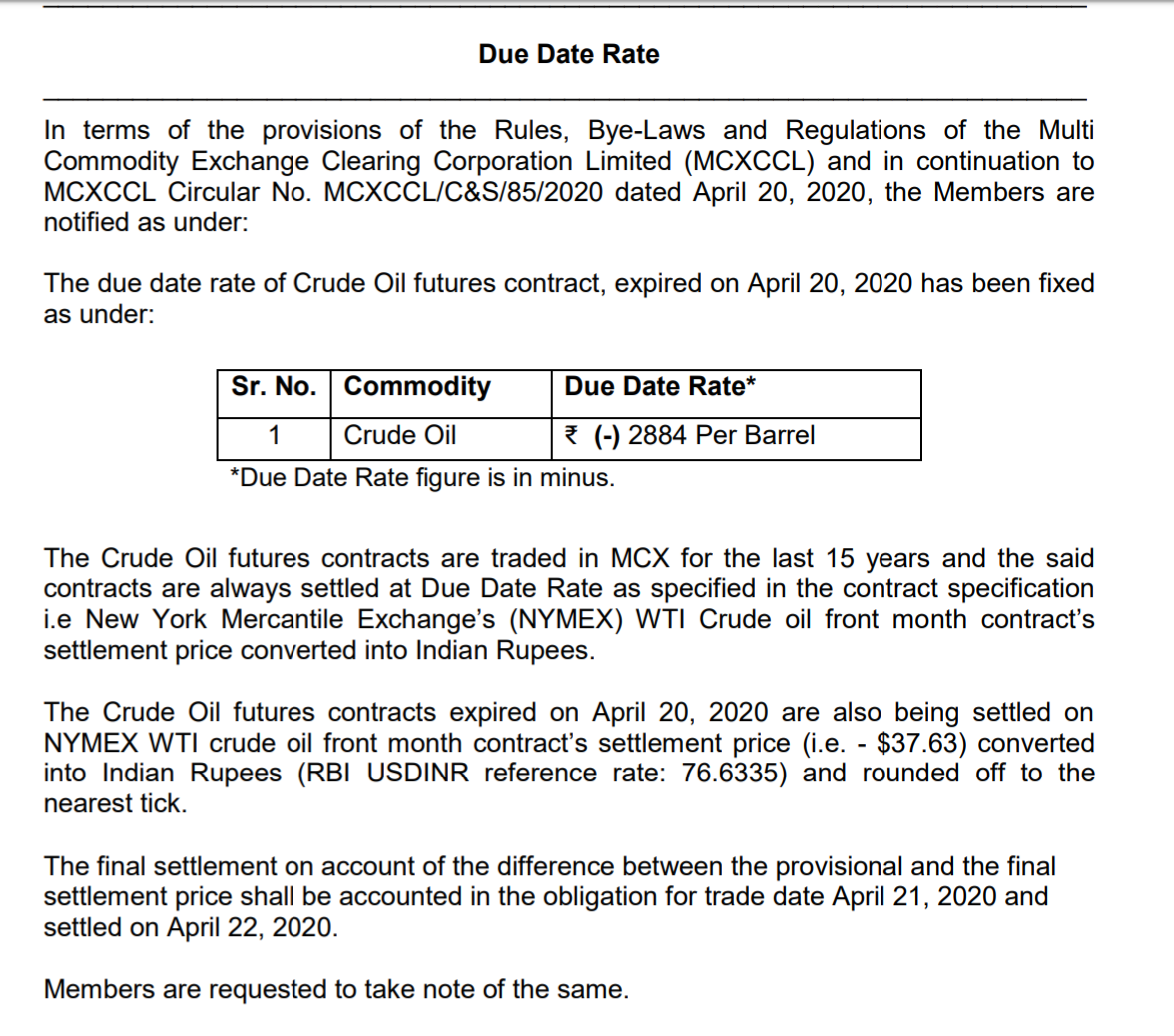

And yesterday was probably the craziest day of my 25 years of being in the capital markets. A contract trading at a negative value is unheard of. April crude on MCX was at around 1436 per barrel on April 17th, Friday closing. One lot of crude is 100 barrels, or the contract size is 1,43,600 as per Friday’s closing price. The margin required to buy crude was around 57% or around Rs 80,000. Crude started falling on the Monday, 20th morning itself. When our markets closed at 5 pm, MCX crude was trading at Rs 965, i.e., contract value had fallen to Rs 96500 or down around 30%. While a 30% fall is abnormal for crude, it was still okay for our risk management as the margin required was 57%, so even if some clients lost 30%, they had sufficient margins. Yesterday was the expiry day of Crude Oil April contracts, and the weird stuff started happening as the contracts headed to expiry on the international markets. The prices kept falling and guess what? They closed at -$37 on the international markets. This meant that all the Indian crude oil April contracts that were open would settle at -Rs 2880 (yeah, minus!).

Crude oil price on Indian markets at 5 pm was Rs 965, and the final settlement price was -Rs2880, which meant a loss of Rs 3.8lks for people who had a long position. The margin required to trade crude at 5 pm was around Rs 80,000, which meant that a customer with Rs 80000 would have lost Rs 3.8lks or Rs 3lks more than the money in the account. As I explained earlier, the onus is on the brokerage firm to make good the losses the next day and figure out ways to recover it from the customer. There were 11100 contracts open at 5 pm yesterday on MCX, which means a potential loss of over Rs 330 crores for the Commodity brokerage firms over and above the margins placed by customers.

Is Zerodha okay?

Our commodity business is run through a separate company called Zerodha commodities Pvt Ltd (Equity is through Zerodha Broking Limited). This company has a networth of close to Rs 100 crores. We are currently looking at debits of around Rs 10 crores (9th March and 20th April incident combined) which we are trying to recover from the customers. While the loss seems big and does hurt us, it is only around 10% of our net worth, so we are okay. Also quoting from a recent email we had sent to all customers

How safe is Zerodha?

I have answered this many times, but it keeps coming up. With a general concern on the health of financial services firms after the recent stock market meltdown, I thought maybe it prudent to update you on why you should not be concerned about your relationship with us.

- We are a zero-debt financial services company. There is no borrowing of any kind.

- There is no credit risk, less than 5% of our own capital is lent to customers in any form.

- Our own funds in the business are greater than 25% of all client funds put together.

- Our ratio of ‘complaints to active clients’ is among the least on the exchange.

- We are profitable as a business and have enough reserves to sustain (over Rs 1000 crores across our companies), even if there was an extended downturn in the economy.

- We haven’t spent any money on marketing and advertising. The month of March was our largest till date in terms of new client account opening, thanks to our million-plus happy customers who help us spread the word.

What about other brokerage firms?

There are around 300 commodity brokerage firms who offer trading in Crude oil contracts. A few small firms are bound to go bust without having sufficient money to pay up for the loss. We’ll only get to know tomorrow about who will be able to survive this episode.

Broking business, especially the leveraged side, is very similar to the Insurance industry. You keep earning a

small premium on every deal (brokerage), but one black swan event is enough to bring you down. The only way to survive is to make sure what you earn can cover the risk of bad debts on these event days when the market movement is greater than the margin collected.

We have invested in multiple businesses, and I am close to founders of many startups, I don’t think there is any business as complex as broking, especially the F&O and equity intraday trading bit. All the dependencies which are not in your control and can potentially bring you down are crazy - from leased lines connecting to exchanges to an event like what happened with crude yesterday.

Update 22nd April

Interactive Brokers puts out a press release, provisionary loss of $88 million due to this episode. Check this article.