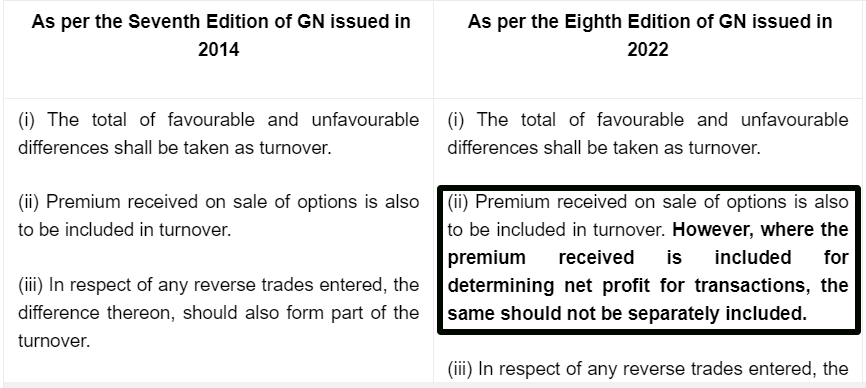

Finally, in some good news for options writers, ICAI has clarified that when calculating turnover to determine tax audit, only the profit or loss has to be considered. No need to separately add the premium received when writing options as turnover.

Here is the link to the guidance note (page 17). GN 44AB-DTC-19-8-22-fINAL.pdf - Google Drive

We have updated the Varsity chapter on taxation. We will update our tax P&L statements to show option turnover per the guidance note in a few days.

Hopefully, the audit requirements when online trading is the only business income are also Simplified soon.

Trading isn’t like running a normal business, and audit requirements are onerous for retail investors. Hence, most traders avoid declaring when filing ITR.

Folks who are having any doubt regarding what’s the impact on option buyers :

There’s no change as even earlier, profit or loss was used to determine the turnover for option buyers.

Sellers had this addition burden to add premium recd on sale of options in turnover (for weird reasons), that rule is removed now and buyers and sellers are now on par with each other when it comes to determining tax audit applicability.

Our resident CAs here at @Tradingqna - @Jason_Castelino and others can confirm if the above statement is correct or incorrect

Yes. Some relief for the ones trading in options. But I do not understand one thing. How is it good news only for sellers? It’s for both buys are sellers. The turnover was calculated the same way earlier for both buys are sellers.

I came across this article late and had already filed as per previous rules. Also had to undergo audit because of it ,not to mention the book keeping charges. This was costing me so much every year. Did all loss making traders with turn over of over 1 cr had to do the same thing?