Whenever you talk about market timing, the most common reaction you hear is - “Don’t do it, it won’t work.” Which, for most past is true but if you absolutely had to do, here’s one right way to do it.

This paper is by Clifford Asness, Antti Ilmanen, and Thomas Maloney. These guys are quite literally genius quants. They are part of a firm called AQR which manages about $200 billion. It’s famous for factor-driven strategies such as Value, Momentum, Low-volatility etc. They publish some amazing research on all things markets, if you guys want to check out.

Anyway, here are some select excerpts from the paper on Market Timing.

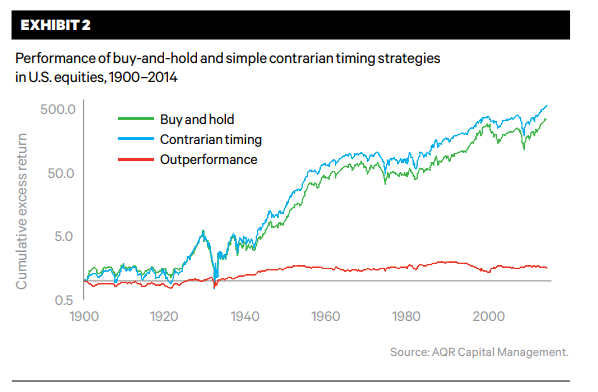

If market timing is a sin, then there are times when even the saints can be tempted into sinning a little. We are going to argue that market timing isn’t really a sin except, as for so many things, if done to excess. But the results and logic behind the two simple strategies that govern so much of the investing world — basic value, or contrarian, investing and basic momentum, or trend-following, investing — imply that when it comes to market timing, one should indeed sin a little and do so as a matter of course, not just at extremes.

Today’s high stock prices, and for that matter low bond yields and concomitant low expected future returns (at least in our opinion), naturally bring the timing discussion back to the forefront, leading many investors to wonder if they should get out now. The answer to this question is almost certainly not. “Getting out now” is a very extreme action yet oddly often how people think about market timing (an approach to timing that we will soon label binary, immodest and asymmetric). If, on the other hand, investors wonder whether they should own somewhat fewer stocks and bonds than usual right now — well, that’s a much harder and much more interesting question. Overall, for those who think market timing is infeasible, we give hope. At the other extreme, some observers oversell market timing as easy and reliable. It ain’t.

We see a clear and strong relationship. Decades that started with low P/Es had, on average, subsequently higher average excess (over cash) returns, and decades that started with very high P/Es experienced the opposite: very low average excess returns by historical standards. Of course, like all averages, a lot of variation is obscured by only looking at this summary. There was quite a range around the average decadelong return in each of these buckets.

Link to the full paper